Titan Macro Desk

Iran Deal Signing Meets BOE Day — Which Force Wins London Open?

Pre-London Brief | Thursday 18 June 2026 | Iran Deal + BOE Day

Published: 05:15 UTC | Titan Macro Desk

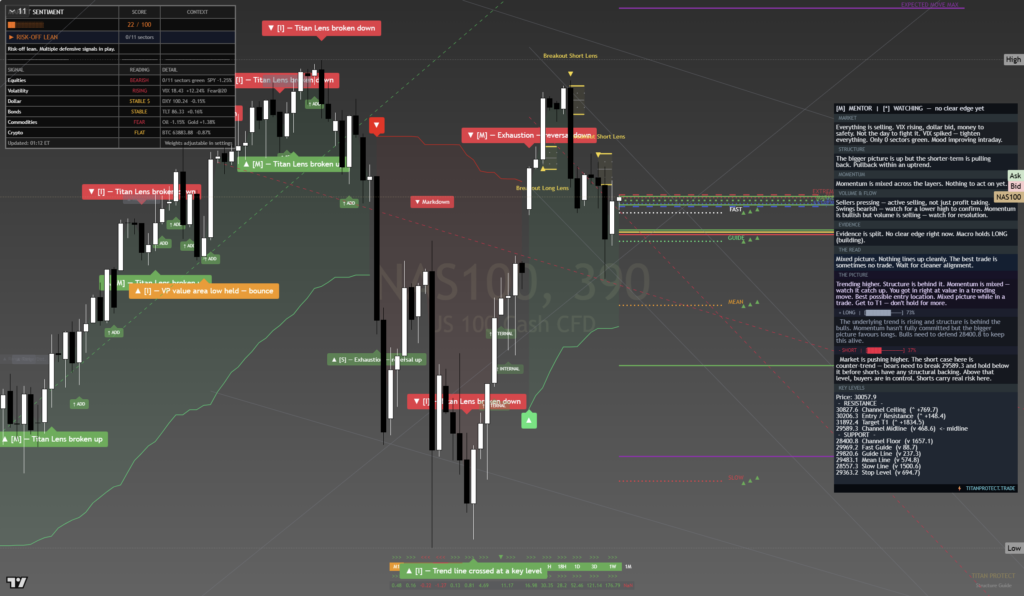

The market spent four days telling us one story, then rewrote it three times. Monday was euphoria — Iran peace headlines and SpaceX lifted everything +3%. Tuesday was the hangover — a 670-point reversal as traders decided they’d bought too fast. Wednesday was the Fed — hawkish hold, VIX jumped 10% to 17.99, gold sold off 1.68%, the dollar caught a bid. Now it’s Thursday, and we have two catalysts landing simultaneously: the official Iran deal signing and the Bank of England rate decision. NAS100 bounced 300 points overnight to 30,059. Our read: this is a session where the answer won’t be obvious until mid-morning. Two forces of roughly equal weight are pointing in opposite directions, and the one that fades first tells you everything.

Where We Stand at 05:15 UTC

| Instrument | Level | Wednesday Move | Our Read |

|---|---|---|---|

| NAS100 | 30,059 | Overnight bounce +300pts from 29,757 | Dip buyers active but conviction low |

| S&P 500 | 7,423 | -1.17% Wed | Still below pre-FOMC levels |

| VIX | 17.99 | +10.0% Wed | Elevated — hedges still on |

| Gold | $4,258 | -1.68% Wed | Dollar strength hit hard; safe-haven bid gone |

| DXY | 100.40 | +0.87% Wed | Fed hawkishness buying the dollar |

| Crude (WTI) | $75.41 | -0.84% Wed | $5.48 below pre-deal level — already pricing Iran |

| GBP/USD | 1.3300 | -1.08% Wed | BOE decision amplifies or reverses this |

| Bitcoin | $64,408 | -1.82% Wed | Risk-off mode following equities |

| Fear & Greed | 34.7 | Fear territory | Monday euphoria fully unwound |

| gex-max-pain-and-putcall-ratios/” style=”color:#D8AF44;text-decoration:underline” title=”What is Options Intelligence?”>P/C Ratio | 0.824 | VVIX: 93.94 | Moderate put buying; not extreme fear |

The Four-Day Arc That Got Us Here

Understanding Thursday requires stepping back to Monday. This week has been a textbook sentiment whipsaw, and the session structure matters.

The net effect over four days: the market started at roughly 30,700 (pre-Monday levels) and is sitting at 30,059 — down but not broken. What’s important is that two of the three big macro shocks this week (Iran, FOMC) are now known quantities. Today we get the third: how the BOE responds to the hawkish Fed backdrop, and whether the formal deal signing does anything crude — and risk — haven’t already done.

Catalyst One: The Iran Deal Signing

The headline is significant. An official signing ceremony on a ceasefire extension, Strait of Hormuz reopening protocols, and the start of nuclear talks is a genuine geopolitical shift. But the market got ahead of this on Monday, and the question isn’t whether the deal is real — it’s whether it moves prices from here.

Look at crude: it was $80.89 before the deal started being priced. It’s now $75.41. That’s a $5.48 supply-expectation premium that’s already been extracted. The Strait carries roughly 20% of global oil flow — when markets believed it was reopening, they sold crude aggressively. Today’s signing is the formalisation of a belief that was already priced.

The question our read focuses on: is there any element of today that wasn’t in Monday’s price? Three things could still move crude and risk today:

- A surprise timeline for full Hormuz normalisation — faster than expected reopening would push crude lower and support energy-cost-sensitive risk assets

- A broader ceasefire scope than the 60-day extension — if this extends to a framework agreement, that’s new information

- Any reversal or complication at the signing — a breakdown or last-minute obstacle would spike crude and crush equities fast

The base case: this is a confirmation event, not a catalyst. Crude drifts sideways to slightly lower, risk assets get a modest sentiment lift that fades by mid-morning. The market already owned the deal — the signing just files the paperwork.

Catalyst Two: The Bank of England Decision

GBP/USD came into today at 1.3300, down 1.08% on FOMC day. The pound is carrying a Fed-hawkishness discount — when the dollar rallied Wednesday, cable got hit. Now the BOE has to show its own hand, and the reading of the room matters enormously.

The BOE’s dilemma is the same one facing every central bank that isn’t the Fed: they’re responding to their own inflation data, but the Fed’s posture sets the global liquidity backdrop. If the BOE holds and sounds hawkish — matching the Fed’s tone — sterling could recover some of Wednesday’s losses, which would read as GBP strength and likely see FTSE 100 come under mild pressure (exporters lose a tailwind). If the BOE holds but sounds dovish — hinting at cuts later in the year — sterling could slide further, FTSE 100 benefits from the currency effect, but the macro message is negative for UK assets broadly.

Our read: the BOE follows the Fed’s hawkish hold framing. Bailey has been cautious about premature easing. Inflation in the UK hasn’t fully resolved. Expect hold + neutral-to-hawkish language. This stabilises sterling around 1.33–1.34 and has a neutral read for NAS100 — the US market won’t react much to UK rate rhetoric unless it triggers a broad EM FX move.

The FOMC Overhang

Wednesday’s Fed decision was the heaviest thing that happened this week, and it didn’t go away with the close. A hawkish hold means rate cuts are pushed further into the future. That affects:

- Equity multiples — higher for longer rates compress P/E ratios, particularly in tech-heavy indices like NAS100

- Growth expectations — consumer spending and corporate borrowing are both rate-sensitive

- Dollar strength — DXY at 100.40 is a headwind for multinational earnings and commodities

The VIX at 17.99 is telling us that participants are still holding tail hedges. It’s not a fear spike — it’s a worry level. That’s different. Fear spikes get bought. Sustained worry levels drain confidence slowly. Pair that with the Fear & Greed index at 34.7 — we’ve come a long way from Monday’s enthusiasm.

Our read on the FOMC overhang: It doesn’t disappear today. Even if Iran provides a sentiment boost at the open, the underlying rate environment is the same as it was Wednesday afternoon. Any rally built on geopolitical optimism that doesn’t come with better macro data will likely face selling into strength.

OpEx Friday Setup

Tomorrow is monthly options expiry. That matters today because gamma is already shifting. Before FOMC, the gamma landscape had a particular structure. Post-FOMC with VIX up 10%, the strike landscape has reshuffled. Market makers have repositioned, and that affects how directional moves behave in today’s session.

With P/C at 0.824 and VVIX at 93.94, the structure suggests moderate hedging activity rather than extreme positioning. VVIX under 100 means the market isn’t screaming for volatility insurance on top of volatility — which is a relatively contained environment despite VIX at 17.99.

For London session specifically: Expect gamma compression to tighten the range around key strikes. If NAS100 can hold above 30,000, positive gamma forces work to stabilise. If 30,000 breaks, the next natural gamma support is lower — and the pre-FOMC low of 29,757 becomes the reference.

Three Scenarios for the Session

| Scenario | Probability | NAS100 Path | What Triggers It |

|---|---|---|---|

|

Iran Catalyst Rally

Geopolitics offsets Fed

|

35%

|

Pushes above 30,200, tests 30,350+. Crude holds $74–$76. Risk-on tone. | Deal signing comes with expanded scope (faster Hormuz timeline, nuclear progress). BOE neutral. Sterling steadies. European indices lead the bid. |

|

Hawkish Hangover

FOMC weight dominates

|

35%

|

Fades from 30,059 through 29,900, tests 29,757 FOMC low. Sellers use London open as a distribution point. | Iran signing is a “sell the news” event. BOE sounds hawkish, reinforcing rate-higher message. DXY strengthens further above 100.40. Tech stays under pressure. |

|

Sideways Digest

Two forces cancel out

|

30%

|

Chops between 29,900–30,200 for most of the session. Frustrating range, no clean trend. London fades into NY handoff. | Iran catalyst is fully priced, BOE is neutral, FOMC overhang remains. No new information forces a directional decision. Low-conviction session with OpEx gamma compression keeping range tight. |

Instrument-by-Instrument Read

| Instrument | Key Level | Bias | Watch |

|---|---|---|---|

| NAS100 | 30,000 pivot / 29,757 low | Cautiously neutral | 30,200 resistance. Break above opens 30,400. Below 29,900 — bears back in control. |

| FTSE 100 | GBP reaction-dependent | Mild bullish skew | If BOE is neutral-hawkish and GBP steadies, FTSE loses its currency tailwind. Energy sector watches crude. |

| DAX | Iran energy read | Neutral | Lower energy costs are a manufacturing positive for Germany. Iran deal confirmation is quietly good for DAX industrials. |

| GBP/USD | 1.3300 support | BOE-dependent | Hawkish BOE: 1.33–1.34 recovery. Dovish BOE: break below 1.33 accelerates to 1.31–1.32. |

| Crude WTI | $75.41 / $74 support | Bearish skew | Deal formalisation = more supply certainty. No catalyst to push crude back above $78 unless signing fails. Watch $73.50 as next support. |

| Gold | $4,258 / $4,230 | Cautious | Dollar strength caps upside. Iran risk reduction removes some safe-haven premium. Watch DXY — if dollar fades, gold gets a bid. |

| Bitcoin | $64,408 / $63,000 | Risk-linked | Follows equities until decoupling. Risk-on session lifts toward $66K. Risk-off breaks $63K. |

Accenture on FOMC Day

Accenture reported earnings on Wednesday — exactly the wrong day to get attention. Earnings released on FOMC day tend to be read through a macro lens rather than on their own merits. The market was preoccupied with the Fed statement and Powell’s presser. Accenture’s numbers likely got less clean a read than they deserved.

Our read: any post-earnings reaction that didn’t fully play out Wednesday morning gets another look today. If Accenture beat and the reaction was muted due to FOMC noise, you could see a delayed move in the stock and in consultancy/IT services peers during the London session. Conversely, if the numbers were soft and got buried by macro — watch for that to catch up. IT services is a lens into corporate spending appetite, which matters to the growth story that rate hawks are questioning.

What We’re Watching This Session

Official signing expected to be covered live. Market reaction to any surprises in scope, timing, or complications will be immediate. Crude is our proxy — moves above $77 suggest the market sees a reversal risk; below $73.50 means the deal’s supply implications are being front-run further.

Expected: hold at current rate. The language is what matters. Watch Bailey’s press statement for any shift toward earlier cuts (GBP sells, FTSE rallies on currency) or confirmation of patience (GBP stabilises, sterling shorts cover). A surprise cut would be GBP negative but global risk positive — low probability.

Round numbers with options clustering matter. 30,000 is the pivot for today’s session. Above it: the overnight bounce has legs, dip buyers are in control. Below it for more than 30 minutes: the bounce was distribution, and 29,757 is back in play before Friday OpEx.

If VIX fades from 17.99 back toward 16 during the London session, that’s hedges coming off — risk appetite is returning. If VIX holds or rises above 18.5, participants are adding protection into the BOE decision and through OpEx. VIX direction is more informative than equity price alone today.

Our Read: The Bottom Line

This is not the session to build a big position into the London open and walk away. Two catalysts of roughly equal and opposing weight are landing in a market that’s already absorbed a major Fed shock. The overnight bounce is encouraging but thin — 30,059 after a hawkish Fed and a 670-point reversal this week tells us buyers exist but confidence doesn’t.

The Iran signing is an important geopolitical moment that probably reads as a confirmation rather than a catalyst. The BOE is the swing variable — not because UK rates drive US tech stocks, but because the BOE’s tone today will be read as a global signal about whether central banks are genuinely aligned on “higher for longer” or whether the Fed is out on its own.

The first 90 minutes of London trade — 07:00 to 08:30 UTC — will tell us which way the session leans. Watch crude and VIX before watching equity price.

This briefing is prepared by the Titan Macro Desk for informational purposes. Nothing published here constitutes investment advice or a recommendation to buy or sell any financial instrument. All views are analytical reads based on publicly available data at the time of publication. Market conditions can change rapidly. Past analytical accuracy is not a guarantee of future results. Capital is at risk. Please ensure you understand the risks involved before trading.

Watch this brief

More on the YouTube channel: new briefs daily. Subscribe so the next one reaches you.