Macro Pulse | Tuesday 21 April 2026 | Published 23:00 London / 18:00 New York / 08:00 Tokyo

Three things happened on Tuesday that matter more than the 181-point Nasdaq decline. First, the dollar strengthened 0.51%. Second, bonds sold off with TLT down 0.55%. Third, gold dropped 2.29%. When equities, bonds, and gold all sell simultaneously while the dollar rises, the macro message is unambiguous: the world is repricing risk and moving to cash. This is not a rotation. This is a de-risking event.

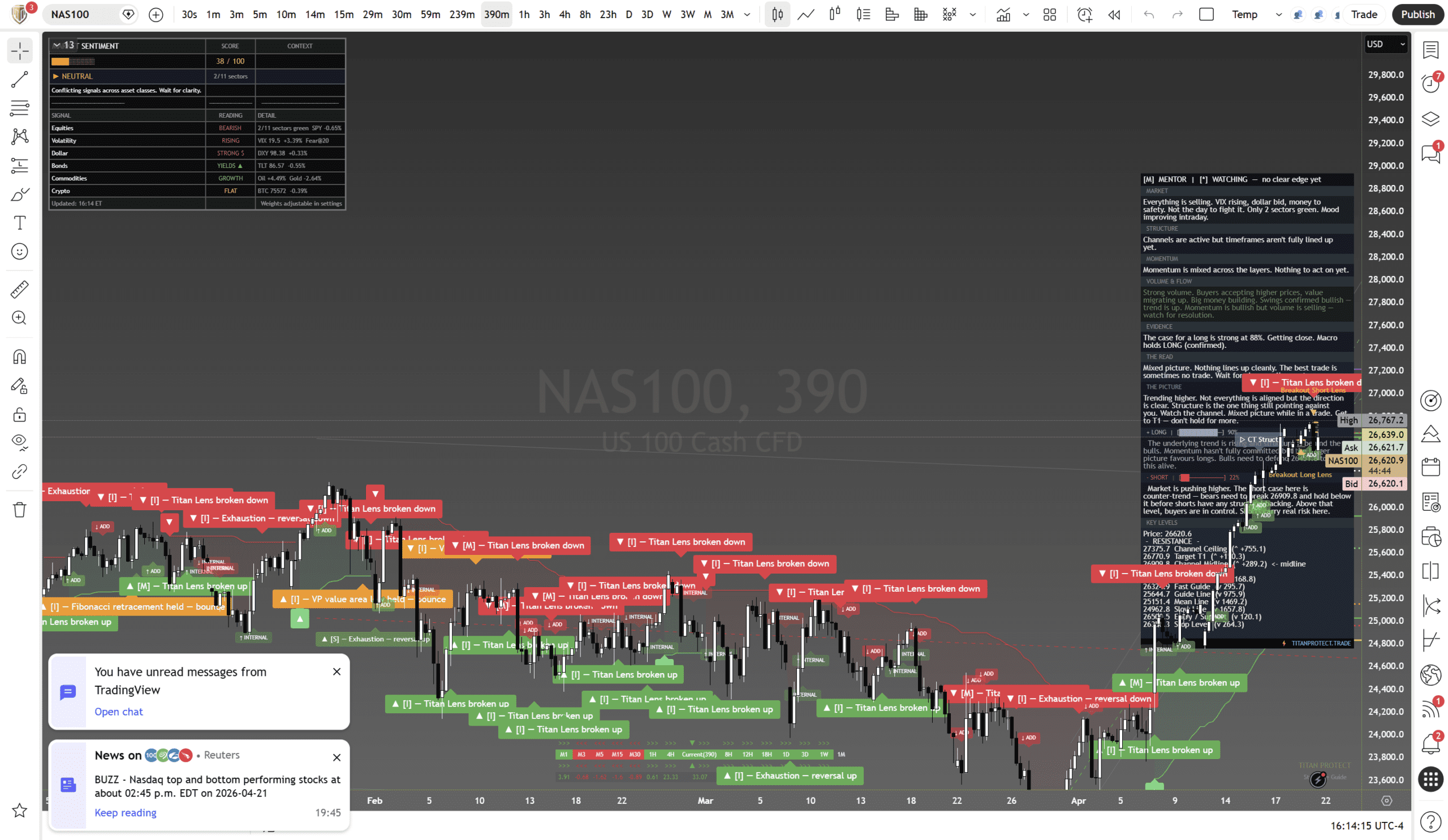

Monday’s 6/8 bullish cross-asset reading has compressed to 3/8 in a single session. That is the fastest deterioration we have tracked since this analysis began. The macro framework still reads 91% structural bullish on the long timeframe, but the short-term picture has flipped. As you will find in our Positioning Pressure brief, the institutional dark pool volume dropped 31% today. The macro data tells you why: the risk/reward of holding through Wednesday’s GOOGL earnings and Flash PMI does not justify the exposure.

What We Called vs What Happened

| Call (Monday) | Result | Verdict |

|---|---|---|

| 6/8 cross-asset bullish. Late-cycle expansion | Compressed to 3/8. Equities, gold, bonds all sold. Dollar strong | DETERIORATED |

| Earnings are the catalyst. BOJ is the risk | TSLA tonight, GOOGL tomorrow. Market pre-positioning for event risk | CONFIRMED |

| Dollar structural short below DXY 100 | DXY rallied +0.51%. Structural thesis intact but short-term reversal | TESTING |

| Gold triple tailwind (rates + dollar + geopolitics) | Gold -2.29%. Dollar tailwind reversed to headwind. Profit-taking | PARTIAL |

| Wage divergence favours quality growth + metals | MSFT +1.46%, AMZN +0.66%. Quality held. Gold did not | PARTIAL |

Track record: 1 confirmed, 1 deteriorated, 2 partial, 1 testing. Running accuracy: 17/21 over 2 weeks. Today is the first session where the macro picture materially shifted against us. The honest read: we called Monday right and Tuesday caught us mid-transition.

Cross-Asset Macro Dashboard

| Asset Class | Mon Signal | Tue Signal | Tuesday Close | Macro Read |

|---|---|---|---|---|

| US Equities (NQ) | Bullish | Neutral | 26,620 (-181) | Structural lens broken. Above channel floor. Watching |

| US Equities (SPY) | Neutral | Bearish | $704.19 (-0.64%) | Below max pain. Broad weakness. Small caps worst |

| European Equities | Neutral | Bearish | Sympathy selling | US weakness transmitted. No independent catalyst |

| Gold (XAU/USD) | Bullish | Neutral | $4,696 (-2.29%) | Profit-taking into dollar strength. Watch $4,650 support |

| Silver (XAG/USD) | Bullish | Bearish | -5.39% | Silver sold harder than gold. Industrial metal component hurting |

| Crude Oil (CL) | Bearish | Bullish | $91.75 (+2.39%) | Hormuz premium building. Approaching $92 resistance |

| Dollar (DXY) | Bearish | Neutral | +0.51% | Short-term reversal within structural weakness. Risk-off bid |

| Bonds (TLT) | Neutral | Bearish | -0.55% | Yields rising. No safe haven in bonds. Cash is king today |

Aggregate: 1 bullish (crude), 2 neutral, 5 bearish. Net reading: BEARISH short-term. Down from 4 bullish / 2 neutral / 2 bearish on Monday.

Critical observation: This is the first day since this analysis began where equities, bonds, and gold all sold simultaneously. When all three traditional asset classes decline together, the money is going to cash and the dollar. That is a macro de-risking signal, not a sector rotation.

Sector Performance – Tuesday 21 April

| Sector | Change | Read |

|---|---|---|

| Energy | +1.8% | Hormuz-driven crude rally lifting the sector |

| Utilities | +0.3% | Defensive rotation. Classic risk-off positioning |

| Technology | -0.45% | Mixed. MSFT/AMZN green, mega-cap names red |

| Consumer Discretionary | -0.82% | TSLA earnings fear dragging the sector |

| Financials | -0.91% | Yield rise should help but risk-off overwhelming |

| Industrials | -0.96% | Cyclicals unwinding. PMI tomorrow is the test |

| Materials | -1.15% | Monday’s leader is Tuesday’s laggard. Silver -5.39% driving this |

| Healthcare | -0.78% | Defensive but still selling. No safe harbour |

| Communication Services | -1.10% | GOOGL earnings tomorrow. Pre-event de-risking |

| Consumer Staples | -0.42% | Defensive but selling. Even safe havens are not safe today |

Sector narrative: Only 2 of 11 sectors green (energy and utilities). On Monday, 5 of 10 were green and the rotation was cyclical-into-value. Today the rotation is everything-into-cash. Energy is the exception because crude is trading on Hormuz headlines, not macro fundamentals. When the only green sector is geopolitically driven, that is not leadership. That is dislocation.

Economic Calendar – Wednesday Impact

| Event | Time | Significance | What to Watch |

|---|---|---|---|

| Flash Manufacturing PMI | 09:45 ET | HIGH | Above 50 = expansion intact. Below 50 = recession fears return. The number that tells you if the economy matches the market |

| Flash Services PMI | 09:45 ET | HIGH | Services is 70% of GDP. If this holds above 50 while manufacturing slips, the economy is bifurcated, not collapsing |

| Alphabet (GOOGL) Earnings | After close | CRITICAL | The AI thesis print. Cloud revenue and AI capex guidance are the numbers that move the entire tech sector |

| TSLA Earnings (tonight) | After close today | HIGH | Framework reads SHORT with T1 reached. Exhaustion signals. The options market priced an 8% implied move |

Wednesday is the most important day of the week. Flash PMI in the morning tells you about the economy. GOOGL in the evening tells you about the AI thesis. If both disappoint on the same day that VIX is above 20 and the structural framework is broken, the channel floor at 26,447 will be tested. If both beat, the hesitation ends and institutions re-engage.

The Dollar Problem

Monday’s macro story was “dollar weak, everything else strong.” Tuesday’s story is the opposite. DXY rose 0.51% and everything correlated to dollar weakness sold: gold down 2.29%, silver down 5.39%, emerging markets weak, commodities mixed.

This matters because the dollar trade was the highest-conviction macro call last week. DXY below 100 was supposed to be structural. One day of strength does not invalidate a multi-week thesis, but it does force you to question: is the dollar weakness over, or is this a counter-trend bounce within a larger decline?

The evidence says bounce. Dollar strength on a risk-off day is normal. The dollar is still the world’s reserve currency and the default destination when everything else sells. The test is whether DXY reclaims 99.5 on a sustained basis. A one-day move driven by de-risking is not the same as a fundamental reversal. But until the dollar rolls over again, the gold trade, the GBP/USD trade, and the emerging market trades all have a headwind they did not have yesterday.

Yields Rising – What It Means

TLT dropped 0.55% on Tuesday, meaning bond prices fell and yields rose. On a day when equities also sold, this is the worst combination for balanced portfolios. There is nowhere to hide except cash and the dollar.

Why yields rose matters more than that they rose:

- If yields rose on inflation expectations (crude at $91.75 feeding through to CPI forecasts), that is bearish for rate-cut expectations and extends the Fed pause. Equities and bonds both lose

- If yields rose on term premium (investors demanding more compensation for holding duration), that is a supply/demand issue and typically self-correcting

- If yields rose on growth expectations (economy stronger than expected), that would normally be equity-positive. But equities sold, so this explanation does not fit

The most likely explanation: crude at $91.75 is reigniting inflation concerns. If Hormuz tensions push crude above $95, the entire rate-cut narrative for 2026 collapses. That is the macro risk that the bond market is pricing today. Tomorrow’s Flash PMI will either confirm or deny this read.

Strategy by Timeframe

Scalping (1-5 min)

- VIX above 20 means wider stops and faster moves. Size down 25-30%

- Watch TSLA after-hours for gap direction on NAS100 Wednesday open

Intraday (15 min – 4 hr)

- Bias: NEUTRAL. Do not chase shorts in a 91% structural uptrend. Do not buy dips without confirmation

- Key levels: NAS100 26,447 (channel floor – the line in the sand) and 26,700 (resistance)

Swing (1-5 days)

- New NAS100 longs: WAIT until 26,447 is tested or Wednesday events resolve

- Gold: WAIT. Do not buy into a -2.29% day. If $4,650 holds on a retest, that is the entry

- GBP/USD: TIGHTEN stops. Dollar strength is a headwind. The structural thesis needs DXY to roll over

Positional (weeks-months)

- 91% structural bullish is the anchor. This is a pullback, not a reversal. But pullbacks within uptrends can be 3-5% and still be healthy

- The expansion thesis survives unless: PMI below 50, VIX sustains above 22, and the channel floor breaks. All three must happen. One or two is just noise

Risk Assessment

Domain risk: Around 60% (elevated)

Up from Monday’s 40%. The macro picture has deteriorated on every front simultaneously:

- Triple sell-off: Equities, bonds, and gold all down. This is the rarest and most concerning macro pattern

- Crude inflation risk: $91.75 crude threatens to reignite inflation expectations and kill rate-cut hopes

- PMI tomorrow: If manufacturing falls below 50, the market will reprice growth expectations overnight

- GOOGL earnings: The AI capex thesis is being tested. A miss on cloud revenue or guidance could pull the entire tech complex lower

- Structural framework broken: The trend lens that institutions rely on for timing has broken down on short timeframes

Scenario Analysis

| Scenario | Probability | Macro Trigger | Action |

|---|---|---|---|

| PMI beats + GOOGL beats | 25% | Growth and AI confirmed. Dollar fades. Bonds stabilise | Re-engage swing longs. VIX drops below 20. Risk-on resumes |

| Mixed (one beats, one misses) | 35% | Conflicting signals. Market stays in range | Hold. Wait for Friday BOJ clarity. No new positions |

| PMI below 50 but GOOGL beats | 20% | Economy weakening but AI thesis intact. Bifurcated market | Long GOOGL/MSFT, short IWM. Pairs trade. No index exposure |

| Both miss + crude above $95 | 20% | Growth scare + inflation scare + geopolitical escalation | De-risk everything. Cash and short-duration. Channel floor breaks. VIX above 23 |

Position Sizing

| Trade | Sizing | Macro Conviction |

|---|---|---|

| NAS100 long (dip) | REDUCED (4%) | Downgraded from MAX. Wait for 26,447 or earnings clarity |

| Gold long | WAIT | Do not catch a falling knife. Wait for dollar to roll over |

| Dollar short (GBP/USD) | REDUCED (4%) | Thesis intact structurally but headwind short-term |

| MSFT long | STANDARD (8%) | Macro rotation into quality. Confirmed by price and flow |

| Crude | AVOID | Headline-driven. Untradeable with positioning |

Experience Breakdown

Beginners

Stay flat. When equities, bonds, and gold all sell on the same day, it means the professionals do not know what happens next. If they do not know, you should not be trading. Wait for Wednesday’s data. The macro picture will be clearer in 24 hours.

Intermediate

If you hold Monday’s equity longs, tighten stops to 26,447 on NAS100 or $700 on SPY. Do not add. The macro dashboard went from 6/8 bullish to 3/8 in one session. That velocity of change demands caution, not courage.

Advanced

The macro de-risking creates opportunity if you can read the sequence. Watch TSLA tonight for the first signal. If TSLA misses and NQ gaps to 26,500, buy the gap IF VIX does not breach 23. If TSLA beats, watch whether the quality rotation (MSFT/AMZN) expands to the broader market or stays concentrated. The answer tells you whether this is a temporary de-risk or the start of a bifurcated market where only the strongest names survive.

Market Timing Verdict

- Short-term (1-7 days): BEARISH-NEUTRAL. Triple sell-off. VIX above 20. Structural lens broken. Do not force trades

- Medium-term (1-8 weeks): NEUTRAL. Downgraded from bullish. The 91% reading is intact but the short-term damage needs repair. Earnings and PMI are the repair mechanism

- Long-term (2-12 months): Cautiously bullish. Nothing in today’s data changes the expansion thesis. But the speed of the macro deterioration warrants respect

Cross-References

As you will find in our Positioning Pressure brief, the institutional dark pool drop of 31% confirms the macro de-risking we see across asset classes. And as our Sentiment Shift coverage details, the sentiment composite dropping to 38/100 with VIX above 20 creates the fear environment where earnings surprises have the most impact. Wednesday is the macro verdict day.

This is analysis, not financial advice. Always manage your risk.

Get the daily framework intelligence

Trade the framework, not the noise.

The principles in this article are how we read markets every day. Members get the live application: daily Pre-Asia, Pre-London, Pre-NY and Post-Close briefs across 20+ instruments, the indicator suite, the Foundry library, and live community.

Free Explorer tier · No card required · Upgrade when you’re ready

Deepen Your Understanding

Related articles from the Titan Protect Foundry: