Alpha Insights | Pre-London Brief

FOMC Aftermath Meets BOE Decision Day

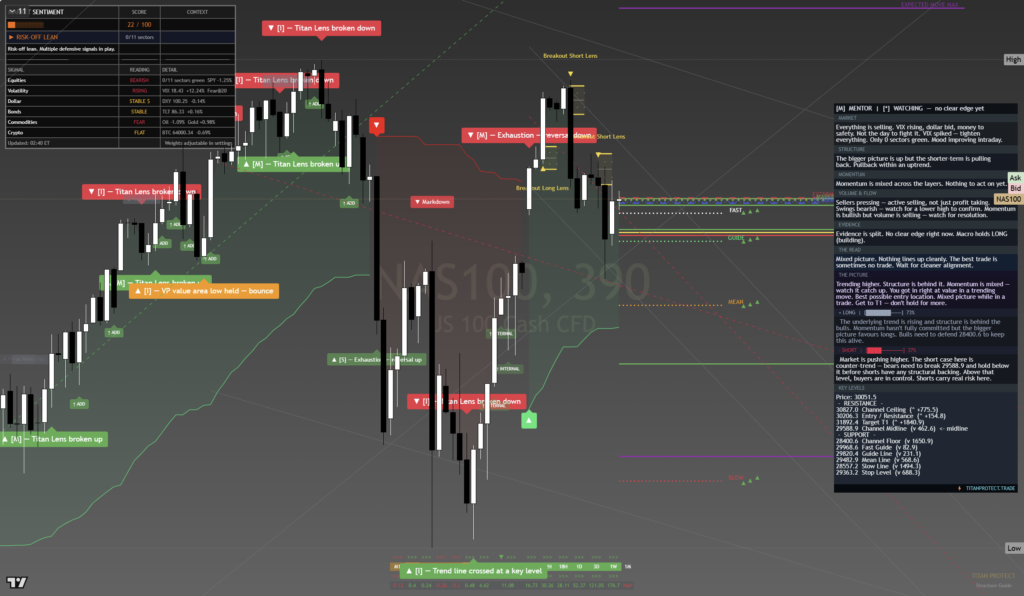

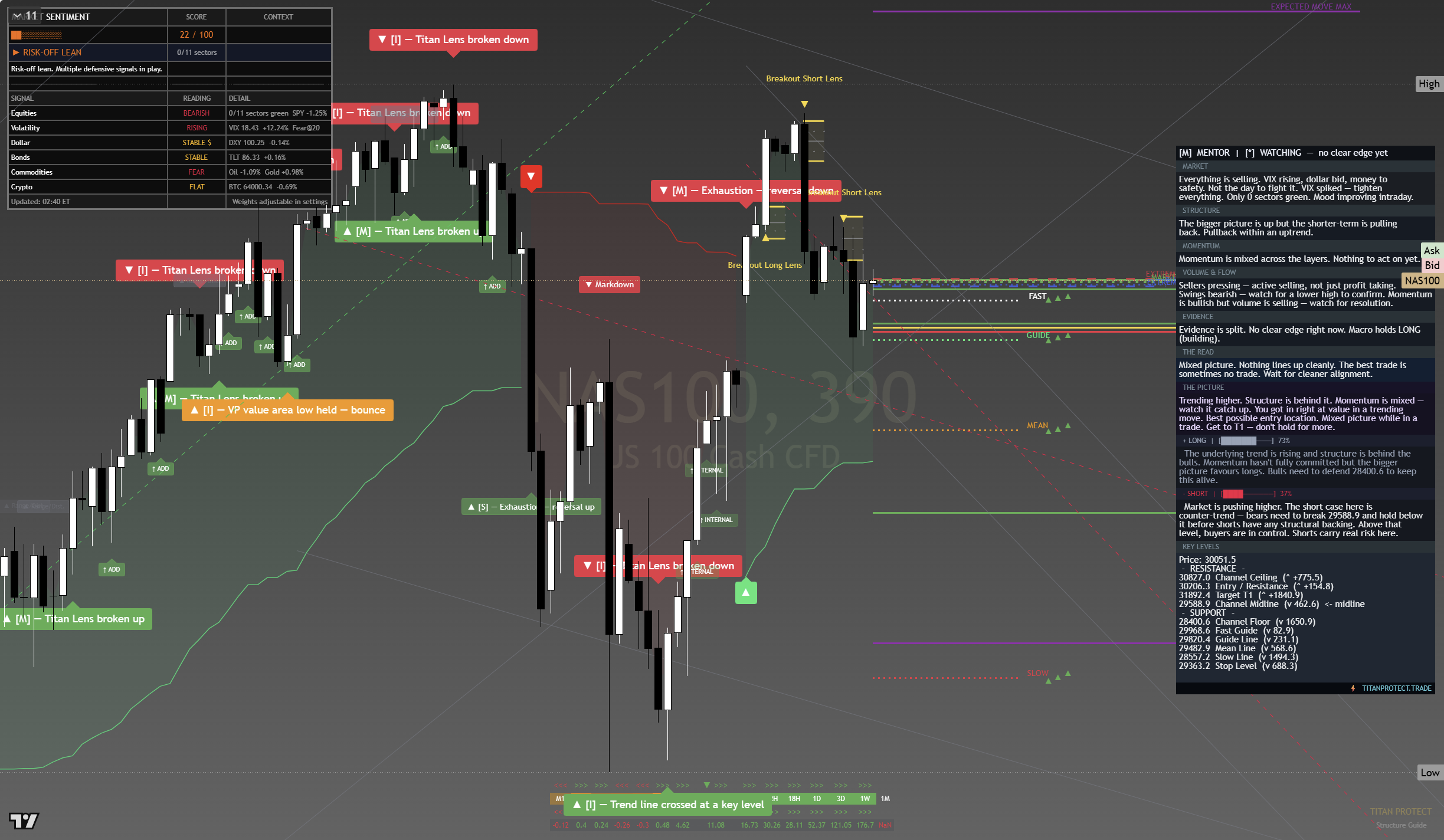

VIX Backwardation Signals Structural Stress as Markets Enter Options Expiry Week

Thursday 18 June 2026 | Data locked 06:21 UTC | Published for Elite Members

Composite Bias

Structurally cautious with selective opportunity. VIX term structure in backwardation means the near-term is priced for more stress than the medium-term — that does not resolve itself quickly. Today the BOE adds a second policy variable on top of yesterday’s Fed shock. Treat any pre-BOE rally as positioning noise, not a change of trend.

Overnight Recap — FOMC Aftermath into Asia

Wednesday delivered a hawkish hold from the Federal Reserve. Rates stayed unchanged but the accompanying language and updated projections were materially more restrictive than markets priced. VIX moved from 16.41 at the prior close to a session high of 18.84, settling at 18.44 — a move of over 12% in a single session. That tells you the options market repriced tail risk, not just day-to-day volatility.

The dollar was the primary beneficiary. DXY strength compressed Gold, pressed EUR/USD and GBP/USD lower, and confirmed the carry trade unwind into yen that pushed USD/JPY to 160.59. Crude suffered a separate shock: the Iran peace deal signing is scheduled for today, and oil markets decided to price the removal of the geopolitical risk premium rather than wait for the ceremony. WTI fell 3.45% to $74.14.

Asia overnight traded with low conviction. No material data from Japan or China. The session effectively held the FOMC marks and waited for London to provide direction. That is where we are now.

What We Called vs What Happened

Pre-London (Wed 17 Jun) Called:

- FOMC was the dominant risk event. De-risking was already in motion post-Tuesday’s 670-point Nasdaq reversal.

- GBP/USD flagged as vulnerable ahead of today’s BOE given sterling was already sold aggressively on dollar strength.

- Gold and crude identified as dual tail risk if the Fed surprised hawkish and the Iran timeline accelerated simultaneously.

What Delivered:

- Both risks triggered simultaneously. VIX +12%, Gold -0.54%, Crude -3.45%.

- SPY closed at $740.96 (-1.25%). NDX at 29,671 (-0.99%). The de-risking was orderly, not a crash.

- GBP/USD fell -0.83% to 1.3315, setting up today’s BOE as a live catalyst with a pair already under pressure.

European Session Setup

London opens into a market that has already absorbed one central bank shock. The question today is whether the BOE adds a second layer or provides relief. European indices are likely to open cautiously, tracking Wall Street’s overnight read. FTSE 100 carries dual exposure: domestic rate sensitivity via the BOE and commodity weight, specifically through energy names that face further pressure if crude continues to price the Iran deal.

DAX 40 is watching EUR/USD at 1.1527 after yesterday’s dollar-driven compression. German exporters benefit from a weaker euro but the broader equity read is risk-off, and that tends to override FX tailwinds in sessions like this one.

Euro Stoxx 50 is effectively a policy crossfire trade today — Fed hawkishness from yesterday, BOE decision at 11:00 GMT, and US data at 13:30 BST that could reprice Fed expectations again. That is three separate macro inputs in a single session. Position sizing matters more than trade direction in this environment.

Opportunity

$11B+ dark pool prints on FOMC day suggest institutional repositioning at scale. Extreme put speculation with absent call speculation is a classic contrarian setup for a relief bounce — but only if macro catalysts cooperate. Watch the BOE print closely for any dovish lean that changes the dollar narrative.

Risk

VIX term structure in backwardation (VIX 18.44 vs VIX3M 20.62) means implied volatility is pricing more near-term stress than medium-term. This is not a panic spike. It is a structural repricing. Trend-chasing longs or premature dip-buying without confirmation carries elevated risk today.

Key Levels & Tactical Bias

| Instrument | Last | Support | Resistance | Bias | Tactical Note |

|---|---|---|---|---|---|

| Nasdaq 100 (NDX) | 29,671 | 29,200 | 30,000 | Bearish | Sellers active. Multiple breakdown signals visible on higher timeframes. 29,200 is first structural support; a close below puts 28,800 in play. Call speculation absent — no buyers stepping in with conviction. |

| S&P 500 (SPY) | $740.96 | $730 / $725 | $750 | Cautious | Max pain at $725 — spot is $16 above. OpEx Friday tomorrow creates magnetic pull toward max pain into close. $750 is significant call clustering per positioning data. A $1.4B dark pool block at $750.06 confirms institutional interest at that level, not below it. |

| FTSE 100 | Watch open | 8,700 | 8,820 | Neutral | BOE hold expected but GBP weakness could benefit large-cap exporters. Energy weight is a drag given WTI -3.45%. BOE surprise in either direction is the key variable — do not commit directionally before 11:00 GMT. |

| DAX 40 | Watch open | 22,800 | 23,200 | Bearish lean | EUR/USD pressure from DXY strength is a tailwind for exporters but global risk-off is the dominant force. Watch 22,800 as near-term tell for continuation vs stabilisation. |

| Gold (XAU/USD) | $4,335 | $4,290 | $4,380 | Neutral-Bearish | Sold on hawkish FOMC and DXY strength. Gold has dual headwinds today: continued dollar strength and Iran deal removing geopolitical premium. $4,290 is immediate support — a break there opens $4,230. Any dollar softening around BOE is a tailwind. |

| Crude Oil WTI | $74.14 | $72.00 | $76.00 | Bearish | Iran deal has 95% probability of completion by end of month per prediction markets. The risk premium has been largely priced out already with Wednesday’s -3.45% move. Watch for “sell the news” if the signing goes smoothly, or a short-cover squeeze if complications emerge at the ceremony. |

| GBP/USD (Cable) | 1.3315 | 1.3260 | 1.3380 | Bearish | The most live instrument today. Down -0.83% yesterday. BOE at 11:00 GMT is a binary. A hawkish surprise (hike or hawkish hold with upgraded guidance) could trigger a sharp recovery through 1.3380. A hold with dovish language or split vote could accelerate toward 1.3200. Do not fade the initial BOE move without confirmation. |

| EUR/USD | 1.1527 | 1.1470 | 1.1600 | Bearish lean | DXY rally from hawkish Fed is the primary driver. Eurozone macro is thin today — the pair follows the dollar narrative. US Jobless Claims at 13:30 BST is next repricing event for this cross. |

Economic Calendar — Three-Timezone View

| Event | NY (ET) | London (BST) | Tokyo (JST) | Impact |

|---|---|---|---|---|

| BOE Rate Decision + Statement | 06:00 ET | 11:00 BST | 19:00 JST | HIGH |

| BOE Governor Bailey Press Conference | 06:30 ET | 11:30 BST | 19:30 JST | HIGH |

| Iran Deal Signing Ceremony | TBC | TBC | TBC | HIGH |

| US Initial Jobless Claims | 08:30 ET | 13:30 BST | 21:30 JST | MED |

| US Housing Starts & Building Permits | 08:30 ET | 13:30 BST | 21:30 JST | MED |

| Philadelphia Fed Manufacturing Index | 08:30 ET | 13:30 BST | 21:30 JST | MED |

| Accenture (ACN) Earnings — Before Open | Pre-market | Pre-open | Overnight | MED |

The 13:30 BST US data trio (Jobless Claims + Housing + Philly Fed) is a macro crossfire point. Weak claims would push back against the hawkish Fed read and could trigger a short-covering rally. Strong claims confirm the labour market is not yet breaking and supports the Fed’s patient stance.

Geopolitical Watch

Iran Deal Signing

Prediction markets put the probability of the deal holding through 30 June at 95%. That is a high-conviction read but also one that means most of the risk premium has already left crude prices. Wednesday’s -3.45% WTI move priced a significant portion of the peace dividend. Today’s ceremony is watched for complications, not confirmation. Any breakdown in negotiations would produce a violent short-squeeze in crude energy names — this is a tail risk, not a base case. The base case is continued gentle selling in WTI as the deal removes the geopolitical ceiling on Iranian supply.

US Monetary Policy Architecture — Structural Signal

Reports that senior Federal Reserve officials are standing up a task force reviewing five areas of monetary policy framework suggest the current approach is under review. This is not a near-term rate story. It is a longer-cycle signal. Markets that have been anchored to a particular Fed reaction function may need to reprice over coming months. Record global government bond issuance of $504 billion in H1 2026 is the fiscal backdrop against which this is playing out. Rates staying higher for longer against a backdrop of aggressive supply is the scenario this sets up. Watch this space.

Options Context — Positioning & OpEx Friday Setup

SPY Max Pain

$725

Spot $16 above

QQQ Max Pain

$690

Gravity into OpEx

Dark Pool Prints

$11B+

Institutional scale

VVIX/VIX Ratio

5.13

Elevated vol-of-vol

The options picture has three distinct signals today. First, max pain gravity: SPY at $740.96 sits $16 above its $725 max pain level. With OpEx tomorrow, market makers face incremental pressure to defend or reposition around that level. This creates a mechanical pull lower that is independent of fundamental news.

Second, the positioning asymmetry: put speculator activity is at an extreme with call speculation absent. This is contrarian bullish in isolation — it reflects overcrowding on the bearish side. But it only converts to a bounce when there is a catalyst to squeeze those puts. The BOE or the US data at 13:30 BST could both serve that function.

Third, the dark pool context: a $1.4 billion block at SPY $750.06 represents institutional positioning at resistance, not at support. Large players are not stepping in as buyers below the market. That is a meaningful read — they chose $750 as their reference level, which remains $9 above spot. SPX call clustering at 7,600+ is where the upside is being sold, not where it is being bought.

OpEx Friday Positioning Note

Monthly options expiration tomorrow means today is the final positioning day. Dealers will be hedging gamma through the European afternoon and into the US open. Expect elevated intraday volatility in the final two hours of the US session today as desks square positions ahead of expiry. This is not a market where end-of-day moves should be read as clean signals.

Earnings Preview — ACN, KR, TSCDY

| Company | Timing | What to Watch | Market Implication |

|---|---|---|---|

| Accenture (ACN) | Before market open | AI and cloud services demand; guidance for FY2026 full year; any mention of client budget caution post-macro uncertainty. | ACN is a bellwether for enterprise tech spending. Strong results validate the AI investment cycle and could provide a tailwind to tech-heavy indices in an otherwise risk-off session. |

| Kroger (KR) | Before market open | Same-store sales growth; margin compression from food inflation; consumer trading-down behaviour. | Grocery retail is a defensive read on consumer health. Weak comps would reinforce the “consumer slowing” narrative and add to the bearish macro backdrop the Fed is monitoring. |

| Tesco (TSCDY) | UK trading update | UK grocery volumes; price investment vs margin; any read on post-BOE consumer sensitivity. | Directly relevant to FTSE 100 and the UK consumer picture. A strong Tesco trading statement ahead of the BOE creates an interesting cross-read on domestic UK economic health. |

Multi-Strategy Approach

Scalping (under 15 min)

Two windows: the BOE reaction at 11:00 BST and the US data print at 13:30 BST. Outside those windows the environment is choppy with no clean directional bias. Fade the first move only with tight confirmation. GBP/USD is the cleanest instrument for the BOE window — 20-30 pip moves likely on the initial print.

Position sizing: REDUCED

Intraday (1-4 hours)

Wait for BOE confirmation before committing. If the BOE holds with hawkish language: short GBP/USD toward 1.3260, long DXY exposure via short EUR/USD. If BOE surprises with a cut or split vote showing dove majority: long GBP/USD to 1.3380, watch Gold for dollar reversal opportunity. Entry/stop discipline is critical — entry near 1.3315, stop above 1.3370 or below 1.3280 depending on direction. Target: 60-80 pip move in the two hours post-BOE.

Position sizing: STANDARD

Swing (2-5 days)

The 3-day narrative arc from Monday euphoria to Wednesday hawkish shock argues for a period of digestion, not a straight recovery. Swing longs in equity indices carry the risk of OpEx gamma drag tomorrow and the structural VIX backwardation signal. More attractive to look at swing shorts in crude given the Iran deal momentum, with a defined stop above $76.50. Risk around 3.3%, reward targeting $70.00 — approximately 5.6% — gives an R:R of roughly 1.7:1.

Position sizing: STANDARD

Positional (weeks)

The macro backdrop has shifted. Hawkish Fed plus backwardation VIX term structure plus $504B bond issuance globally equals a structurally more expensive cost of capital environment. This argues against adding new long equity risk at current levels. The SpaceX IPO filing and continuing AI flow into specific names (evidenced by unusual options activity) keeps selective individual name exposure valid. Broad index exposure should be REDUCED until the VIX term structure normalises back into contango.

Position sizing: REDUCED (indices) / MAX (selective single names)

Scenario Analysis — Today’s Session

| Scenario | Probability | Trigger | Market Read |

|---|---|---|---|

| Relief Rally | 25% | BOE hawkish surprise + Iran deal smooth + US data beats. Dollar softens, equities recover half of Wednesday’s losses. | GBP/USD to 1.3400+, NDX tests 30,000, Gold steady at $4,340+. |

| Sideways Chop | 40% | BOE holds as expected with neutral tone. Iran deal proceeds without drama. US data in-line. OpEx positioning dominates. | Ranges narrow. GBP/USD 1.3280-1.3350. SPY 738-745. Max pain gravity builds into Friday. |

| Continuation Lower | 28% | BOE dovish split vote or language + weak US data + Iran complications. Dollar extends gains, puts get squeezed, not covered. | GBP/USD to 1.3200, SPY test $730 (near max pain), Gold below $4,290, VIX re-tests 18.84. |

| Black Swan | 7% | Iran deal collapses publicly at ceremony, or surprise emergency Fed communication, or major earnings shock (ACN miss of over 20%). | VIX spike through 22, crude +5%, equities -2%+ in a session. Safe-haven rotation into JPY and Gold. |

Probabilities are analytical assessments, not forecasts. They sum to 100%.

Session Risk Assessment

Session Risk: Around 65%

Three factors drive this elevated reading: (1) dual central bank policy uncertainty with BOE on top of FOMC aftermath, (2) VIX term structure in backwardation signalling near-term stress is not yet resolved, (3) OpEx tomorrow creating mechanical gamma pressure that amplifies any directional move. This is a session to execute on existing theses, not to open new directional risk without clear confirmation.

Position Sizing Guide for Today

REDUCED — all new risk until after 13:30 BST

STANDARD — post-BOE confirmed FX setups

MAX — only high-confluence setups post US data

Guidance by Experience Level

Beginner

Today is a watching session, not a trading session. Three major catalysts hit between now and 13:30 BST. The market does not owe you clarity before all three resolve. If you must act, keep size at minimum. Write down what you expect to happen with the BOE before the announcement, then compare. That exercise teaches you more than any trade you put on today. The FOMC aftermath does not mean markets go in one straight line — they chop, reverse, and then move. Learning to read that chop is the skill that separates those who last from those who do not.

Intermediate

The BOE is your primary focus. Have your levels pre-mapped: GBP/USD 1.3260 support, 1.3380 resistance. Know your scenario — if BOE is hawkish, what is your entry, what is your stop, what is your first target. Pre-plan removes emotional decision-making in the moment of the announcement. Avoid multi-instrument exposure simultaneously around the BOE print. One instrument, one clean read. The US data at 13:30 BST is a second window if you miss or pass on the BOE setup. Both opportunities do not need to be taken.

Advanced

The contrarian structure is worth monitoring: extreme put speculation without corresponding call buyers, combined with a VIX that is elevated but not in panic territory, suggests the market has absorbed the shock in an orderly way. Orderly repricing that reaches extreme put positioning levels has historically resolved in sharp short-covering rallies. The trigger here is a risk-positive BOE or strong US data. If neither materialises today, the OpEx gamma dynamic tomorrow becomes the next test. Watch whether SPY can hold $736-738 into the US close today — that level will determine whether max pain gravity at $725 becomes a real risk into expiry or whether positioning ratchets back toward $750. Delta hedging flows through the afternoon will give you the answer in real time.

Upcoming Alpha Insights Coverage

Following today’s BOE decision and the Iran deal ceremony, the research desk is tracking several threads worth your attention:

- A deep-read on what VIX term structure backwardation has historically signalled for equity returns over the subsequent 10 trading days — coming in this week’s institutional research tier.

- The Iran deal sector rotation map: energy out, which sectors attract the capital. The historical precedent from the 2015 JCPOA is instructive and that analysis is in preparation.

- OpEx expiration day analysis for tomorrow — the full gamma squeeze and pin risk map will publish pre-market Friday.

- The BOE decision will be analysed in today’s Post-Close briefing alongside the full US session read. Elite members receive the combined read before midnight.

Important Information

This briefing is produced by the Titan Macro Desk and is intended for information and educational purposes only. Nothing in this document constitutes financial advice, a solicitation, or a recommendation to buy or sell any financial instrument. All levels, scenarios, and analytical assessments represent the views of the research team at the time of publication and may change without notice. Past performance referenced in any analysis is not indicative of future results. Trading financial instruments carries a high level of risk. You should only trade with capital you can afford to lose. Seek independent financial advice if you are unsure whether trading is appropriate for you. Titan Protect Alpha Insights is published for members under terms agreed at the point of subscription.

Titan Protect Alpha Insights

Pre-London Brief | Thursday 18 June 2026 | Data locked 06:21 UTC | Titan Macro Desk