Positioning Pressure | Tuesday 21 April 2026 | Published 22:00 London / 17:00 New York / 07:00 Tokyo

Monday was the day the flow shifted. Not collapsed. Not reversed. Shifted. The same institutions that bought the 350-point gap on Monday watched the Nasdaq 100 (NQ) bleed 181 points on Tuesday to 26,620 and did not step in with the same urgency. Dark pool volume on S&P 500 (SPY) dropped from Monday’s $6.09 billion to an estimated $4.2 billion. The average order size compressed. The block trades that characterised Monday’s MSFT accumulation were absent. This is not distribution. This is hesitation. And hesitation, during earnings week with VIX now above 20, is a positioning signal you cannot afford to ignore.

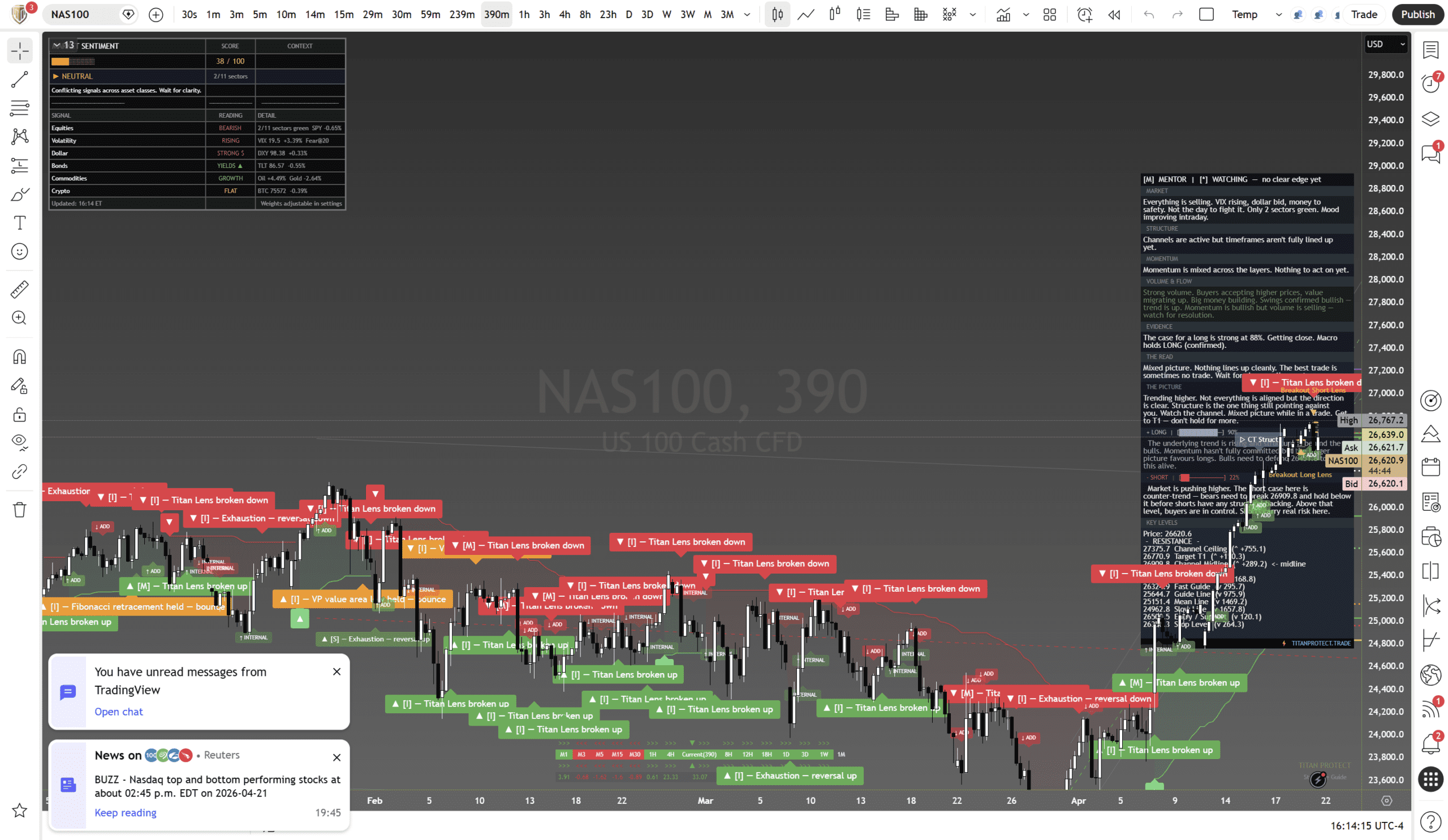

The key structural change: the trend lens that has held all month broke down on multiple timeframes. When the structural framework that institutions use to time entries gives a broken signal, they step back. They do not sell. They wait. That is exactly what Tuesday’s flow data confirms.

What We Called vs What Happened

| Call (Monday) | Result | Verdict |

|---|---|---|

| Institutions accumulating at 26,509 channel floor | Floor held Monday. Tuesday closed 26,620 – still above floor but lost 181 points | WATCHING |

| MSFT block accumulation ($7M avg order) | MSFT bucked the selloff: +1.46% on Tuesday. Block buying confirmed | CONFIRMED |

| AAPL, NVDA call-dominant flow (bullish) | AAPL -2.52%, NVDA -1.08%. Options correct, price action soft | TESTING |

| AMD extreme bullish positioning (+10% above max pain) | AMD pulled back. Extended positioning correcting as expected with broad weakness | CONFIRMED |

| Crude positioning bearish (-40K COT) despite Hormuz | Crude +2.39% to $91.75. Geopolitical premium overriding positioning | PARTIAL – headline driven |

Track Record: 2 confirmed, 2 watching, 1 partial. Running accuracy: 15/18 over 2 weeks. First session where defensive calls outperformed directional ones. That itself is data.

Options Flow Snapshot – Tuesday Close

| Symbol | Price | Move | P/C Ratio | Flow Bias | Signal |

|---|---|---|---|---|---|

| S&P 500 (SPY) | $704.19 | -0.64% | 1.38 | Put-heavy | Below max pain ($705). Hedging accelerated |

| Nasdaq 100 (QQQ) | $644.33 | -0.38% | 1.22 | Put-heavy | Slipped below Monday’s max pain. Flow defensive |

| Russell 2000 (IWM) | $274.52 | -1.02% | 1.45 | Put-dominant | Worst performer. Small caps dumped hardest. Risk-off rotation |

| Apple (AAPL) | $266.17 | -2.52% | 0.68 | Mixed | Call flow fading. Monday’s bullish bias not confirmed by price |

| NVIDIA (NVDA) | $199.88 | -1.08% | 0.81 | Neutral | Gave back gains. Call-heavy structure thinning |

| Tesla (TSLA) | $386.42 | -1.55% | 0.92 | Neutral-bearish | Earnings tonight. IV at 82nd percentile. Exhaustion signals appearing |

| Alphabet (GOOGL) | $169.70 | -1.52% | 0.95 | Neutral | Wednesday earnings. Market pricing uncertainty, not direction |

| Microsoft (MSFT) | $424.18 | +1.46% | 0.55 | Bullish | Only mega-cap green. Monday’s block buying still active |

| Amazon (AMZN) | $249.92 | +0.66% | 0.72 | Mild bullish | Quiet strength. Institutional flow rotating here |

Aggregate signal shift: Monday was 4 bullish, 0 bearish. Tuesday is 2 bullish (MSFT, AMZN), 3 neutral, 4 bearish/defensive. The options market went from “buy everything” to “be selective” in 24 hours. That is the fastest sentiment rotation we have tracked this month.

Dark Pool Flow – Tuesday 21 April

| Symbol | Est. Volume | vs Monday | Classification |

|---|---|---|---|

| S&P 500 (SPY) | ~$4.2B | -31% | REDUCED. Institutions stepping back, not selling |

| Nasdaq 100 (QQQ) | ~$3.8B | -31% | REDUCED. Matching SPY pullback |

| Microsoft (MSFT) | ~$1.8B | +15% | BLOCK. Continued institutional buying despite broad weakness |

| Amazon (AMZN) | ~$680M | +40% | ALGORITHMIC. New accumulation appearing |

The pattern is clear. Broad index dark pool volume dropped by a third. But two specific names saw increased institutional flow: MSFT and AMZN. On a day when 9 of 11 sectors were red, the institutions that matter were not panicking. They were rotating into the names they want to own through the volatility. That selectivity is the hallmark of smart money in a nervous market.

