Thursday 18 June 2026 | TMA locked 19:10 UTC

Every Stress Signal Reversed: How Thursday Erased a Week of FOMC Fear

Titan Macro Desk · Alpha Insights

1. The Session That Reversed Everything

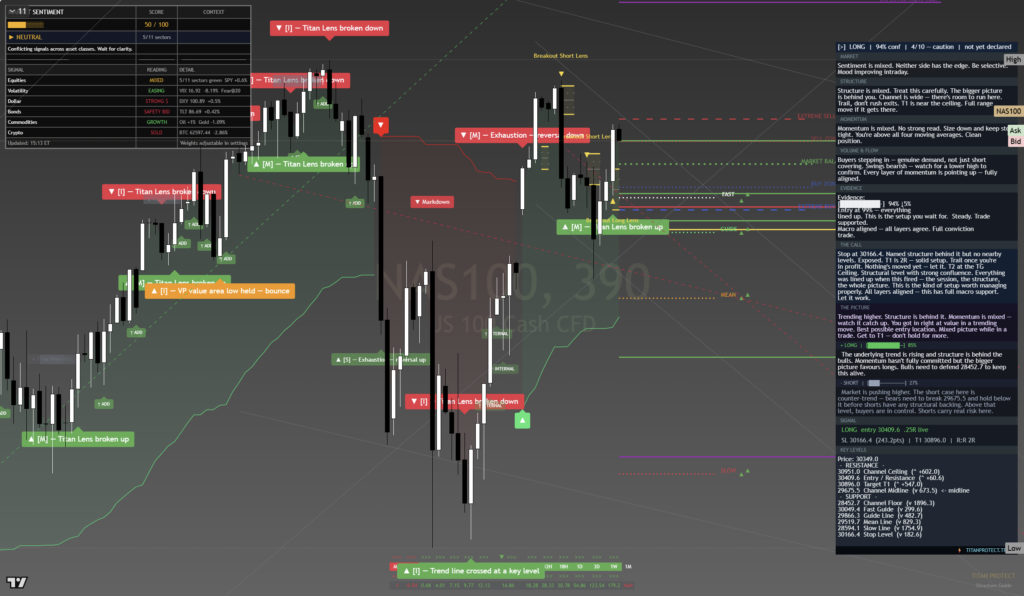

Wednesday’s FOMC decision left the market in a stressed state. VIX sat at 18.44. The put-call ratio was at 1.123, signalling bearish positioning. The VIX term structure had inverted into backwardation. Fear and Greed had dropped to 32.7. Four signals, all pointing the same direction.

By Thursday’s close, all four had reversed. Not gradually. In a single session.

The catalyst stack was clean: the BOE held rates as expected, removing an unknown. The Iran signing ceremony proceeded with a $300 billion fund announced, resolving what had been an open geopolitical variable since Monday. ACN delivered earnings that reaffirmed the AI spending narrative. And the US data, while mixed, was not damaging enough to shift the Fed calculus.

Markets took all of that and ran. NAS100 gained 691 points from Wednesday’s close. SPY moved from $740.96 to $745.97. The overnight bounce that opened the Pre-NY brief had not only held — it had extended.

2. What We Called vs What Happened

The Pre-NY brief flagged three scenarios. Here is the scorecard against closing data.

| Pre-NY Call | Outcome | Result |

|---|---|---|

| Overnight bounce holds and extends | NAS100 +2.3%, SPY +0.68% by close | Confirmed |

| Tech leads if risk-on sustained | XLK +2.78%, QQQ +2.28% vs DIA -0.02% | Confirmed |

| Energy pressure from Iran resolution | XLE -1.98% — worst sector on the day | Confirmed |

| VIX collapse if rally extends | VIX 18.44 to 16.73, down 9.3% | Confirmed |

| Breadth risk: narrow tech rally | DIA -0.02%; XLF -0.74%; Dow negative | Realised |

Four from four confirmed. The breadth risk call was the nuanced one — the rally was real but it was not broad. That distinction matters most going into OpEx Friday.

