Basis Edge | Tuesday 21 April 2026 | Published 22:00 London / 17:00 New York / 07:00 Tokyo

Monday’s contango held through the geopolitical gap and rewarded those who trusted it. Tuesday was a different test. The Nasdaq 100 (NQ) dropped 181 points, VIX pushed above 20, and institutions stepped back from the tape. The question for the basis structure is simple: did the forward curve still price higher values, or did the selling crack the carry trade? The answer is nuanced and matters more than any headline tonight.

Equity contango narrowed. It did not collapse. The spread between futures and cash on the S&P 500 (ES) compressed from Monday’s 3.5% annualised to approximately 2.8%. On the Nasdaq 100, it dropped from 3.8% to around 3.1%. This is significant because contango narrowing without inversion means the market still prices higher forward values but with less conviction. Institutions are not betting on a crash. They are betting on uncertainty.

What We Called vs What Happened

| Call (Monday) | Result | Verdict |

|---|---|---|

| Equity contango healthy (3.5-3.8% carry) | Contango narrowed to 2.8-3.1% but held. No inversion | CONFIRMED |

| Crude backwardation deepening | Crude surged +2.39%. Front-month premium expanded further | CONFIRMED |

| VIX contango ~2.5pts | Compressed to ~1.8pts with VIX crossing 20. Approaching caution zone | WATCHING |

| Gold contango normal | Gold dropped -2.29%. Futures premium compressed as spot sold hard | PARTIALLY CONFIRMED |

Track record: 2.5/4. Running accuracy: 42.5/45 over 2 weeks. The VIX contango compression is the one to watch. If it inverts, everything changes.

Basis Dashboard

| Instrument | Structure | Spread | Carry (Annualised) | Change vs Mon | Signal |

|---|---|---|---|---|---|

| S&P 500 (ES) | Contango | ES vs SPY $704.19 | ~2.8% | -0.7% | Still bullish but weakening |

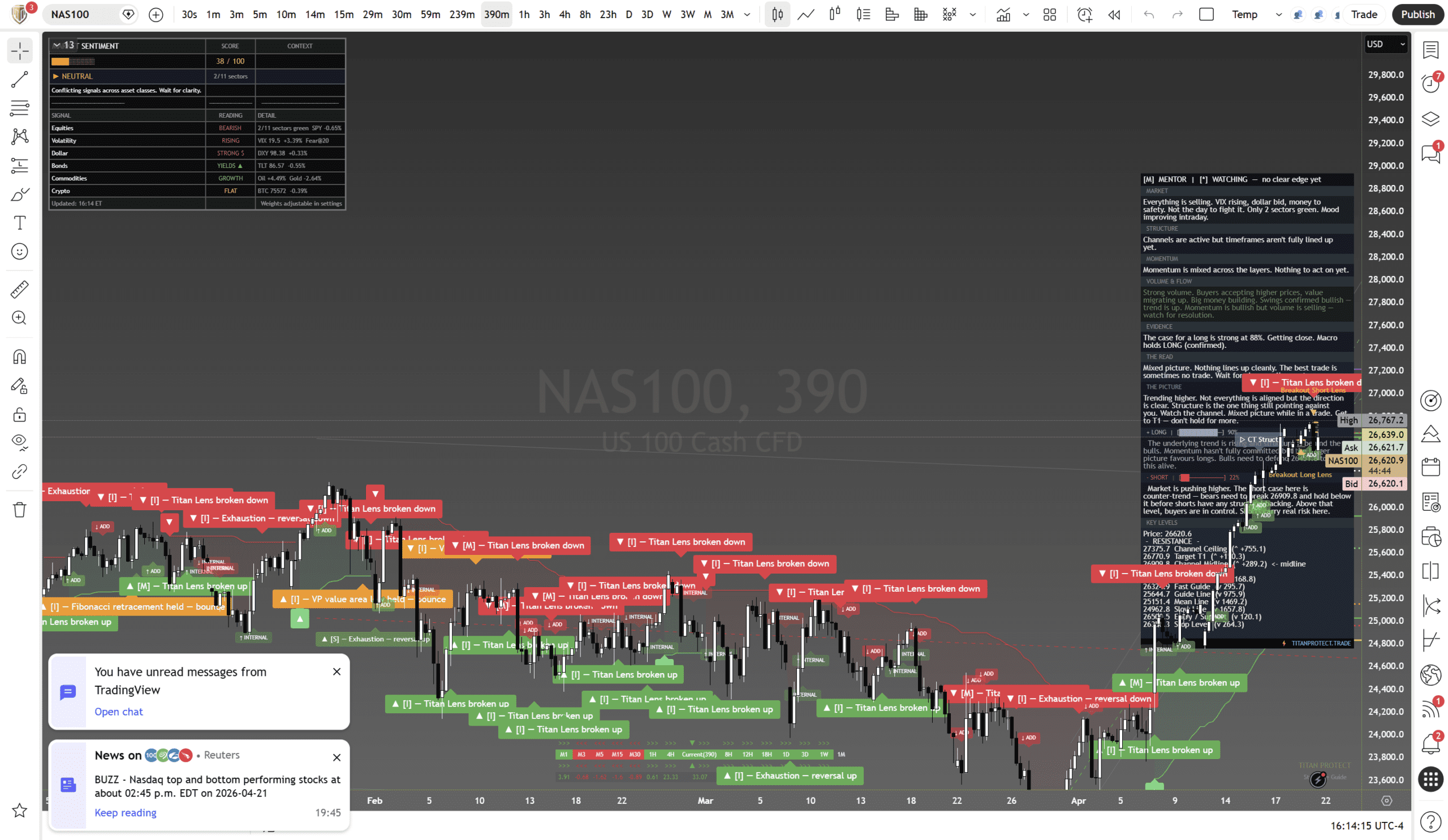

| Nasdaq 100 (NQ) | Contango | NQ 26,620 vs cash | ~3.1% | -0.7% | Weakening but intact |

| Crude Oil (CL) | Backwardation | Front premium widening | Negative carry | Deepening | Supply premium accelerating at $91.75 |

| Gold (GC) | Contango | GC vs spot $4,696 | ~0.8% | -0.4% | Compressed. Profit-taking hit spot harder than futures |

| VIX | Contango | ~1.8pts | n/a | -0.7pts | CAUTION. Compression accelerating. Inversion watch |

| Bitcoin (BTC) | Mild contango | Futures slight premium | ~1.8% | -0.2% | Flat. Crypto basis unaffected |

| Bonds (ZN) | Slight backwardation | Minimal | n/a | Shifted | TLT -0.55%. Yield rising = bonds repricing |

The VIX Contango Compression

This is the single most important basis signal today. On Monday, VIX contango was approximately 2.5 points between the front and second month. Tuesday compressed that to around 1.8 points. The pace of compression tells you how quickly the options market is repricing near-term risk relative to longer-term expectations.

Why it matters: VIX contango inversion (spot above the second month) has preceded every significant equity decline in the past two years. We are not inverted yet. But we have gone from 2.9 points on Friday to 1.8 points on Tuesday. That is a 38% compression in two sessions. If Wednesday’s GOOGL earnings and Flash PMI disappoint simultaneously, the remaining 1.8 points could evaporate in hours.

As our Volatility Lens brief covered, VIX crossed 20 for the first time in three weeks. The basis structure is confirming what the spot VIX is telling you: the market is transitioning from complacency to caution. Not panic. Caution. The distinction is everything for position sizing.

Crude Backwardation and the Supply Premium

Crude oil’s basis structure is now the most distorted in the complex. The front month trades at a widening premium over deferred months. This backwardation deepened further on Tuesday as crude surged 2.39% to $91.75. Our Positioning Pressure brief flagged the conflict: institutional positioning is short (COT -40K) but geopolitical headlines are driving price higher. The basis structure confirms the headlines are winning.

For traders, this creates a specific cost problem. If you are short crude futures, the backwardation means you pay carry every day. The roll cost from front to second month is negative. You are paying to hold a losing position. This is why positioning-vs-headline conflicts in commodities are so dangerous. Even if you are directionally correct long-term, the carry cost can bleed your account dry before the trade works.

The Carry Trade – Updated

| Position | Mon Carry | Tue Carry | Implication |

|---|---|---|---|

| Long NAS100 futures | +3.8% | +3.1% | Still earning carry but less edge. Reduced conviction |

| Long S&P 500 futures | +3.5% | +2.8% | Declining. Matches dark pool hesitation |

| Long Gold futures | +1.2% | +0.8% | Compressed. Wait for $4,650 test before re-entering carry trade |

| Short Crude futures | Negative | More negative | DO NOT short crude futures. Carry cost is punitive |

| Long VIX futures | Negative | Less negative | Contango compression means VIX hedges bleed less. Hedging cost improving |

Strategy by Timeframe

Scalping (1-5 min)

- Basis irrelevant at this timeframe. Trade levels, not carry

Intraday (15 min – 4 hr)

- NQ futures longs still have a mild carry tailwind. Shorts face a headwind. Edge has shrunk from Monday

- Crude intraday: front-month premium means longs are structurally favoured over shorts

Swing (1-5 days)

- Equity carry trade is still positive but the edge is shrinking. If contango narrows further on Wednesday, the carry advantage becomes negligible

- Gold carry trade is paused. Wait for spot to stabilise before re-entering. The -2.29% selloff distorted the basis temporarily

- VIX hedges are now cheaper to hold. If you need portfolio protection, the contango bleed is 30% less than it was Friday

Positional (weeks-months)

- The contango structure remains intact across equities. This favours long-term bulls. The 91% structural reading from our positioning analysis is consistent with a market that still prices forward optimism

- Watch the VIX term structure closely. If the remaining 1.8 points of contango compress to below 1 point, it signals the market is pricing near-term risk equal to medium-term risk. That is the warning shot before inversion

Scenario Analysis

| Scenario | Probability | Basis Implication |

|---|---|---|

| Earnings beat + PMI above 50 | 25% | Contango widens back toward 3.5-4%. VIX term structure recovers. Carry trade fully reinstated |

| Mixed results | 35% | Contango holds 2.5-3%. Current compression stabilises. Wait-and-see for Friday |

| Earnings disappoint, PMI soft | 25% | VIX contango compresses below 1pt. Equity contango drops to 2%. Carry advantage minimal |

| VIX term structure inverts | 15% | Regime change. All carry trades off. Cash is king until contango returns |

Risk Assessment

Domain risk: Around 50% (moderate)

- VIX contango compression: The fastest 3-session compression this month. From 2.9 to 1.8 points. Inversion risk is real if Wednesday disappoints

- Equity carry declining: Still positive, but the shrinking edge means the market’s conviction in forward growth is fading

- Crude backwardation: Creates a cost trap for shorts. Do not fight the basis structure in commodities

- Bond shift: TLT -0.55% and a slight move toward backwardation signals rising yield expectations. This pressures equity valuations

Cross-References

The basis compression aligns with our Positioning Pressure finding that dark pool volume dropped 31% and the regime shifted from Accumulation to Hesitation. The forward curve is telling the same story as the flow data: institutions are not selling, but they are not committing either. Our Macro Pulse brief highlighted dollar strength (+0.51%) and rising yields as the macro drivers. Both of these directly compress the equity carry trade because higher rates reduce the forward premium. And the Sentiment Lens showed Fear and Greed dropping from 69 to 38, approaching the contrarian zone. If sentiment reaches extreme fear while contango holds, that is historically the best entry point for carry trades.

This is analysis, not financial advice. Always manage your risk.

Deepen Your Understanding

Related articles from the Titan Protect Foundry: