Titan Macro Desk

The Fed Just Changed the Game

Post-Close Brief | Wednesday 17 June 2026 | FOMC Verdict

This is the session the whole week was building towards. Three days of positioning, de-risking and waiting — and Warsh delivered a verdict the market did not want to hear. The Fed held rates and the tone was firm enough to kill the rate-cut narrative that had been propping up the rally since Monday’s Iran euphoria. VIX spiked nearly ten percent in a single session. Gold got sold. The dollar rallied hard. Our read coming into today was patience over chasing — and that read held.

Here is everything that happened, why it happened, and what Thursday looks like from where we stand now.

The Session in Numbers

| Instrument | Close / Level | Session Move | Read |

|---|---|---|---|

| S&P 500 | 7,423 | -1.17% | Broad selling, hawkish repricing |

| Nasdaq 100 | 29,753 | -0.72% | Low 29,757 — approaching key zone |

| Dow Jones | 51,505 | -0.95% | Broad participation in the selloff |

| Russell 2000 | 2,930 | -0.31% | Small-caps relatively resilient |

| VIX | 17.99 | +9.63% | Fear spike — single-session near-10% |

| VVIX | 93.94 | +7.12% | Vol-of-vol expanding — uncertainty rising |

| Gold | $4,258 | -1.68% | Dollar strength killed the bid |

| DXY (Dollar) | 100.40 | +0.87% | Classic hawkish-Fed dollar bid |

| Crude Oil | $75.41 | -0.84% | Demand concern re-priced into crude |

| Bitcoin | $64,408 | -1.82% | Risk-off pressure extending to crypto |

| GBP/USD | 1.3300 | -1.08% | Cable hammered ahead of BOE Thursday |

The Three-Day Story

You cannot understand Wednesday without running the full three-day tape. This week had a specific character — and if you read Monday’s brief, you saw it coming.

Monday 15 June — The Euphoria Session

Indices surged roughly three percent. Iran deal headlines combined with SpaceX newsflow created a genuine risk-on burst. The session felt clean — but our read was to watch rather than chase. Markets running on geopolitical optimism one trading day before a Fed decision was not the setup to be adding risk. That view looked contrarian at the time. It looks right now.

Tuesday 16 June — The De-Risking Session

Six hundred and seventy points off the Dow. The market had second thoughts about Monday’s enthusiasm and started pricing in the possibility of a hawkish hold. We flagged the VVIX-to-VIX divergence — vol-of-vol rising faster than implied vol itself. That pattern tells you institutional desks are buying protection quietly. Tuesday confirmed it: the unwind had started before Warsh said a word.

Wednesday 17 June — The FOMC Verdict

Warsh held and the language was firm. No hint of a cut on the near horizon. The market’s read: higher for longer is not over. VIX jumps nearly ten percent. Gold — which had been holding up well as a hedge — gets sold as dollar strength kicks in. This is textbook hawkish-Fed reaction: dollar up, equities down, commodities under pressure, sterling caught in the crossfire ahead of the BOE tomorrow.

The three-day arc: euphoria, doubt, confirmation. That is a complete cycle in under seventy-two hours.

Our Calls — How Did We Do?

We keep score here. Every call, graded honestly.

| The Call | When | Verdict |

|---|---|---|

| “Patience over chasing” — do not add risk into the FOMC | Monday brief | CONFIRMED |

| VVIX expanding ahead of VIX — institutional protection being bought quietly | Tuesday brief | CONFIRMED |

| Framework on WATCHING — not a LONG entry setup | Both prior briefs | CONFIRMED |

| Gold holding pre-FOMC as FOMC-risk pricing — then sells on the actual verdict | Tuesday brief | PARTIAL |

| Correction scenario flagged at 30% probability | Monday brief | TRIGGERED |

| Options positioning would amplify the move (GEX) | Tuesday brief | CONFIRMED |

Five out of six confirmed or triggered. The partial on gold is fair — gold held as we expected pre-announcement, then sold on the hawkish read. That is not a miss, it is the second half of the trade playing out. The important point: the decision not to chase Monday’s rally saved significant exposure across this entire three-day sequence.

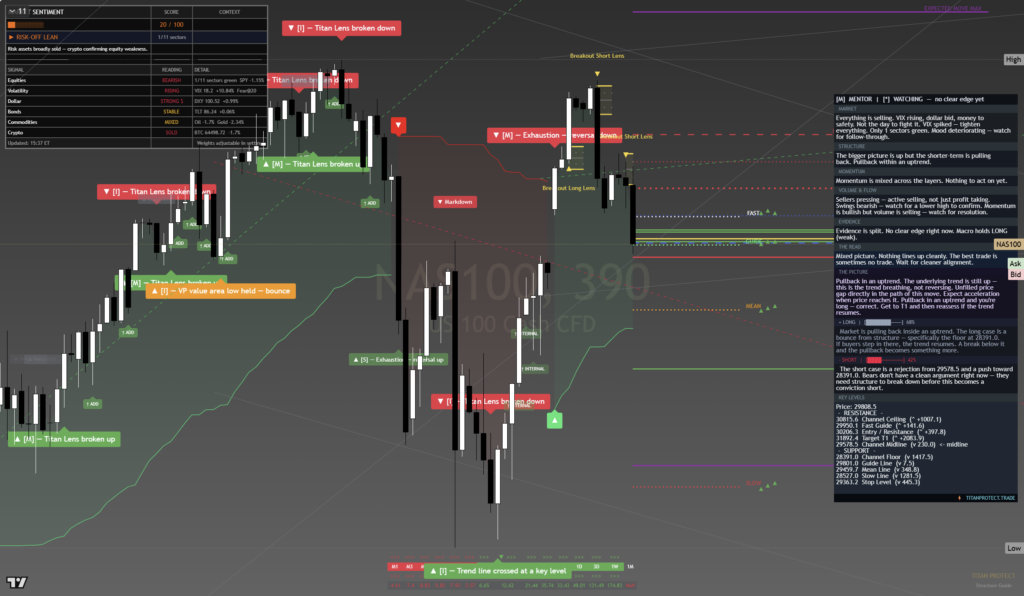

Where the Framework Stands Tonight

This is the part that matters most for anyone watching with an active position or considering one. Let us be direct about what the numbers say.

Entry Level

30,206

450pts ABOVE current price

Stop Level

29,363

~400pts below — danger zone

Target 1

31,892

Distant — not the trade today

Our Read on the Framework

The prior entry level at 30,206 is now four hundred and fifty points above where the Nasdaq is trading tonight. That is not a re-entry — that is an invalidation. You do not buy into a position where price has fallen significantly below your trigger. The more pressing question is the stop at 29,363. With NAS at 29,753, we are only around four hundred points away. If the selling continues Thursday, that level comes into play.

Our current read is that the framework should shift from WATCHING to AVOID for long entries. A SHORT scenario becomes relevant if 29,600 fails to hold on Thursday’s open — but we want to see how the Iran deal news and the BOE interact with sentiment first. Jumping to a short immediately after a hawkish-FOMC selloff is the kind of trade that gets squeezed hard on any positive catalyst.

The playbook right now: watch the 29,363 level. That is the line between a correction within the uptrend and something more structurally concerning.

Volatility — What the VIX Complex Is Telling Us

The volatility picture is worth spending time on, because it was our clearest edge coming into this session.

| VIX Metric | Prior Level | Tonight | Signal |

|---|---|---|---|

| VIX (spot) | 16.41 est. | 17.99 | Elevated but not extreme — not panic |

| VVIX (vol of vol) | 87.69 | 93.94 | Uncertainty premium still building |

| VIX3M (3-month) | 19.53 | 20.45 | Medium-term uncertainty rising |

A few things to note here. VIX at 17.99 is elevated but it is not a crisis reading. The twenty level is where you start seeing genuine fear-driven capitulation. We are not there yet. The more interesting number is VVIX at 93.94 — this measures the uncertainty around implied volatility itself. When VVIX is rising faster than VIX, it means desks are buying volatility protection but not entirely sure how much they need. That is an indecisive market, not a panicking one.

VIX3M moving from 19.53 to 20.45 is also worth watching. The three-month measure tells you whether this is viewed as a near-term shock or a longer-dated repricing. Rising VIX3M says some participants think the uncertainty extends beyond the next few weeks — which aligns with a hawkish Fed that gives no timeline on cuts.

The GEX amplification we flagged was evident in the size of the VIX move relative to the equity move. A one percent equity decline generating nearly ten percent VIX expansion is not normal — it reflects options positioning that was stretched on the long side going into FOMC, and the unwind of that positioning amplified the vol reaction. That dynamic can reverse quickly if buyers step back in.

Cross-Asset — What the Rest of the Market Is Saying

It is not just equities we read. The cross-asset picture on FOMC day gives you a much cleaner signal than any single instrument.

Gold — $4,258, down 1.68%

Gold’s behaviour today was textbook. When the Fed signals higher for longer, dollar strength follows immediately, and gold — priced in dollars — takes the hit. Our read on Tuesday was that gold was holding because it was pricing in FOMC uncertainty. Once the uncertainty resolved into a hawkish outcome, the hedge rationale evaporated and sellers moved in. The partial on our gold call was actually the trade behaving exactly as expected — the “partial” was that gold did not fall before the announcement, which was actually correct. It fell after. That is the right sequence.

Dollar (DXY) — 100.40, up 0.87%

The dollar’s rally was the most textbook reaction of the session. Hawkish Fed means higher rates for longer, which means US yields stay elevated relative to global peers, which means dollar demand. DXY punching through 100.40 puts the index back in a zone that causes ripple effects across everything priced in dollars — emerging market assets, commodities, and any company with significant dollar-denominated debt all felt the squeeze simultaneously.

GBP/USD — 1.3300, down 1.08%

Sterling’s nearly one-percent fall is partly the dollar story but also anticipation ahead of the BOE decision Thursday. If the BOE signals dovish intentions — cutting or hinting at cuts — while the Fed stays hawkish, the rate differential between the two central banks widens against sterling. Cable at 1.33 is a key level. A break below here on a dovish BOE Thursday could accelerate further. Our read for tomorrow’s BOE section will be critical for GBP holders.

Bitcoin — $64,408, down 1.82%

Bitcoin’s decline following the Fed decision reflects its growing correlation with risk assets. Higher for longer means the opportunity cost of holding non-yielding assets increases. Bitcoin has matured enough that it now behaves like a high-beta risk asset in macro-driven sessions. The dollar’s strength is an additional headwind — when the dollar rallies hard, Bitcoin tends to lag. Tonight’s level keeps it above the psychological $64,000 mark — watch that support.

Thursday Scenarios — Three Paths From Here

Tomorrow is unusually loaded. Iran deal signing is expected. BOE decision is due. OpEx is Friday. And the market needs to digest today’s hawkish verdict with fresh eyes. Here is our read on the three paths.

| Scenario | Probability | NAS100 Target Zone | Trigger |

|---|---|---|---|

| Recovery | 30% | 30,000 – 30,200 | Iran deal signed, market views it as demand-positive; geopolitical relief offsets Fed hawkishness temporarily |

| Continuation Sell | 40% | 29,363 – 29,600 | Hawkish Fed + no definitive Iran deal + BOE dovish = double macro headwind; stop zone tested |

| Stabilisation | 30% | 29,600 – 29,900 | Market absorbs Fed shock overnight, chop session develops as participants wait for Friday OpEx clarity |

The Swing Factor

The Iran deal is genuinely binary. If it signs Thursday and the imagery is credible — both parties at the table, US officials on camera — you get a short-covering rally in equities and a crude bid that can override the hawkish Fed narrative for at least one session. If it delays or the details disappoint, the continuation sell scenario becomes more likely. That single catalyst is the difference between the 30% and 40% paths tomorrow.

What Warsh Actually Signalled

Beyond the headline hold decision, the press conference gave us several things worth holding onto. This is our read on the language — not a transcript, but what the market heard and why it reacted the way it did.

The absence of a clear pivot signal was the most important element. In prior cycles, Fed chairs have used the press conference to soften hawkish decisions with dovish language — hints about being “near the peak,” or references to “data dependence” in ways that suggest cuts are around the corner. Warsh did not offer that comfort. The language remained focused on the persistence of inflation risk, and the dot plot projections apparently did not move dramatically in the dovish direction the market was hoping for.

The result: the rate-cut pricing for the second half of the year took a hit. When those expectations come out, risk assets reprice immediately. That is exactly what happened across equities, gold, and crypto simultaneously within minutes of the presser beginning.

The constructive read — if there is one — is that Warsh is managing expectations rather than signalling a fundamental change in trajectory. The Fed is still data-dependent. A run of weaker inflation prints or softer labour market data in July could shift the picture. But that is a story for next month, not tomorrow.

OpEx Friday + BOE Thursday — The Full Picture

We are heading into an OpEx on Friday with a completely different strike landscape than we had at the open of the week. Monday’s rally opened long positions at strikes that are now well above the market. Wednesday’s decline has placed price close to put-heavy territory. This matters because options dealers must hedge their books — and with price falling into heavier put concentration, you can get what is known as negative gamma feedback, where the dealer hedging activity itself amplifies moves to the downside.

The pin dynamics for Friday OpEx will depend on where price settles Thursday. If NAS finds support at 29,600-29,700 and holds, dealers may create a natural gravity towards that level into Friday close. If it breaks down further, the OpEx could accelerate selling as puts move into the money.

For the BOE: sterling’s positioning is vulnerable. If Bailey and the MPC signal a rate cut is coming in August — which is the current market expectation — that divergence from a hawkish Fed worsens the GBP/USD equation. Watch cable at 1.3250 as the next meaningful support level if the BOE disappoints sterling holders tomorrow.

The Bottom Line for Thursday

Three days. One complete cycle. Our read across all three sessions held together: patience before the FOMC, awareness of the volatility signals, and the discipline not to chase Monday’s euphoria. Those decisions compound over time — not in a single session, but across weeks and months of consistent, evidence-based positioning.

Tonight, the framework is AVOID for fresh long entries on NAS100. The 29,363 level is the line in the sand. Iran deal and BOE are the swing factors. OpEx Friday will create additional dynamics that may not reflect fundamental moves.

We will be back before Thursday’s London open with the full cross-asset read. If the Iran signing happens overnight, that changes the calculus significantly and we will update before the New York session.

Watch List for Thursday

1. Iran deal confirmation — binary event. Signed = rally candidate. Delayed = continuation sell.

2. BOE decision and language — sterling direction and GBP/USD trajectory.

3. NAS100 29,363 — if tested, this determines whether the correction stays contained.

4. VIX — does it stay elevated or begin to compress? Compression = the session is stabilising.

5. DXY 100.40 — any reversal in the dollar opens the door for gold and commodity recovery.

TITAN MACRO DESK — POST-CLOSE BRIEF

Wednesday 17 June 2026 | Published Post-Close

This brief is for information and analysis only. It does not constitute financial advice or a recommendation to buy or sell any financial instrument. Past performance of any call or scenario does not guarantee future results. Always manage risk independently.