Asia Inherits a Full Stress Reversal — But Tech Did All the Work

Wednesday’s US session didn’t just recover — it reversed every single stress signal from Tuesday in one move. VIX back in contango. P/C flipped bullish. Fear & Greed out of fear territory. The question for Asia tonight: does this become a global bid, or does the tech-only leadership leave the rally on thin ice heading into OpEx?

Published pre-London handover

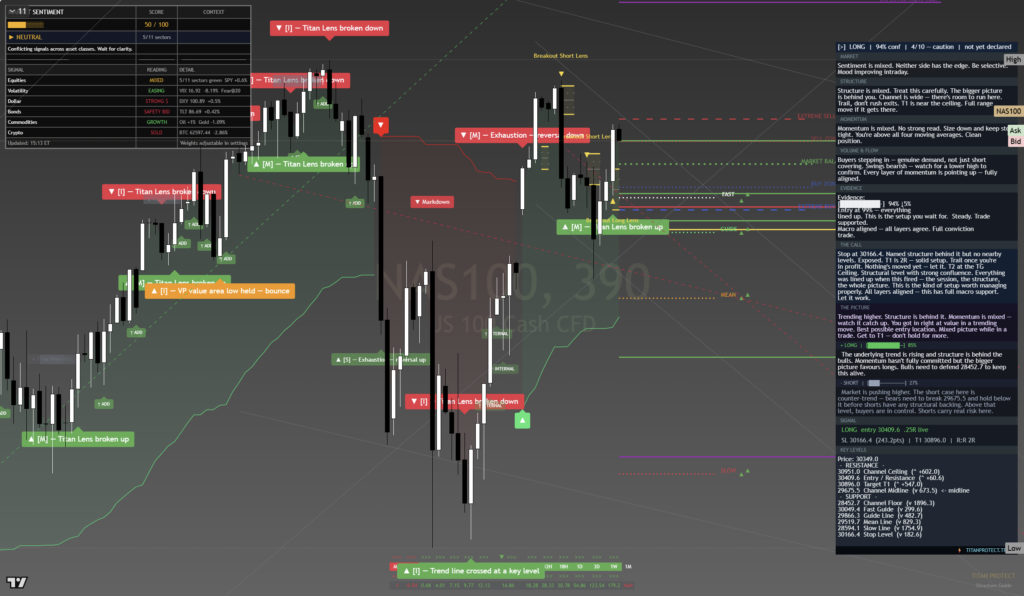

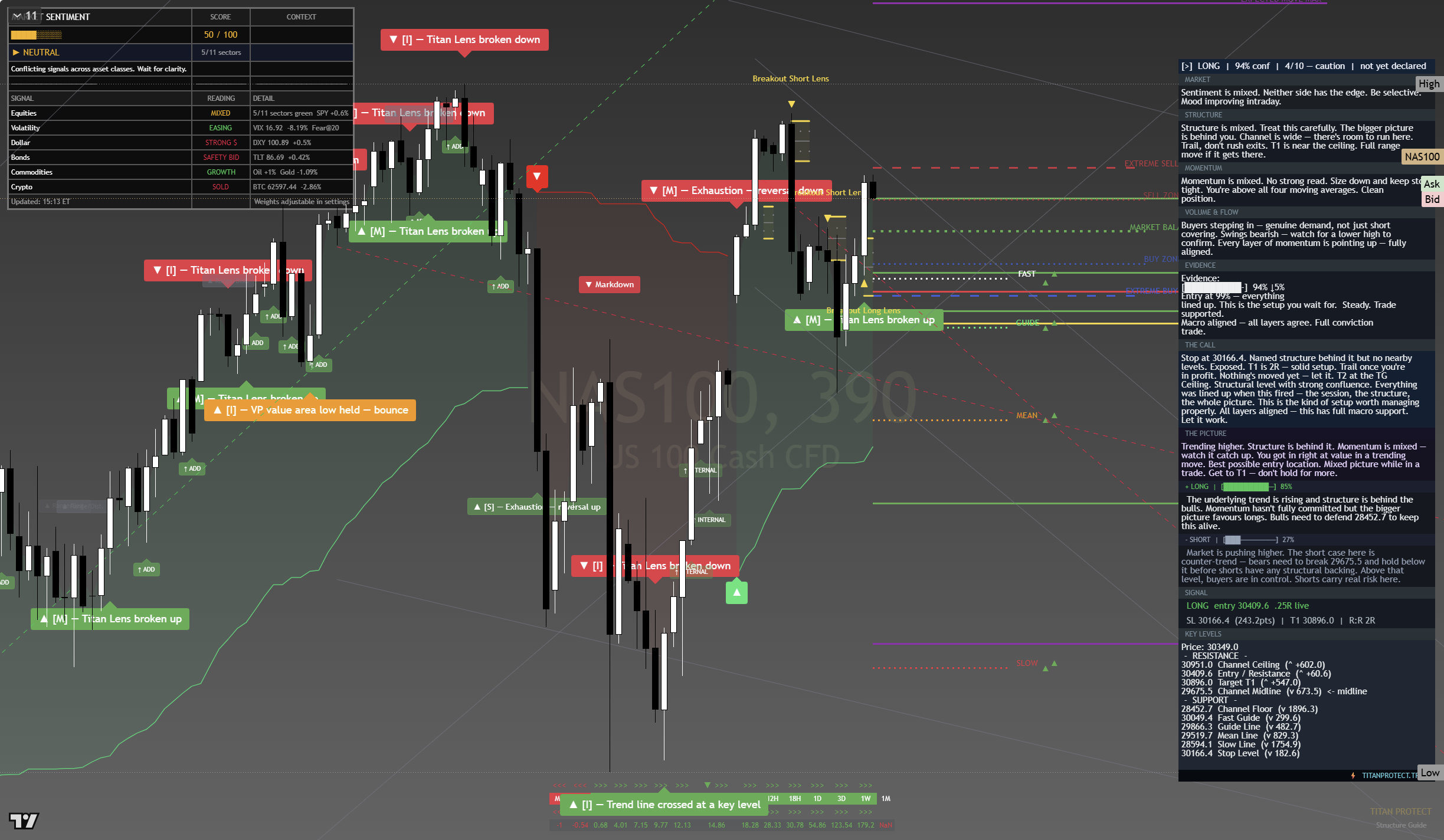

NAS100 daily — Post-close capture 18 June 2026 | Titan Macro Desk

1. The US Session: Everything Reversed

Wednesday handed markets what they needed — a clean, decisive flush of the stress signals that had been building since Monday. NAS100 closed at 30,362 (+2.33%). SPY hit $745.97, up 0.68%. The divergence between those two numbers tells you something: this was a tech rally first, a broad market rally second.

Three catalysts did the heavy lifting. Accenture beat on earnings and guided higher — the kind of read-across that gives the market permission to re-rate tech multiples. The Iran nuclear deal was formally signed, removing a tail risk that had been suppressing risk appetite for weeks. And the BOE held at 3.75%, removing the threat of a surprise rate shock out of London. None of these things are wildly bullish on their own. Together, they cleared the path.

CLOSING SNAPSHOT — WEDNESDAY 18 JUNE

| Instrument | Level | Move | Read |

|---|---|---|---|

| NAS100 | 30,362 | +2.33% | Tech led |

| SPY | $745.97 | +0.68% | Broader, thinner |

| VIX | 16.73 | ‑1.71pts | Contango restored |

| Fear & Greed | 37.1 | Recovered | Exited fear zone |

| gex-max-pain-and-putcall-ratios/” style=”color:#D8AF44;text-decoration:underline” title=”What is Options Intelligence?”>P/C Ratio | 0.889 | Flipped | Bullish positioning |

| XLK (Tech) | +2.78% | Led | Sector winner |

| XLE (Energy) | ‑1.98% | Lagged | Iran deal pressure |

| Gold | $4,335 | Flat | Not fleeing, not chasing |

| Crude Oil | $74.14 | Soft | Iran supply risk priced out |

| BTC | $63,832 | Absent | Did not participate |

The QQQ vs DIA split was only 2.3 points — narrower than you’d expect given the NAS100’s 2.33% move. That’s not a red flag, but it’s worth noting: the Dow isn’t fully on board. Housing Starts missed by 5.5%, a data point the bond market will have filed away. Philly Fed beat at +10.3 — manufacturing resilience holding for now. The net read: the recovery is real, but it’s narrow.

2. What Asia Inherits Tonight

Asia doesn’t get a clean sheet. It gets a market that has snapped back hard, where the easy move is already done. Here are the five things that define tonight’s session.

SPY closed at $745.97. Max pain is $725.00. That’s a $20.97 gap. On OpEx Fridays, dealers hedge gamma exposure by selling into strength and buying into weakness. This mechanical pressure means Asia and early London session strength into 745+ is not necessarily confirmed momentum — it could be a headwind being priced by dealers running off positions.

3. Regional Setup: Nikkei, Hang Seng, ASX, Nifty

The Nikkei should follow the US bounce. It has the clearest transmission path — US tech strength pulls Japanese exporters, and USD/JPY staying elevated at 160.59 is margin-boosting for multinationals. The risk: yen at intervention level. If the BOJ or MoF steps in overnight, the move reverses fast. Watch the 160.00 handle on USD/JPY as the stress indicator for this session.

Don’t expect Hang Seng to follow the US rally cleanly. China’s structural headwinds — property sector overhang, deflationary pressure, limited stimulus firepower — mean the index has its own gravity. A relief bid is possible on Iran deal news (reduced geopolitical premium) but the ceiling is lower. This is not a US beta trade tonight.

The ASX faces a split. Financials and tech follow the US lead higher. But resources — the ASX’s backbone — are fighting Iran-deal crude weakness and a softer gold bid. Crude at $74.14 is energy sector headwind. Gold flat at $4,335 doesn’t hurt but doesn’t help. Net: ASX likely opens higher but underperforms the US move.

India benefits from the Iran deal — reduced oil import costs for a current account deficit economy. But the strong dollar creates INR pressure that partially offsets the tailwind. Nifty tends to show the Iran deal benefit with a lag as the macro transmission works through. Domestic demand narrative intact, but this session is secondary to Nikkei as the primary read.

4. FX Context: The Dollar Is Still the Story

The dollar didn’t give back any gains despite the equity rally. That’s the friction point for Asia tonight.

160.59 is not a number Japan’s monetary authorities are comfortable with. The last intervention came at similar levels. Asia session FX desks are watching every tick. If BOJ/MoF steps in — even verbally — that triggers yen buying, Nikkei selling, and a broad reset of the carry-funded positions that helped the US rally. This is the single biggest tail risk in tonight’s session.

5. Commodity Context: Gold Unmoved, Crude Soft

Gold’s flat close is worth sitting with for a moment. In a session where every other risk asset was rallying, gold didn’t sell off. That’s the behaviour of a market that’s recovered a mood, not one that’s convinced the problem is solved. The overnight gold bid (or lack of one) will tell you how Asia really feels about the sustainability of Wednesday’s move.

6. OpEx Friday: What It Means for Asia Positioning

Options expiration is tomorrow. This changes the mechanics of tonight’s session in three specific ways.

7. Key Levels for the Asia Session

8. Asia Session Scenarios

9. Asia Session Bias

Wednesday’s session was as clean a stress reversal as you get. All the boxes were ticked: VIX down, sentiment recovered, catalysts cleared. The problem is where it left us — at $745.97 on SPY with max pain $21 below. That’s not a reason to fade the move, but it’s a reason not to chase it aggressively.

For Asia specifically: the Nikkei is the clearest expression of this recovery. The yen carry is doing its job, US tech is doing its job. The risk is the BOJ, and 160.59 is close enough to 161 that every tick matters. If you’re positioned long Nikkei, know where your stop is — it’s not a structural view, it’s an overnight carry with a government intervention risk attached.

The framework isn’t chasing. It’s noting where the recovery happened, reading what didn’t confirm (crypto, energy, breadth), and letting OpEx Friday’s mechanics resolve before adding conviction. The honest read: the setup is bullish in tone, but thin in breadth and carrying OpEx friction into tomorrow.

This briefing is produced by the Titan Macro Desk for informational and educational purposes only. It does not constitute financial advice, a solicitation, or a recommendation to buy or sell any financial instrument. All market analysis involves uncertainty and past patterns do not guarantee future results. Trading financial instruments carries significant risk of loss, including the loss of more than your initial capital. Readers should conduct their own research and seek independent professional advice before making any investment decisions. The Titan Macro Desk may hold positions in instruments discussed. All levels and probabilities are analytical assessments, not guarantees of outcome.