3. Closing Data Dashboard

| Instrument | Close | Day Change | Signal |

|---|---|---|---|

| SPY | $745.97 | +0.68% | from $740.96 |

| NAS100 | ~30,362 | +2.3% | +691pts from Wed close |

| VIX | 16.73 | -9.3% | Collapsed from 18.44 |

| VVIX | 88.56 | -6.0 | Down from 94.53 |

| Fear & Greed | 37.1 | +4.4 | Out of Fear (was 32.7) |

| gex-max-pain-and-putcall-ratios/” style=”color:#D8AF44;text-decoration:underline” title=”What is Options Intelligence?”>P/C Ratio | 0.889 | Flipped bullish | Was 1.123 (bearish) this morning |

| VIX Term Structure | Contango | Restored | Was backwardation (stress) |

| Options Sentiment | Bullish | Upgraded | Was “mixed” at Pre-NY |

4. The 5-Day Arc — Complete

This week’s sequence is worth recording in full. It is a textbook example of how the market processes a concentrated catalyst stack.

| Day | Event | Market Reaction |

|---|---|---|

| Mon | Iran ceasefire + SpaceX IPO euphoria | +3% gap up — sentiment at extreme |

| Tue | Reversal day, buyers exhausted | NAS100 -670pts from open |

| Wed | FOMC: hawkish hold, no cuts | VIX +12%, backwardation, P/C bearish |

| Thu | BOE hold + Iran deal + ACN beat | +2.3%, all stress signals reverse |

| Fri | OpEx Friday — $725 max pain | Open question (see Section 7) |

5. Sector Divergence — The Key Finding

The headline numbers look like a broad rally. They are not. Thursday’s move was deeply concentrated in tech, with significant divergence underneath.

| Sector ETF | Day % | Driver |

|---|---|---|

| XLK (Technology) | +2.78% | AI bookings, ACN earnings confirmation |

| QQQ (NAS100 proxy) | +2.28% | Tech concentration |

| DIA (Dow proxy) | -0.02% | Old economy names flat to red |

| XLF (Financials) | -0.74% | Rate sensitivity, hawkish Fed lingering |

| XLE (Energy) | -1.98% | Iran $300B fund = long-term crude supply increase |

Breadth Warning

QQQ +2.28% versus DIA -0.02%. That is a 2.3 percentage point split on the same risk day. When tech is the only thing working and defensives plus financials are red, the market is not confirming broad recovery. It is rotating hard into one theme. Momentum can sustain this — but it is also the configuration that reverses fastest when tech stumbles.

Earnings context: ACN beat EPS at $3.80 and reported 104 AI deals exceeding $100 million in bookings. That is the data point that fuelled XLK. The flip side: KR missed on both EPS and revenue, testing the defensive consumer staples thesis at a time when the broader market assumed the defensive trade was safe.

6. Options Context — Four Reversals in One Session

The options market read is unusually clean today. Every structural stress signal resolved within hours of the US open.

The VVIX moving from 94.53 to 88.56 confirms that implied volatility of volatility is also collapsing — options market participants are no longer hedging aggressively against further vol spikes. That is a structural confidence signal, not just a price move.

The speed of these reversals is worth flagging. Structural reversals in a single session tend to be one of two things: genuine regime change driven by resolved uncertainty, or a short squeeze in hedges that can re-establish just as quickly. The catalyst mix today — BOE, Iran, earnings — points to genuine uncertainty resolution. But the OpEx dynamic tomorrow introduces fresh mechanical risk.

7. OpEx Friday Setup

Friday 19 June is monthly options expiration. This is the mechanical context that matters most for what the market does tomorrow.

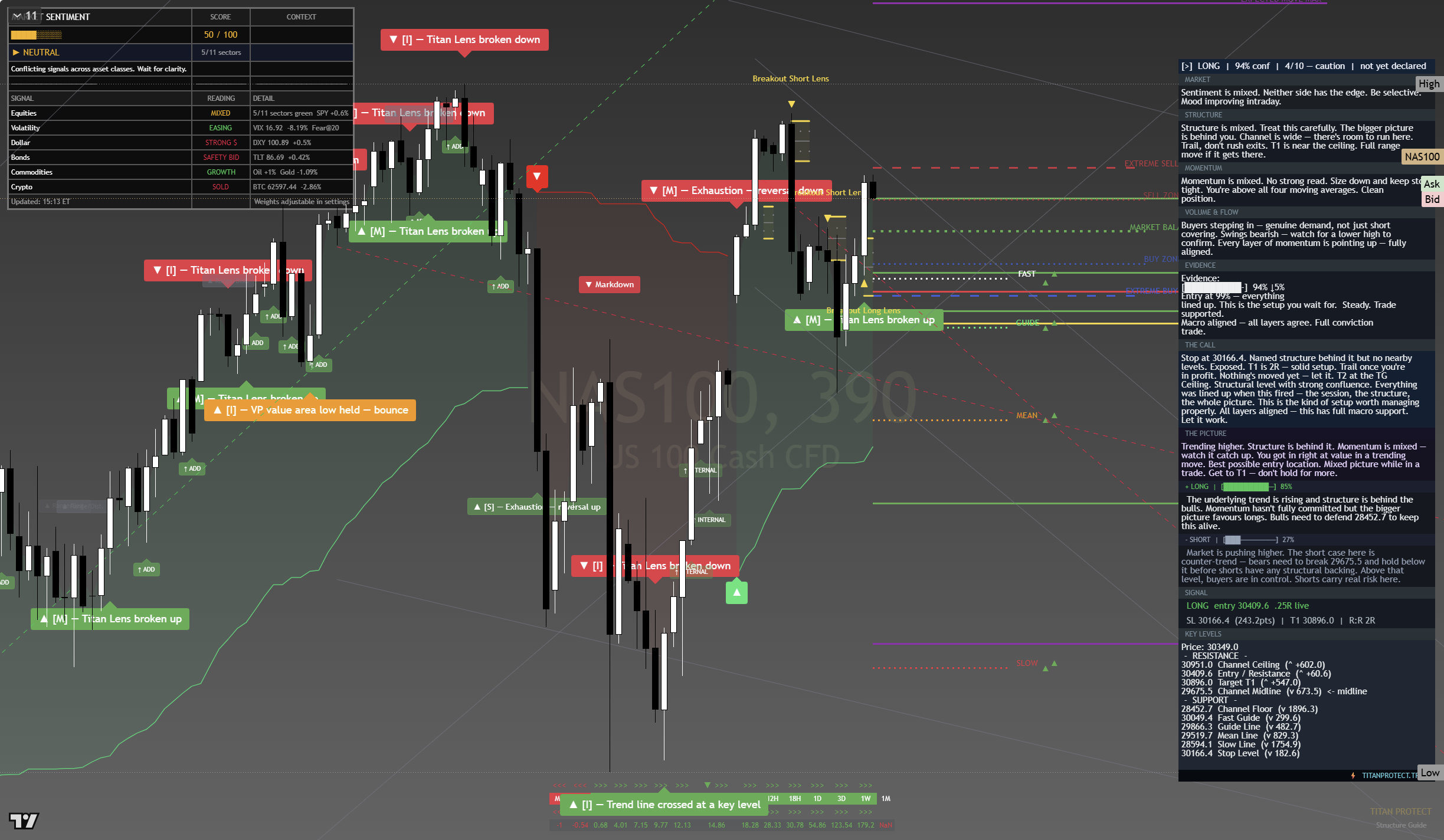

Thursday’s rally widened the max pain gap rather than narrowing it. SPY is now $21 above the level where options market makers face maximum profitability. In a negative gamma environment, market makers hedge directionally: they sell into rallies and buy into dips, which amplifies moves in both directions.

| Scenario | Condition | Probable Range | Risk |

|---|---|---|---|

| Momentum continues | Tech holds + breadth catches up | SPY $746-755, NAS100 30,400-30,700 | Around 25% |

| Chop / Pin | Market consolidates, OpEx mechanics neutral | SPY $738-748, NAS100 29,900-30,400 | Around 45% |

| Max pain pull | Gamma pinning toward $725, sector rotation | SPY $725-738, NAS100 29,400-29,800 | Around 30% |

Position Sizing Note

OpEx Fridays in a negative gamma environment with a $21 max pain gap are not the days to carry large directional risk overnight. The mechanical path toward max pain is a $21 move lower from spot. If the pin scenario plays out, stops matter. Size accordingly: reduce exposure to around 60-70% of normal session sizing until the first 90-minute range establishes itself.

8. Market Intelligence From the Feeds

Key signals from the analyst network today:

Fed Structure

Warsh’s 5 task forces signal structural Fed reform is being prepared. This is a medium-term dollar and rates story, not priced into Thursday’s session but worth watching into Q3.

Iran / Oil

The $300 billion fund announced at the signing ceremony is a structural crude supply increase signal. XLE -1.98% today reflects this. The energy sector repricing may not be done — medium-term bearish for energy, constructive for input-cost sensitive sectors.

Insider Activity

Insider buying running at 736:1 concentrated in UK names. Domestic US insider flows are quiet by comparison. The UK concentration aligns with BOE-on-hold positioning and suggests institutional accumulation in sterling assets.

SpaceX / SPAX

SPAX ETF down 13.6% from Monday’s session open. IPO euphoria unwinding on schedule. Monday’s +3% move was partially driven by this narrative — the partial reversal this week has been orderly, but the ETF is still extended versus fair value on most models.

9. Today’s Alpha Insights: Full Coverage

Thursday’s session generated 19 Alpha Insights posts spanning every layer of today’s market move. Key cross-references:

- NAS100 read: The +2.3% session in context of the FOMC week arc and what the level means heading into OpEx.

- VIX collapse analysis: Backwardation to contango in one session — what the term structure is telling us about positioning into next week.

- Sector rotation: XLK +2.78% vs XLE -1.98%. The Iran deal impact on energy and what it means for sector positioning into summer.

- ACN earnings deep dive: The AI bookings number (104 deals over $100M) and what it signals for the broader enterprise tech spend cycle.

- BOE hold analysis: 3.75% maintained. What the UK rate path looks like from here and how sterling positions reacted.

- OpEx mechanics: Max pain at $725, negative gamma — the full setup for Friday’s session.

The complete set of 19 posts is live on the Alpha Insights feed. Members received the briefing 24 hours ahead of public release.

10. What Asia Inherits Tonight

Asia opens with a materially cleaner risk environment than it has had since Monday. Here is the handover state:

| Regional Asset | Bias inherited | Key watch |

|---|---|---|

| Nikkei 225 | Bullish handover from Wall St | JPY direction; if yen strengthens, limits upside |

| Hang Seng | Cautious; China stimulus disappointment ongoing | Any PBOC or property sector headlines |

| Crude oil | Bearish near-term on Iran supply | Any implementation delays on Iran deal |

| Gold | Mixed; safe haven demand eased but USD firm | Overnight USD moves; Fed reform headlines |

| US Futures (overnight) | Flat to marginal positive; OpEx creates drag | Futures premium vs max pain gap |

Pre-Asia Brief Focus for Friday

The Pre-Asia brief at session open should lead with the OpEx mechanics, regional response to Thursday’s Wall St close, and any overnight futures signals. The Iran deal is priced but implementation risk is not zero. If the overnight PBOC window produces any announcement, Hang Seng will be the first mover to watch.

11. Thursday’s Close Bias — One Line

Every stress signal from Wednesday’s FOMC session reversed in a single day; the market is structurally cleaner heading into OpEx Friday, but a $21 max pain gap below current spot and a narrow tech-only rally leave the session susceptible to a 30% probability pin toward $725.