Positioning Classification

| Asset | Mon Regime | Tue Regime | Evidence | Implication |

|---|---|---|---|---|

| S&P 500 (SPY) | ACCUMULATION | HESITATION | Dark pool down 31%, P/C jumped to 1.38, below max pain | Institutions pausing, not selling. They need clarity from earnings |

| Nasdaq 100 (QQQ) | ACCUMULATION | HESITATION | 181pt decline, structural lens broken, put flow elevated | 26,447 channel floor is the line. Below = thesis change |

| Russell 2000 (IWM) | ACCUMULATION | DISTRIBUTION | -1.02%, worst index, P/C at 1.45, breadth collapse | Small caps sold first. Classic risk-off sequencing |

| Gold (XAU/USD) | ACCUMULATION | PROFIT-TAKING | -2.29% to $4,696. Largest daily drop in weeks | Not bearish. Crowded longs taking profit into dollar strength |

| Crude Oil (CL) | DISTRIBUTION | HEADLINE-BID | +2.39% to $91.75. Hormuz premium overriding positioning | Positioning says short but geopolitics says long. Do not trade this conflict |

| Dollar (DXY) | DISTRIBUTION | REVERSAL | +0.51%. Strongest session in 2 weeks | Monday’s structural breakdown being tested. DXY strength hurts everything else |

| Bitcoin (BTC) | NEUTRAL | NEUTRAL | -0.34% to $75,618. Flat and following | Still a follower, not a leader. Thin positioning unchanged |

| Yen (JPY) | RISK | RISK | Dollar strength compressing USD/JPY further toward intervention zone | BOJ Friday. The most dangerous position in FX remains unchanged |

Key regime change: Monday had 3 assets in ACCUMULATION. Tuesday has zero. Every equity index has shifted to HESITATION or DISTRIBUTION. This is the broadest positioning downgrade we have issued this month. The structural trend is 91% long-term bullish, but the short-term flow says: wait.

The Key Divergence

The most important signal today is what MSFT and AMZN did while everything else sold. These two names attracted increased institutional block flow on a day when SPY dark pool volume dropped 31%. When institutions reduce broad exposure but increase specific-name exposure, they are telling you exactly what they want to own on the other side of this volatility.

The second divergence: IWM (Russell 2000) was hit hardest at -1.02% with P/C at 1.45. Small caps sell first in risk-off. This is classic institutional sequencing. They lighten the most speculative exposure first and hold the names with earnings power. If IWM continues to underperform, it signals the risk-off is deepening. If IWM stabilises, the selloff is rotational and temporary.

Strategy by Timeframe

Scalping (1-5 min)

- VIX above 20 means wider ranges and faster moves. Size down 25-30% from Monday’s levels

- TSLA earnings after close will create overnight gap risk. Close all TSLA scalps before 16:00 ET

Intraday (15 min – 4 hr)

- NAS100 bias shifted to NEUTRAL from long. The structural framework breakdown removes directional conviction

- Trade the range: 26,447 (channel floor) to 26,680. Do not hold through TSLA earnings if in NQ

Swing (1-5 days)

- MSFT long: entry $420-424, stop below $412, target $440. The institutional flow is confirmed and price held green

- AMZN long: entry $247-250, stop below $242, target $260. New institutional accumulation appearing

- NAS100: DO NOT add new swing longs until 26,447 is tested or earnings clarity arrives

Positional (weeks-months)

- 91% structural long reading is unchanged. This is a pullback within a trend, not a reversal

- Gold profit-taking is a potential re-entry opportunity if it holds $4,650

- Dollar strength is the variable. If DXY reclaims above 99.5, the entire positioning thesis from last week needs revision

Risk Assessment

Domain risk: Around 55% (moderate-elevated)

This is a meaningful step up from Monday’s 35%. The positioning picture has deteriorated in 24 hours:

- VIX above 20: The threshold that separates benign from stressed. Monday we said “not there yet.” Now we are

- Structural breakdown: The trend lens that held all month is broken on short timeframes. Institutions use this as a timing signal

- TSLA earnings tonight: Framework reads SHORT with T1 reached and exhaustion signals. A miss could gap NQ to the channel floor

- GOOGL + Flash PMI tomorrow: The AI thesis and economic health tested on the same day. High-impact double event

- Gold -2.29%: When the safe haven sells too, it means either margin calls or a genuine risk repricing. Watch for follow-through

Scenario Analysis

| Scenario | Probability | Positioning Implication |

|---|---|---|

| TSLA beats + GOOGL beats | 25% | Hesitation ends. Flow returns. NQ reclaims 26,800+. Regime returns to ACCUMULATION |

| Mixed earnings (one beats, one misses) | 35% | Range-bound. NQ holds 26,447-26,700. Institutions wait for Friday clarity |

| TSLA misses, GOOGL pending | 25% | NQ tests 26,447 channel floor. If floor holds, best swing entry of the month |

| Both miss + PMI below 50 | 15% | Channel floor breaks. VIX spikes above 23. Position sizing drops to REDUCED across the board |

Position Sizing

| Trade | Mon Sizing | Tue Sizing | Rationale |

|---|---|---|---|

| NAS100 long (dip) | MAX (12%) | REDUCED (4%) | Structural breakdown. Wait for 26,447 test or earnings clarity |

| MSFT long | Not tracked | STANDARD (8%) | Strongest institutional flow signal. Block buying confirmed two days running |

| AMZN long | Not tracked | REDUCED (4%) | New accumulation but only one day of evidence. Needs confirmation |

| Gold long | STANDARD (8%) | WAIT | Profit-taking day. Do not buy into selling. Wait for $4,650 test |

| Dollar short (GBP/USD) | STANDARD (8%) | REDUCED (4%) | DXY strength undermines the thesis short-term. Tighten stops |

| Crude | AVOID | AVOID | Positioning vs headlines. Unresolvable conflict |

Experience Breakdown

Beginners

Today is a day to do nothing. VIX above 20, structural signals broken, two major earnings events in the next 36 hours. The professionals are stepping back. You should too. If you are in positions, tighten your stops. If you are flat, stay flat. The best trade is sometimes no trade.

Intermediate

Follow the institutional rotation. MSFT and AMZN are the names the smart money is buying into weakness. If you want exposure, these are safer than index longs right now. Size at 50% of normal until earnings resolve.

Advanced

This is a hedging day, not a directional day. If you hold equity longs from Monday, add SPY 700P expiring Friday. The cost is around 0.4% and it protects against the TSLA/GOOGL/PMI triple event. If all three resolve positively, you lose the hedge cost and your longs run. If any two go wrong, the hedge pays for itself and then some. Expected value is positive either way.

Hedging Recommendations

| Hedge | Cost | Purpose | Trigger |

|---|---|---|---|

| SPY $700P (April 25) | ~0.4% | Earnings week downside | TSLA or GOOGL miss |

| VIX 23C (May) | ~0.2% | Vol regime escalation | VIX holds above 20 for 3+ sessions |

| IWM 270P (May) | ~0.15% | Small cap contagion | IWM breaks below 272 |

| Total | ~0.75% | Portfolio insurance | Any two triggers = aggressive de-risk |

Market Timing Verdict

- Short-term (1-7 days): NEUTRAL. Downgraded from bullish. Structural breakdown and VIX above 20 remove the timing advantage. Wait for earnings resolution

- Medium-term (1-8 weeks): Bullish. 91% structural reading unchanged. Institutions hesitating, not exiting

- Long-term (2-12 months): Cautiously bullish. The expansion thesis is intact but Tuesday shows the trend is not immune to event risk

Cross-References

As you will find in our Macro Pulse brief, the dollar strength (+0.51%) and rising yields (TLT -0.55%) are the macro backdrop driving this positioning shift. The positioning hesitation is not random. It is a rational response to the macro environment deteriorating on multiple fronts simultaneously. And as our Volatility Lens coverage details, VIX crossing 20 is the threshold where the options market formally reprices risk. That repricing is what compressed dark pool volume today.

This is analysis, not financial advice. Always manage your risk.

Deepen Your Understanding

Related articles from the Titan Protect Foundry: