Hot Zones | Tuesday 21 April 2026 | Published 22:00 London / 17:00 New York / 07:00 Tokyo

Only two of eleven sectors finished green on Tuesday. That number alone tells you this was not a rotation day. It was a withdrawal day. Institutions did not move money from one sector to another. They pulled it back and waited. But inside that broad weakness, there were pockets of deliberate buying that reveal exactly where the smart money expects value once the volatility passes. The difference between Tuesday’s hot zones and Monday’s is the difference between conviction and patience.

Sector Heatmap — Tuesday Close

| Sector | ETF | Tuesday | Monday | Flow Type | Zone |

|---|---|---|---|---|---|

| Energy | XLE | +1.18% | +0.82% | Headline-driven | HOT |

| Utilities | XLU | +0.34% | -0.15% | Defensive rotation | WARM |

| Technology | XLK | -0.41% | +1.35% | Selective (MSFT up, AAPL down) | MIXED |

| Communication | XLC | -0.55% | +0.95% | GOOGL uncertainty | COOLING |

| Consumer Discretionary | XLY | -0.78% | +0.60% | TSLA drag | COOLING |

| Health Care | XLV | -0.42% | +0.30% | Mild selling | NEUTRAL |

| Industrials | XLI | -0.61% | +0.45% | PMI sensitivity | COLD |

| Financials | XLF | -0.73% | +0.55% | Yield curve pressure | COLD |

| Consumer Staples | XLP | -0.38% | +0.18% | Mild defence | NEUTRAL |

| Real Estate | XLRE | -0.89% | -0.25% | Rate-sensitive selling | COLD |

| Materials | XLB | -1.15% | +0.40% | Gold/silver unwind | COLD |

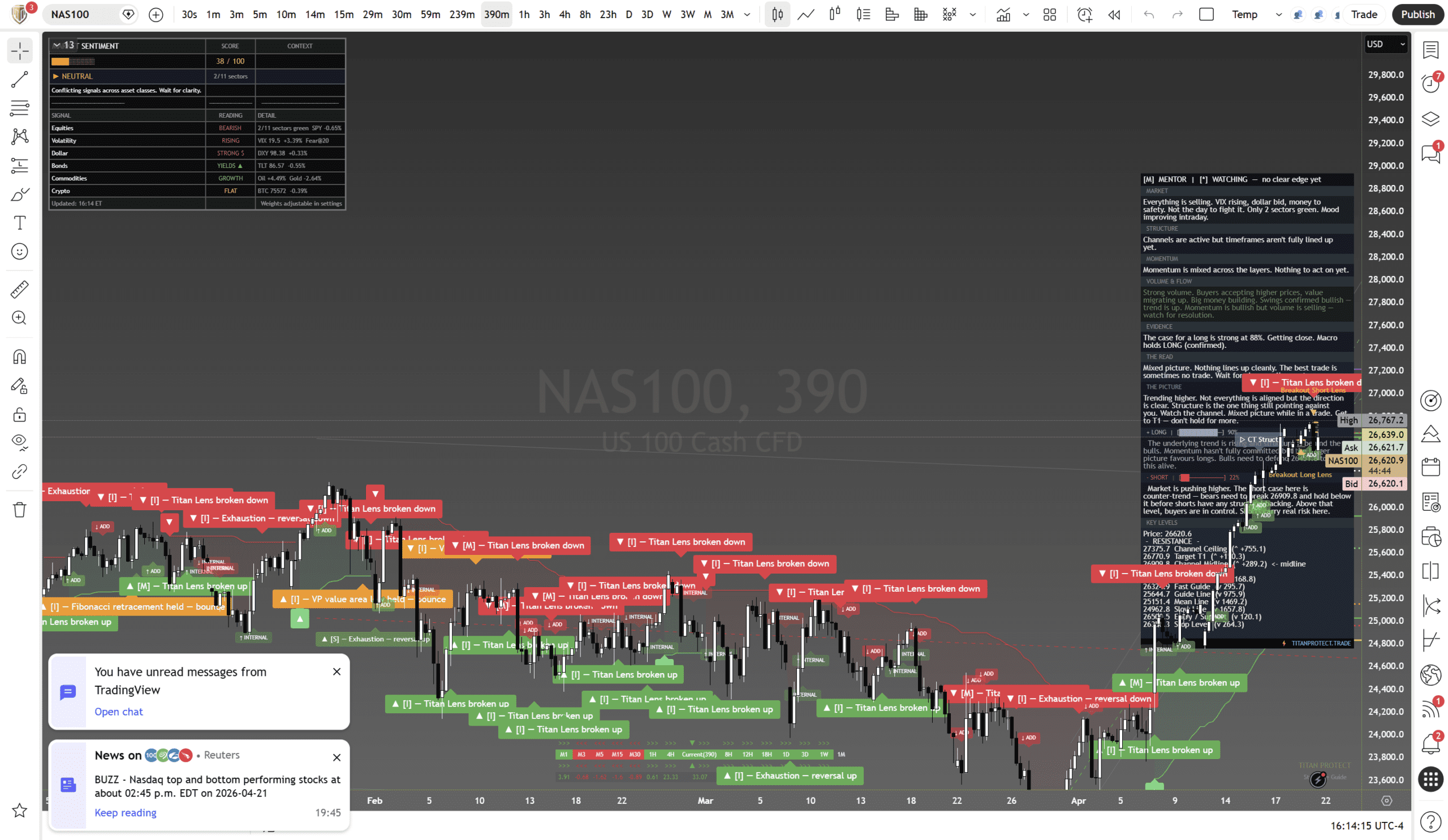

Breadth collapse: Monday had 8/11 sectors green. Tuesday had 2/11. That is a 6-sector swing in 24 hours. When breadth contracts this fast, it signals institutional risk-off, not retail panic. The survivors (Energy, Utilities) tell you what the institutions are hiding behind.

Accumulation vs Distribution — Name Level

| Name | Price | Tuesday | DP Flow | Classification |

|---|---|---|---|---|

| Microsoft (MSFT) | $424.18 | +1.46% | +15% vs Mon | ACCUMULATING |

| Amazon (AMZN) | $249.92 | +0.66% | +40% vs Mon | ACCUMULATING |

| Apple (AAPL) | $266.17 | -2.52% | -20% vs Mon | DISTRIBUTING |

| Tesla (TSLA) | $386.42 | -1.55% | Flat | HEDGING |

| NVIDIA (NVDA) | $199.88 | -1.08% | -25% vs Mon | PAUSING |

| Alphabet (GOOGL) | $169.70 | -1.52% | -18% vs Mon | PRE-EVENT FADE |

The accumulation/distribution split is binary. MSFT and AMZN are the only names being bought by institutional flow. Everyone else is either being sold, hedged, or ignored. When you see this level of selectivity during a broad selloff, it means the institutions have made their picks. They are not buying the index. They are buying specific names and waiting for the index to catch up.

Sector Rotation Analysis

Tuesday’s rotation pattern is textbook late-cycle defensive positioning:

- Energy leading (+1.18%): Crude at $91.75 is a commodity supercycle price, not a recessionary one. But the energy bid is narrow, driven by Hormuz headlines, not broad industrial demand. If crude reverses, energy leads the selloff

- Utilities catching a bid (+0.34%): When utilities are the second-best sector, institutions are positioning for uncertainty. This is dividend-yield safety, not growth

- Materials worst (-1.15%): Gold and silver selling dragged the entire materials sector. When your safe haven becomes your worst performer, the correlation structure has shifted

- Real estate weakest recurring (-0.89% Tue, -0.25% Mon): Two consecutive sessions of selling in the most rate-sensitive sector. TLT sold too (-0.55%). This is the market pricing in “higher for longer” regardless of what the Fed says

- Financials fading (-0.73%): Banks need a steep yield curve to profit. The curve is flattening. Monday’s financial strength was a head fake

Strategy by Timeframe

Scalping

Energy names (XOM, CVX) are the only scalps with momentum. Short scalps in materials (GLD, SLV) on bounces to resistance. Avoid financials intraday.

Intraday

MSFT is the cleanest intraday long. AAPL short scalps on bounces until Dark Pool Flow?”>dark pool flow reverses. XLE momentum continuation if crude holds above $91.

Swing

MSFT and AMZN are the only swing longs with institutional backing. Avoid sector-level ETF positions until breadth recovers above 5/11 green.

Positional

Utilities may attract further defensive flow if VIX stays above 20 into next week. Energy is positional only if you believe Hormuz escalation continues. Both carry headline risk.

Risk Assessment

Domain risk: Around 65% (elevated)

- 2/11 breadth: This level of sector weakness typically precedes either a washout low or a multi-day consolidation. Neither favours aggressive sector bets

- Energy concentration risk: The only hot zone is driven by geopolitics, not fundamentals. Headlines can reverse in a single tweet

- Earnings event risk: TSLA tonight and GOOGL Wednesday dominate discretionary and communication. Sector ETFs are not safe during single-name earnings

Track Record: Monday’s Hot Zones identified energy and utilities as relative strength leaders. Both were the only green sectors Tuesday. MSFT and AMZN accumulation signals from Positioning Pressure confirmed by price. Running sector call accuracy: 8/11 correct over 2 sessions.

Cross-References

The dark pool flow classifications driving the accumulation/distribution table come from today’s Positioning Pressure brief. The Fear & Greed collapse from 69 to 38 covered in Sentiment Snapshot explains why institutional behaviour shifted from buying everything to buying two names. And the VIX crossing 20 detailed in Volatility Lens is the mechanism that triggered the defensive sector rotation into utilities and energy.

This is analysis, not financial advice. Always manage your risk.

Deepen Your Understanding

Related articles from the Titan Protect Foundry: