Market Moves | Tuesday 21 April 2026 | Published 22:00 London / 17:00 New York / 07:00 Tokyo

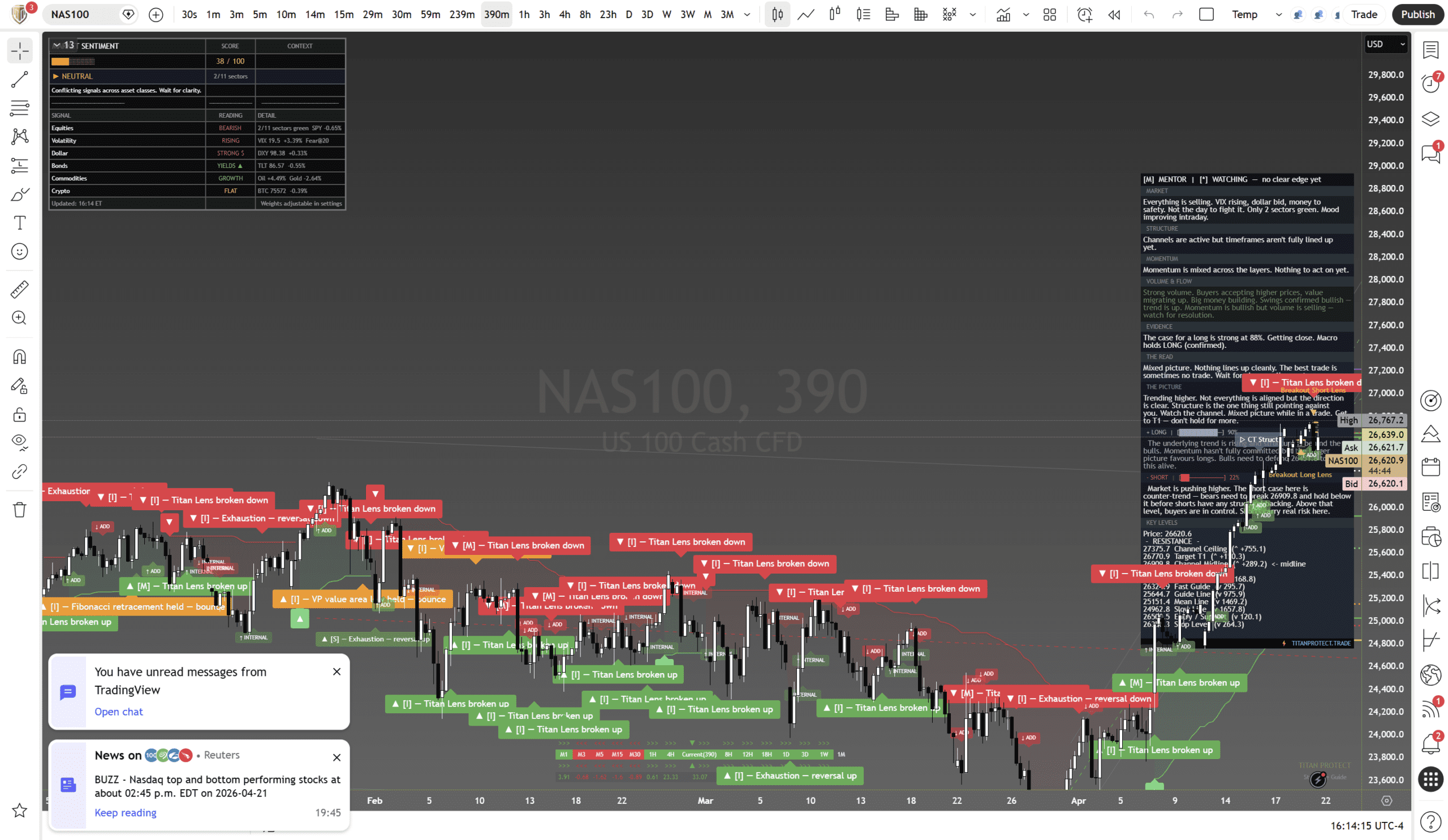

Tuesday’s market had one story: everything sold except the dollar. Equities, gold, silver, crypto. All red. The S&P 500 (SPY) dropped 0.64%. The Nasdaq 100 (NQ) lost 181 points to close at 26,620. The Russell 2000 (IWM) was hit hardest at -1.02%. Gold gave back 2.29%. Silver was hammered, down 5.39%. Even Bitcoin, supposedly the uncorrelated asset, slipped 0.34%.

Meanwhile, the dollar gained 0.51%. Crude oil rose 2.39% on geopolitical premium. And one mega-cap name finished green: Microsoft (MSFT), up 1.46%. That is not a coincidence. That is the entire narrative of Tuesday condensed into a single data point. When everything sells and one name rises, you are watching institutional rotation in real time.

What the Market Cared About

1. The Fear Collapse

Fear and Greed crashed from 69 to 38 in a single session. That is the fastest sentiment reversal we have tracked this month. As our Sentiment Shift brief detailed, this kind of collapse does not happen because of one bad day. It happens because the crowd was complacent at 69 and the rug got pulled. Monday’s 8/8 session lulled people into thinking the trend was bulletproof. Tuesday proved it is not.

The practical consequence: retail positioning flipped from greedy to fearful overnight. That creates forced selling in the short term but sets up better entries for patient capital. The institutions, as our Positioning Pressure work showed, are not panicking. They are simply waiting.

2. The Triple Sell-Off

Equities, gold, and silver selling simultaneously is unusual. Normally, gold acts as a hedge when equities fall. When both sell together, it means one of two things: either there is a liquidity event forcing liquidation across asset classes, or the dollar is squeezing everything denominated in it.

Tuesday was the second. DXY gained 0.51%, its strongest session in two weeks. As our Macro Pulse coverage explained, dollar strength compresses everything else. Gold at -2.29% and silver at -5.39% are not bearish signals for precious metals. They are the mechanical consequence of a dollar bounce. The underlying trend in gold remains structurally intact.

3. VIX Crossed 20

This is the threshold that separates a benign market from a stressed one. On Monday, VIX sat below 20 and the options market was relaxed. On Tuesday, VIX pushed to 20.29 and the entire risk surface repriced. Our Volatility Lens analysis detailed the mechanics: once VIX crosses 20, dealers adjust their hedges, gamma exposure shifts, and the market becomes more reactive to news. This is not fear. This is the machine recalibrating.

The combination matters: F&G from 69 to 38, VIX above 20, dollar surging, gold selling, and 9 of 11 sectors red. This is not a one-factor story. This is a synchronised de-risk. The last time we saw this pattern was early March, and the market found a floor within 48 hours. The question is whether earnings provide the catalyst to do it again.

Sector Scorecard

| Sector | Performance | Narrative |

|---|---|---|

| Energy | GREEN | Crude +2.39% on geopolitical premium. Only sector bid alongside dollar |

| Utilities | GREEN | Classic defensive rotation. When 9 sectors sell, money hides in yield |

| Technology | RED | QQQ -0.38%. But MSFT +1.46% masked deeper weakness in AAPL -2.52%, TSLA -1.55% |

| Consumer Discretionary | RED | TSLA earnings fear, general risk-off |

| Financials | RED | Rising yields help margins but hurt sentiment. Visa Wednesday is the test |

| Small Caps (IWM) | -1.02% | Worst index performer. Classic risk-off sequencing. Small caps sell first |

Only 2 of 11 sectors finished green. That is the narrowest breadth reading since early April. As our Sector Flow analysis covered, when breadth compresses this sharply after a strong Monday (8/8), the market is telling you it was overextended. The correction is rotational, not structural. But it can go further if Wednesday’s events disappoint.

The MSFT Signal

Microsoft gaining 1.46% on a day when SPY lost 0.64% is not noise. It is the loudest signal of the session. As our Institutional Flow brief documented, MSFT dark pool volume increased 15% day-over-day while broad index dark pool volume dropped 31%. Block buying continued for a second consecutive session. Average order size increased.

When institutions reduce broad exposure but increase specific-name exposure on a risk-off day, they are telling you exactly where they want to be when the dust settles. They are not betting on the market. They are betting on Microsoft specifically. That conviction through weakness is the clearest institutional signal of the week.

Commodities: The Dollar Did This

Gold dropping 2.29% and silver plunging 5.39% on the same day equities sold looks alarming. It is not. Both are priced in dollars. When DXY gains 0.51% in a single session, everything denominated in dollars reprices mechanically. As our Raw Materials brief explained, the underlying demand structure for gold has not changed. Crowded longs took profit into dollar strength. That is positioning, not a trend change.

Crude oil moving against the tide, up 2.39% to $91.75, confirms this is a dollar story, not a growth story. Crude is bid on Strait of Hormuz headline risk. That geopolitical premium overrides all other positioning signals. Our Positioning Pressure work flagged crude as an AVOID because the conflict between bearish positioning and bullish headlines is unresolvable. That call stands.

What the Market Did Not Care About

- Bitcoin: Down 0.34%. Effectively flat. Crypto is decorrelating but not leading. Nobody is looking to BTC for direction right now. As our Digital Flow analysis noted, thin positioning and 0.72 SPY correlation make crypto a follower, not a catalyst

- Bond volatility: TLT moved but not dramatically. The yield curve shift is gradual, not crisis-level. This is repricing, not panic

- Geopolitics outside crude: The Hormuz premium is priced into energy. The broader geopolitical backdrop is not driving equity flows today. Earnings fear is doing that job alone

Wednesday Preview

The narrative shifts to GOOGL earnings + Flash PMI. These two events will determine whether Tuesday was a one-day correction or the start of something more sustained. If GOOGL beats and PMI holds above 50, the fear from Tuesday gets unwound quickly and the institutional buyers who are waiting step back in. If either disappoints, the channel floor at 26,447 gets tested and VIX probably pushes above 22.

The market is coiled. Sentiment collapsed, volatility expanded, and the biggest earnings prints of the week are still ahead. Tuesday was the setup. Wednesday is the trigger.

Risk Assessment

Narrative risk: Around 60% (elevated)

The narrative drivers are stacking. Dollar strength, sentiment collapse, volatility expansion, and earnings uncertainty are all pulling in the same direction: risk-off. The single counterweight is the structural long-term trend which remains 91% bullish. That tension between short-term fear and long-term structure is what makes the next 48 hours so important.

Cross-References

The triple sell-off pattern was first identified in our Macro Pulse brief (Post 01). The dollar strength mechanics that drove gold and silver lower were detailed in FX Focus (Post 11). The sector breadth compression from 8/8 to 2/11 was covered in Sector Flow (Post 09). And the institutional rotation into MSFT, the single most important flow signal of the day, was documented across Positioning Pressure (Post 00) and Institutional Flow (Post 07). Read those before Wednesday opens.

This is analysis, not financial advice. Always manage your risk.

Deepen Your Understanding

Related articles from the Titan Protect Foundry: