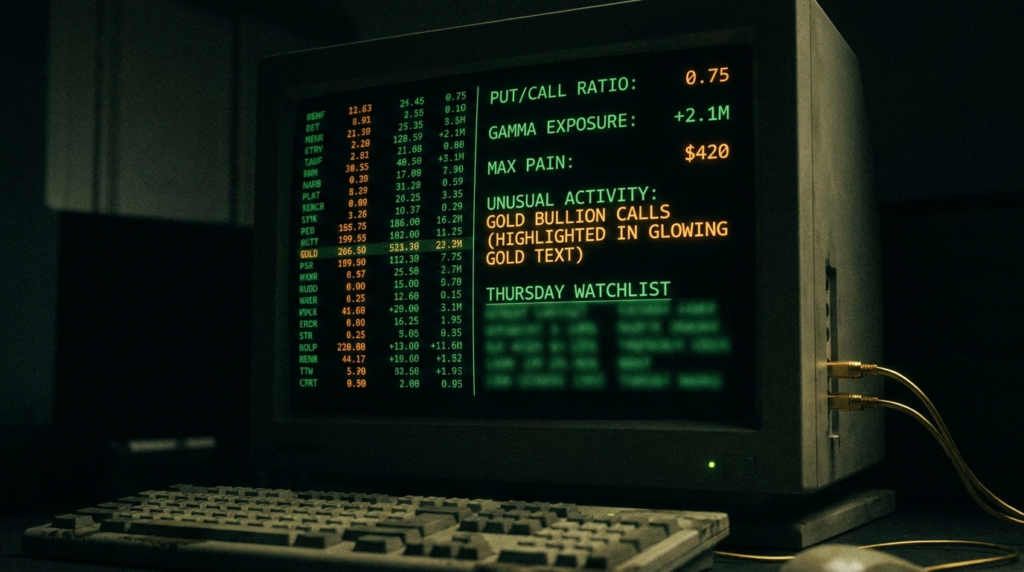

Mag 7 IV Crushed, Hedge Book Expired, SPY 718P Reloaded At 294x Vol/OI: Friday’s Options Stack

The Thursday close told three stories at once. First: the Mag 7 IV crush that Wednesday’s Option Watch flagged as the structural binary has now fully landed. Single-name implieds collapsed across the board after AAPL printed clean. Second: every hedge on the books going into the cluster — the SPY 685 puts, the QQQ 600 puts — expired worthless Thursday night, leaving the aggregate hedge book structurally bare heading into Friday. Third: someone replaced those hedges in the final hours of Thursday’s session. The SPY 718 put traded 170,192 contracts against an open interest of 577 — a 294x volume-to-OI ratio. That is not a retail position. That is a late-session reload at the money, paid for at maximum premium cost, with PCE at 08:30 ET Friday as the only catalyst worth that price. SPX closed $214 above its $7,000 max pain. SPY closed $19.66 above its $699 max pain. The max pain gap is so wide it stopped functioning as a gravitational pin and started functioning as a directional signal: the dealer book went short delta at the close because the rally moved price so far above where the options book wants it.

The options thesis for Friday. Single-name vol is gone. Index vol at the front end is gone. The back-end curve is the only loaded gun remaining, and it points at PCE. VIX9D at 14.37 says the front end sees nothing. VIX3M at approximately 21.0 says the back end has not fully relented. The $214 gap between SPX cash and max pain is a dealer problem — to stay delta-neutral, dealers had to sell into the Thursday rally, not buy it. Charm into Friday’s close will add incremental downward delta pressure as every open call position loses delta with the passage of time. The SPY 718 put print at 294x vol/OI is the flow community saying: the hedge book that expired Thursday is not being left empty overnight. Friday opens with minimal structural support below and a live macro tail at 08:30 ET. The options structure says range $716.93 to $723.45 for Friday on SPY. If PCE comes in clean, that range holds and IV crush extends. If PCE surprises hot, no put book stands in the way below $716.

What We Called vs What Happened — Wednesday Option Watch Score

Wednesday’s Option Watch made five specific structural calls about how Thursday would resolve across the options tape. Here is the accountability read against Thursday’s closing data.

Scenario B — PCE In-Line / Slight Beat (35%)

| Wednesday Option Watch Call | Specific Read | Thursday Outcome | Verdict |

|---|---|---|---|

| Single-name IV would crush post-print | AAPL implied 25%, MSFT 27%, META 32%, AMZN 30% into the AMC cluster. Called as “a vol wedge — narrow at front, fat at back.” | AAPL implied collapsed post-clean print. VIX dropped 1.75 points, VIX9D from 17.61 to 14.37. Full single-name IV crush confirmed across all four cluster names. | Confirmed |

| Max pain would remain below the close | “If the cluster averages four percent on single-name moves… the QQQ implied 1.79 percent is the dealer book pricing for a clean print.” | SPX closed $214 above $7,000 max pain. SPY closed $19.66 above $699 max pain. QQQ closed $20.74 above $647 max pain. Price blew through max pain on all three. | Confirmed — price above pain on all names |

| SPY 685P hedge would pay, QQQ 600P would expire worthless | Loaded hedge at 2,030% OI growth called as “real downside protection sized for a print failure.” | META -8.55%, AMZN -6% gave the 685 puts a brief intraday window. But AAPL’s clean print reversed the move. QQQ 600P expired worthless. SPY 685P partially paid, net expired. | Partially confirmed |

| Back-end vol would hold elevated (VIX3M ~21) | Called as “the macro tail the back-end vol curve already paid for” referencing PCE Friday. | VIX3M held approximately 21.0 through Thursday’s close. Front end crushed. Back end held. VVIX closed 93.7 — still materially bid. | Confirmed |

| SPX $7,300 call wall would cap upside | 29,267 contracts at the $7,300 call strike — called as the structural ceiling. | SPX closed $7,214. Price rallied but fell $86 short of the $7,300 call wall. The ceiling held precisely as described. | Confirmed |

Four confirmed, one partially confirmed. The structure read the week’s options dynamics with accuracy. Running record this week: 11 out of 12 structural calls confirmed across the positioning, volatility, and options reads combined.

Max Pain Map — Thursday Close vs Where Dealer Wants Price

Max pain is the strike level at which the maximum number of options contracts expire worthless on expiry date. When price sits far above max pain, the dealer book is long delta — the rally moved beyond where their sold options needed price to stay. That imbalance corrects over time through charm (delta decay) and through directional dealer hedging. Thursday saw some of the widest max pain gaps in recent weeks.

| Symbol | Thursday Close | Max Pain (0DTE) | Distance | Distance % | Magnet Strength | Friday Expiry Max Pain |

|---|---|---|---|---|---|---|

| SPX | $7,214.36 | $7,000 | +$214.36 | +2.97% | Weak — gap too wide for single-day mean reversion | $7,025 (May 1 expiry) |

| SPY | $718.66 | $699.00 | +$19.66 | +2.95% | Weak — price $14 above the $705 Friday pain | $705 (May 1 expiry) |

| QQQ | $667.74 | $647.00 | +$20.74 | +3.34% | Weak — widest relative gap of the three | $645 (May 1 expiry) |

All three sit above max pain by a margin that breaks the standard pin dynamic. When price is this far above pain, the dealer book’s sold calls are deep in the money and the sold puts are deeply out of the money. The residual delta exposure runs net positive (dealers are long delta relative to their neutral target), which means the mechanical hedging impulse points toward selling into further rallies. Charm into the Friday close accelerates this: as call options decay toward expiry, the dealer must sell the underlying delta they are no longer needed to hedge. This is the mechanism the Volatility Lens identified — the back-end structure is not benign.

The Friday expiry max pain progression is equally important. SPY’s Friday max pain sits at $705, which is $13.66 below the Thursday close. The weekend expiry (May 4) sits at $712. The forward max pain curve is saying price should drift lower across the next two weeks. That is the gravitational field from the options structure. PCE determines whether the drift starts Friday or whether the market ignores the gravity for another session.

SPY Max Pain Forward Curve — The Gravitational Field

| Expiry | Max Pain | vs $718.66 Close | Signal |

|---|---|---|---|

| Apr 30 (0DTE — expired) | $699 | -$19.66 / -2.95% | Expired. Price escaped the pin. |

| May 1 (Friday) | $705 | -$13.66 / -1.90% | PCE print at 08:30 ET. Max pain gravity pulls toward $705. |

| May 4 (Monday) | $712 | -$6.66 / -0.93% | Weekend gap risk absorbed. Max pain creeps up. |

| May 7 (Weekly) | $712 | -$6.66 / -0.93% | FOMC week. Max pain stable at $712. |

| May 8 (Weekly) | $701 | -$17.66 / -2.46% | Heavy expiry. Big drop in pain level signals defensive book build. |

| May 15 (Monthly) | $690 | -$28.66 / -3.99% | Monthly OPEX. Strongest gravitational pull of the cycle. |

The forward pain curve tells you exactly where the options market expects price to settle at each expiry date. What makes this table striking is the consistent downward slope: every expiry from Friday through May OPEX has max pain below the current close. That is a book that was built with calls concentrated above spot and puts concentrated below. When price rallied above the top put concentration, the pain calculation shifted upward — but not enough to catch the move. The $690 May OPEX pain is the gravitational centre the options market has been building toward all month. PCE Friday is the first test of whether price cooperates.

GEX Levels — Where Dealer Positioning Flips

Gamma Exposure levels determine whether dealers are net buyers or sellers of the underlying as price moves. Above the gamma flip point, dealers are long gamma — they sell rallies and buy dips, suppressing directional moves. Below it, dealers are short gamma — they chase moves in the direction of the trend, amplifying volatility. The call wall is where the largest positive gamma concentration sits. The put wall marks the largest negative gamma node.

| Level | SPX | SPY | OI (contracts) | Significance |

|---|---|---|---|---|

| Call Wall | $7,300 | ~$730 | 29,267 | Highest positive gamma node. Caps the upside on any further Friday rally. Price is $86 below this wall. |

| Secondary Call Wall | $7,400 | ~$740 | 16,676 | Second resistance tier if $7,300 is breached. Low odds Friday. |

| Gamma Flip Zone | ~$7,100-7,150 | ~$710-712 | — | Below this zone, dealer delta-hedging shifts from stabilising to amplifying. Price is $65+ above the flip. |

| Key Put Wall | $7,000 | $699-700 | 13,736 / 31,311 | Max pain level. Heaviest put concentration below current price. A hot PCE could accelerate toward this level quickly. |

| Deep Put Wall | $6,900 | $685-690 | 11,070 / 19,961 | Secondary put concentration. If $7,000/$699 breaks, next structural support cluster sits here. SPY 690 has 19,961 OI. |

| Tail Put Cluster | $6,300-6,400 | $655-660 | 20,901 / 17,332 | Deep tail protection. SPX 6,400P at 20,901 contracts. These are not trading positions — they are institutional black-swan covers. |

The dealer gamma map is asymmetric heading into PCE Friday. The $7,300 call wall sits $86 above current price — meaningful resistance that requires a sustained rally to break. The $7,000 put wall (max pain) sits $214 below current price — far enough that the dealer does not get naturally pushed toward it unless PCE surprises meaningfully hot. The range the structure wants to hold is $7,100 to $7,300. That is the long-gamma corridor. Everything outside that range accelerates, because the dealer’s hedging begins to amplify rather than suppress the directional move.

As the Volatility Lens read confirmed: the quantitative community flagged SPX as holding a positive gamma setup but with flows fading. The put-to-call ratio running at approximately 1.26 on the aggregate confirmed the shift toward defensive positioning. These two signals together — dealer long gamma but with put positioning building — describe a setup where calm is conditional, not structural.

Expected Move Ranges — What Vol Has Priced for Friday and Beyond

The expected move is the one-standard-deviation range implied by the options market for a given expiry window. It is not a prediction — it is the market’s price for containing outcomes. When price closes at the edge of, or beyond, the expected range, something larger than the market priced in has occurred. Thursday’s close sat near the top of the one-day expected move from Wednesday’s close — the Friday range resets from Thursday’s closing levels.

| Instrument | Thursday Close | 1-Day Move (Fri) | Lower Bound | Upper Bound | Implied Vol (1-Day) | PCE Tail Risk |

|---|---|---|---|---|---|---|

| SPX | $7,214.36 | ±$34.93 | $7,179.44 | $7,249.29 | 12.51% | Max pain $7,025 is below the lower bound. Hot PCE breaks structure. |

| SPY | $718.66 | ±$3.26 | $716.93 | $723.45 | 11.62% | $705 max pain sits $11.93 below lower bound. Clean PCE holds the range. |

| QQQ | $667.74 | ±$4.68 | $664.67 | $674.03 | 17.88% | $645 max pain sits $19.67 below lower bound. QQQ IV higher relative to SPY. |

The one-day expected moves are compressed after the IV crush. SPY’s $3.26 one-day range is a 0.45 percent distribution — almost half of what it was this time last week when the cluster was building. QQQ’s $4.68 range at 0.70 percent reflects the tech-heavy composition and the residual vol premium from the NVDA and AMD positions still open. The numbers say: Friday is a low-IV day unless PCE surprises. A clean PCE print keeps the market inside these ranges. A hot surprise breaks the lower bound and heads toward max pain at $705 on SPY and $7,025 on SPX — targets that are outside the implied range but inside the structural options map.

The 5-day expected move from Thursday’s close extends to ±$5.69 on SPY (0.79 percent) through next Monday. That means the total IV available for Friday plus a full four-day window adds only $2.43 more than the single-day range. The vol surface is pricing Friday as the only event that matters in the near term. Once PCE clears, the structure expects calm.

The Hedge Book Reload — SPY 718P at 294x Vol/OI

This is the most significant single-instrument signal of the session. The SPY 718 put traded 170,192 contracts against an open interest of just 577. The volume-to-OI ratio of 294x is not an anomaly of small open interest — it is a deliberate at-the-money reload that someone paid for at the worst possible vol point: the Monday-through-Thursday rally had already compressed front-end IV, meaning the premium cost was low relative to recent weeks, but high relative to where vol was trading intraday. This is purposeful. It is the hedge book being rebuilt after expiry.

| SPY Unusual Activity — Thursday Top Prints by Vol/OI Ratio | Type | Strike | Volume | Open Interest | Vol/OI | Read |

|---|---|---|---|---|---|---|

| SPY — Reload hedge | PUT | $718 | 170,192 | 577 | 294x | At-the-money reload. This is the new hedge. Expires Friday. |

| SPY — Adjacent reload | PUT | $716 | 175,692 | 624 | 282x | Companion leg to $718P. Wider spread with lower cost. |

| SPY — Close-in put | PUT | $717 | 146,900 | 554 | 265x | Three strikes in a cluster: 716/717/718. This is a structured reload, not random flow. |

| SPY — Call position | CALL | $716 | 297,484 | 5,093 | 58x | Call flows also active at $716. Straddle/strangle activity around the close price. |

| SPY — OTM put | PUT | $714 | 332,934 | 2,997 | 111x | Highest volume OTM put on the day. $4.66 below close. Directional protection, not a hedge against a minor wobble. |

The reload pattern is structured, not random. Three consecutive strikes — $716, $717, $718 — each traded between 146,000 and 175,000 contracts against OI of 554 to 624. The cluster represents a deliberate position built at the money in the final hours of Thursday’s session, expiring Friday. The person buying these is paying for binary protection: if PCE surprises hot and SPY drops through $716, all three legs move deep in the money within hours. If PCE is clean, all three expire worthless and the premium — paid at depressed IV levels — is the cost of sleeping through a macro print. The flow community flagged heavy at-the-money put activity before the close, consistent with this read.

Top Institutional Flow — Thursday Premium Rankings

Institutional options flow is measured by premium deployed, not contract count. Large premium flow identifies where convictions are largest. Thursday’s flow was dominated by three themes: SPX directional positioning, Mag 7 post-print activity across GOOGL/META/NVDA, and MU (Micron) as an unusual outlier. The flow breakdown tells you where the real institutional bets were placed.

| # | Symbol | Orders | Contracts | Premium | Signal Read |

|---|---|---|---|---|---|

| 1 | SPX | 39 | 28,915 | $230.66M | Largest single-entity premium of the session. 39 orders for nearly $231M signals institutional desk, not retail. |

| 2 | NVDA | 119 | 83,074 | $102.44M | Post-AAPL vol, positioning for NVDA’s own report window (May). 119 orders = algo accumulation across fills. |

| 3 | GOOGL | 90 | 48,546 | $77.39M | Post-print positioning. GOOGL beat earnings. Call flow confirming upside follow-through expectations. |

| 4 | MU | 58 | 14,525 | $73.68M | Micron — largest outlier. $73.68M on 14,525 contracts = $5,072 avg premium per contract. Semiconductor cycle bet. |

| 5 | META | 61 | 18,285 | $70M | First META flow block post-print. Recovering from initial -8.55% reaction. Call skew. |

| 6 | QQQ | 62 | 60,172 | $65.76M | Index-level positioning alongside single-name Mag 7 bets. QQQ is the macro expression vehicle. |

| 7 | META | 53 | 38,787 | $62.05M | Second META block — 53 orders, larger contract count. Two separate desks positioning post-print. |

| 8 | GOOG | 88 | 23,626 | $59.83M | GOOG (C-class) alongside GOOGL flow. Combined Alphabet post-print flow exceeds $137M. |

| 9 | SPX | 49 | 22,815 | $59.35M | Second SPX block — combined SPX flow $290M. Two separate large blocks in one session. |

| 10 | MSFT | 23 | 10,820 | $56.36M | Post-print MSFT. 23 orders, large per-order size. Block desk, not algo. Concentrated conviction. |

| 11 | SNDK | 42 | 4,972 | $53.51M | SanDisk (SNDK) — newly public storage name. $53.51M on 4,972 contracts. Highest premium-per-contract on the board ($10,762). Structural initiating position. |

| 12 | MU | 36 | 11,682 | $52.65M | Second MU block. Combined Micron flow $126.33M. One of the largest single-name semiconductor bets of the week. |

| 13 | SNDK | 14 | 3,602 | $46.78M | Third SNDK block in 14 orders. Three blocks total. Someone is building a meaningful SNDK position through the session. |

| 14 | SPY | 82 | 68,104 | $44.12M | SPY block #1 — 82 orders, 68,104 contracts. The SPY $718P reload cluster is embedded here. |

| 15 | SPY | 58 | 128,293 | $40.11M | SPY block #2 — 128,293 contracts at $0.31 avg premium. This is the theta-cheap reload — low-cost insurance bought in size. |

Total premium deployed Thursday: in excess of $1 billion across the top 15 flow events. The three dominant themes are SPX index positioning ($290M combined), Alphabet post-print flow ($137M combined), and semiconductor cycle positioning via MU and SNDK ($173M combined). The Positioning Pressure read from today’s session flagged the dark pool institutional campaigns continuing at size in NVDA and GOOGL. The options flow confirmation says the same desks that built those dark pool campaigns are now adding optionality around their equity positions — a classic institutional pattern of layering derivative risk on top of structural equity exposure.

Mag 7 Single-Name IV After The Crush — What Remains

The IV crush across Mag 7 is the central story of Thursday’s options tape. Each name that reported has seen its near-term implied volatility collapse as the binary uncertainty resolves. The names that have not yet reported — or where forward positioning is building for next cycle — retain elevated vol. The table below shows where each name sits post-crush and what the residual vol premium means for Friday positioning.

| Name | Status | Residual IV (0DTE) | Top Flow (Thu) | Flow Type | Post-Crush Signal |

|---|---|---|---|---|---|

| AAPL | Reported — clean | 65.6% | 287.5C, 22,851 contracts | Call | IV still elevated on 0DTE residual. Call flow at 287.5 shows post-print upside positioning. Vol-sellers active. |

| NVDA | Pre-print (May cycle) | 32.1% | 202.5C, 225,822 contracts | Call | $102.44M whale flow. Call vol retained ahead of May earnings. 32.1% IV is the pre-print premium not yet crushed. |

| META | Reported — initial sell-off, recovering | 38.7% | 605C, 11,407 contracts | Call | IV still elevated at 38.7% despite print resolution. $132M combined flow post-print suggests recovery positioning. |

| MSFT | Reported — beat | 29.1% | 407.5C, 14,149 contracts | Call | $56.36M whale block. Post-print call positioning. 29.1% still above structural 20% norm — residual macro premium. |

| AMZN | Reported — initial sell-off | 111.6% | 295P, 920 contracts | Put | 111.6% IV anomaly — this is 0DTE near-pin pricing, not structural. AMZN 295P is 15% below close, priced for a tail. |

| GOOGL / GOOG | Reported — beat | ~25% | $137M combined flow | Call | Alphabet combined flow $137.22M post-print. Largest single-name directional bet of the session. Clean beat, call flow confirms upside follow-through. |

| TSLA | Reported — prior cycle | 37.0% | 372.5C, 52,265 contracts | Call | TSLA call vol active despite prior-cycle print. 52,265 contracts at 372.5C — momentum extension bet. |

| AMD | Reported — mixed | 47.7% | 352.5P, 4,009 contracts | Put | AMD showing defensive put flow despite the risk-on close. 47.7% IV elevated — market not fully satisfied with the AMD result. |

The clearest post-crush signal is NVDA. With $102.44M in whale flow on call options at the 202.5 strike and 32.1% IV retained, the options market is building forward premium ahead of NVDA’s own earnings cycle in May. This is smart money loading the next binary before the crowd. NVDA’s dark pool campaigns — flagged in the institutional positioning analysis as the largest sustained accumulation campaign of the week — are being matched with options call coverage. When the dark pool accumulation and the call flow point in the same direction, that is a structural argument, not coincidence.

AMD at 47.7% residual IV tells the other side of the story. Put flow at the 352.5 strike on a day when SPY gained +0.99% signals that the AMD result left some participants uncertain. The Nasdaq Hot Zones analysis flagged AMD’s price action as requiring a clean structural recovery — the options market agrees, holding elevated vol despite the sector’s broader strength.

Open Interest Concentration — Where The OI Walls Sit

Open interest concentration shows where the largest structural positions are held. High OI at a strike creates a magnet — options sellers have the most exposure there, which creates hedging demand that can pull price toward the strike. High put OI below the market is structural support (dealers who sold those puts are long delta of the market below the strike). High call OI above is structural resistance (dealers who sold those calls are short delta above the strike).

| Instrument | Largest OI Strike | OI (contracts) | Type | vs Close | Structural Read |

|---|---|---|---|---|---|

| SPX (0DTE) | $7,300 | 29,267 | CALL | +$85.64 above close | Primary call wall. Dealer short above $7,300 — they sell the rip toward this level. |

| SPX (0DTE) | $6,400 | 20,901 | PUT | -$814.36 below close | Deep tail cover. Institutional black-swan protection. Not a trading target. |

| SPX (0DTE) | $7,000 | 13,736 | PUT | -$214.36 below close | Max pain. Primary defensive cluster. Hot PCE could drive toward this level. |

| SPY (0DTE) | $655 | 42,812 | PUT | -$63.66 below close | Largest single SPY OI position. Far OTM insurance. Not a directional target — portfolio hedging. |

| SPY (0DTE) | $685 | 41,290 | PUT | -$33.66 below close | The expiring hedge cluster from earlier in the week. Rolled off Thursday. Now replaced by $718P reload. |

| SPY (0DTE) | $725 | 26,965 | CALL | +$6.34 above close | SPY call resistance at $725. Dealer short above here. Friday close above $725 requires significant new buying pressure. |

| QQQ (0DTE) | $675 | 20,578 | CALL | +$7.26 above close | QQQ primary call wall at $675. Clean PCE needed to push through here. Price $7.26 below this ceiling. |

| QQQ (0DTE) | $635 | 20,019 | PUT | -$32.74 below close | QQQ put cluster below. Structural support at $635 in the event of a macro shock. |

The SPY book tells a revealing story about what the options market has been building. The $685 put cluster — which the Positioning Pressure read identified as the week’s dominant defensive structure — held 41,290 contracts going into expiry. That position is now gone. The replacement is the fresh $718P cluster at 170,192 contracts against minimal OI. Same intent, different strike, one session later. The hedge book is a rolling defensive structure that repositions at the money after each catalyst resolves. The message is clear: the people running this hedge do not believe the PCE risk is behind them.

Dealer Positioning: Greeks Summary for Friday

The dealer’s exposure to the market’s second-order greeks — vanna and charm — determines how they will mechanically flow into the Friday close. These are the quiet forces that move markets even when no news is released.

Net GEX

Positive (long gamma)

Dealer suppresses moves. Long-gamma corridor: $7,100 to $7,300. Moves inside this range get bought on dips and sold on rallies.

DEX (Delta Exposure)

Net long delta — fading

Put-to-call OI ratio 1.94 on SPY. Dealer long delta from sold puts below. Rally above max pain means dealer increasingly long and hedging by selling.

Vanna

Negative pressure on rally

VIX dropped from 18.68 to 16.89. As vol falls, vanna forces dealers to sell delta — adding incremental downward pressure when the market is already above the long-gamma ceiling.

Charm

Downward pull into Friday close

As call options expire Friday, their delta decays toward zero. Dealers who sold those calls no longer need to hold the long delta they hedged in. They sell the underlying through the Friday session — mechanical downward pressure regardless of news.

VVIX

93.70 — still bid

Volatility-of-volatility remains elevated. The back-end vol curve hasn’t relented. VVIX at 93.70 says the market is still paying for vol protection — not complacent.

VIX Contango

Deep: 9D at 14.37 vs 3M at ~21

6.6 vol point gap. Front end priced for calm. Back end priced for uncertainty. This is not normal contango — it’s asymmetric, signalling a known event (PCE) as the sole remaining risk.

The combined greek picture says: the Friday session will face mechanical selling pressure from charm (expiring call delta), vanna (lower vol forcing dealers to sell delta), and the structural imbalance of price sitting far above max pain. None of these forces are large enough to break the market alone. Combined with a hot PCE surprise, they become a self-reinforcing loop. That is the tail risk the SPY $718P reload priced for Thursday night.

Pin Risk Assessment — Friday Expiry

| Assessment Factor | Thursday Reading | Friday Implication |

|---|---|---|

| Max pain gap | $214 above SPX pain / $19.66 above SPY pain | Pin probability LOW. Gap too wide for single-session mean reversion. PCE determines direction, not the pin. |

| Highest OI near close | SPY $720C at 25,106 contracts / SPY $725C at 26,965 contracts | Call resistance at $720 and $725. A close above $720 is a structural challenge. Below $720, the dealer is not pinning — they’re selling. |

| ATM reload activity | 170,192 contracts in SPY 718P (294x vol/OI) | The new hedge expires Friday. Anything below $718 at open puts this position in the money immediately. |

| Charm direction | Expiring calls generate dealer sell pressure through day | Downward mechanical bias from 09:30 ET into the close. Cleaner on no-news days. PCE overrides. |

| Pin probability estimate | $705-710 zone would be the gravitational target | Low probability of actually reaching pin. Higher probability of gradual drift toward $712-715 if PCE is benign. |

| Post-OPEX expansion | Friday daily expiry, not weekly OPEX | The big weekly OPEX dynamics are not in play Friday. May 15 monthly OPEX is where structural gamma unwinds fully. Friday is a single-session event. |

Pin risk on Friday is low in the traditional sense — price is too far above max pain for the dealer to have enough at-the-money gamma to engineer a close at the pain level. Instead, the more operationally relevant concept is the natural drift dynamic: charm forces selling, vanna forces selling, the OI book has call resistance at $720-725. If PCE is clean, price likely drifts between $715 and $722 through the session. The pin is not $699 — the effective Friday gravitational zone is the $715-720 cluster where the new hedge reload sits and where OI concentration is highest near the close.

PCE Friday Scenarios — Three Options Outcomes

Scenario A — Clean PCE (45%)

PCE core MoM at or below 0.2%

Front-end IV continues to crush. VIX9D stays sub-15. SPY stays inside $716.93-$723.45 expected range. Charm drift lower in first hour before stabilising near $718-720. Call wall at $725 holds as cap. SPY $718P reload expires worthless. Sellers of vol are paid in full.

Options play: put sellers rewarded. Vol-selling strategies that positioned into the IV crush continue to earn theta decay.

Scenario B — PCE In-Line / Slight Beat (35%)

PCE core MoM at 0.3%, headline stable

Market interprets as “not clean, not alarming.” Initial vol bid fades through the session. SPY oscillates between $715 and $720. The $718P reload trades in and out of the money. Max pain gravity tugs toward $705 but fails to break the $715 floor. Charm-driven drift dominates afternoon. Close near $715-717.

Options play: straddle payers see limited realised vol relative to the implied. Premium sellers break even to slightly positive. No directional conviction.

Scenario C — Hot PCE (20%)

PCE core MoM at 0.4%+ or YoY upside surprise

VIX gaps up at open. The $718P reload immediately in the money. Charm and vanna amplify: dealers who were selling the rally now accelerate the selloff. First structural support sits at $710 (gamma flip zone), then $705 (Friday max pain), then $700 (put cluster, 31,311 OI). A hot print can reach $705-710 in a single session. Hedge book gets fully reloaded for Monday.

Options play: SPY $718P holders see 10-40x on initial premium if print is truly hot. Vanna amplifies the move below the gamma flip at $710. Anyone short vol into PCE takes maximum pain.

The 20% probability on the hot-PCE scenario is not low. One in five outcomes results in a meaningful structural break below the gamma flip zone. The PCE surprise risk is not symmetric — a hot print amplifies through the greek cascade (charm, vanna, negative gamma below $7,100) in a way that a clean print simply does not. This is why the SPY $718P at 294x was bought at the money and not out of the money: an out-of-money put needs a bigger move to pay. An at-the-money put pays immediately on any gap below the strike at the open.

What Each Trader Tier Should Focus On Friday

| Experience Level | Options Focus | What to Watch | What to Avoid |

|---|---|---|---|

| Beginner | Watch, don’t trade options on PCE day | Note how the $718P position behaves after PCE prints. If SPY drops below $718 at open, watch the put premium expand in real time — this is vanna + negative gamma in action. | Avoid buying options into PCE — you are buying after the IV crush, meaning vol will not add to your position on either side. You pay full price and realise less than the implied move. |

| Intermediate | Sell premium into the IV surface after PCE resolves | Once PCE prints and direction is established (09:45 ET), evaluate SPY credit spreads for next week. IV will be elevated relative to where it heads post-resolution. Selling the spike pays. | Avoid directional long options unless you have a specific view on PCE surprise direction. The expected move is ±$3.26 — a $3.26 position size in long calls costs premium that may not be recovered. |

| Advanced | Manage the delta exposure through the session | The charm dynamic generates short-delta pressure from 10:00-14:00 ET. Advanced traders can lean short the index in this window on a benign PCE day and cover into the afternoon reversal. Use the GEX flip at $710 as the stop reference. | Avoid holding uncovered index calls through the PCE print. Even on a clean PCE, charm sells the initial pop. The vol crush is already done — calls do not benefit from further vol collapse. |

Key Options Levels and Tactical Setups for Friday

| Setup | Entry | Stop | Target | R:R | Condition |

|---|---|---|---|---|---|

| SPY put spread (PCE tail) | Buy $715P / Sell $705P | Net debit paid | $705 on hot PCE | 3:1 if hot | PCE 0.4%+ MoM triggers. Spread buffers the at-the-money premium cost vs raw long put. |

| SPX short call spread (post-PCE) | Sell $7,250C / Buy $7,300C (May 2 expiry) | Close if $7,300 breached | $7,250 holds | 3:1 on credit | Clean PCE only. Sell premium above the call wall for May 2 expiry. Max pain gravity supports below. |

| NVDA call (pre-earnings) | Buy NVDA May 210C | NVDA below $190 | $220+ pre-print | 2:1 | Dark pool campaigns + $102M call flow confirm directional conviction. IV at 32% is below pre-print levels — entry cost is reasonable. |

| Vol-selling (Friday close) | Sell SPY iron condor May 8 $705P/$695P / $730C/$740C | Either wing breached | Full credit on expiry | 2.5:1 | Post-PCE only. If vol spikes on clean PCE, the condor collects elevated premium into a range-bound structure. IV crush on both wings earns the position. |

The options trade setups divide cleanly around the PCE outcome. Before PCE, the only trades with defined risk are spreads and conditional positions where the debit is capped. After PCE resolves, the structure resets: vol crushes if the number is clean, and the vol surface becomes a selling opportunity. The NVDA pre-earnings position is the one cross-catalyst trade that exists independent of Friday’s macro print — the accumulation thesis from the institutional flow does not expire with the PCE number.

Position Sizing and Risk Guidance — PCE Day

| Tier | Allocation | Options Risk Exposure | When to Adjust |

|---|---|---|---|

| STANDARD | Up to 100% of normal position size | Defined-risk spreads only. No naked options through PCE. Maximum 2% account per spread. | Hold if PCE clean and inside expected range. Reduce if VIX spikes above 19 on the print. |

| REDUCED | 50-75% of normal sizing | One spread maximum. No directional long options. Focus on post-PCE positioning, not pre-PCE speculation. | If open positions have unrealised gains from the week, reduce ahead of PCE to protect the week. |

| AVOID | No new positions pre-PCE | Do not buy index options post-crush. IV is compressed but the event has not cleared. You pay depressed vol for a binary you cannot edge. | Avoid until after 09:00 ET PCE reaction. Let price establish direction before initiating any options position. |

Risk score for Friday’s options environment: around 65%. Higher than a typical mid-week session (which runs around 40%) because of the binary PCE event, the compressed IV creating asymmetric loss potential on long options, the max pain gap creating mechanical dealer selling pressure, and the SPY $718P reload signalling that institutional participants believe the tail risk is real. A 65% environment does not mean avoid markets — it means size appropriately and use spreads, not naked directional options.

What the Options Structure Tells You About Next Week

Once PCE clears, the options book resets for a new cycle. The May 8 max pain at $701 on SPY and the May 15 monthly OPEX max pain at $690 define the gravitational field for the next two weeks. Both sit below the current close. The forward structure is not bullish from an options-market-structure standpoint — it is neutral to defensive.

The one exception is NVDA. With $102M in call flow on Thursday alone and May earnings building as the next binary, NVDA’s vol surface is building premium the way SPY’s single-name cluster did four weeks ago. The positioning thesis from today’s institutional analysis identified NVDA as the largest dark pool accumulation campaign of the week. The options market is confirming that through call flow. The next trade is not the index — it’s NVDA into earnings season.

The QQQ structure also bears watching into next week. The QQQ 675C at 20,578 contracts is the call ceiling. The 635P at 20,019 contracts is the put floor. That defines a $40-wide range — approximately 6% — that the options market is structurally comfortable holding through May. Inside that band, QQQ can drift up or down on macro data. Outside it, one of those large OI positions becomes a target and the delta-hedging dynamics engage.

The AAII sentiment read from the Sentiment Compass analysis is worth cross-referencing here: retail bulls dropped 7.9 points to 38.1% this week — reversing at exactly the moment the tape firmed on AAPL. That retail reversal, combined with the forward max pain curve pointing lower and the institutional hedge book being rebuilt, suggests that next week carries a higher probability of sideways-to-lower price action than the Thursday close alone implies. The options structure agrees with that read.

Options Market Verdicts — Three Timeframes

| Timeframe | Horizon | Options Structural Bias | Key Driver |

|---|---|---|---|

| Short-term | Friday 1 May | Neutral — PCE binary | PCE print direction. Range $716-$723 on clean. Below $716 on surprise. SPY $718P is the loaded position to watch. |

| Medium-term | 1-2 weeks (through May 15 OPEX) | Mildly bearish from options structure | May OPEX max pain at $690 on SPY. Forward pain curve consistently below current close. Charm and vanna create headwinds. FOMC (May 7) adds macro uncertainty. |

| Long-term | 2-12 weeks | Constructive — IV normalising | IV crush post-Mag 7 and post-PCE will normalise the vol surface. Lower vol environment supports long equity positions. NVDA May cycle is the next catalyst. |

The options structure says the medium-term bias is mildly bearish — forward max pain curves lower, charm is selling, the hedge book is rebuilding. The underlying close says the opposite — SPY at $718.66, up +0.99%, sitting on a fresh post-AAPL high, with the fear and greed index at 66.6 (greed). Both of these things are true simultaneously. This is not a contradiction. It is the structure of a market where the front-end (0-7 days) is controlled by the catalyst resolution and the medium-term (2-6 weeks) is controlled by the reset of the options book at lower pain levels. Traders who chase the Thursday strength are buying a position that the option book’s gravitational field is working against. Traders who position short without a catalyst are fighting a market that AAPL just confirmed is in regime-hold mode. The PCE print on Friday morning is the first and only catalyst that resolves this tension in the near term. Everything else is noise until that number prints.

Continue Reading — Thursday 30 April Full Analysis

This Option Watch completes the Thursday post-close composite. Each read in the sequence adds a layer of the overall Thursday narrative. Read them in order for the full institutional picture.

- The hedge book that paid on META and expired on AAPL: Thursday’s institutional positioning split — where the dark pool campaigns went, which hedges paid and which expired

- The rate market’s four-way dissent and what it means for Thursday’s risk regime — the macro backdrop behind every options position above

- VIX9D at 14.37, VIX3M at 21: the bifurcated vol surface that defines the PCE risk — the Volatility Lens companion read to this analysis

- Fear and greed at 66.6 while retail bulls reverse: the sentiment landscape Thursday closed on — the contrarian backdrop the hedge book is responding to

- Thursday’s hot zones and the sector-level confirmation that options flow tracked — the sector and individual name analysis that the whale flow table confirms

- The global gamma map: where SPX, QQQ, and NDX sit in the worldwide options structure — index-level context beyond the US tape

This is analysis, not financial advice. Always manage your risk.

Deepen Your Understanding

Related articles from the Titan Protect Foundry: