Pre-Asia Brief • Sunday 10 May 2026

Friday Delivered ATH, Gulf Faded, Tech Led by 2.35% — Sunday Opens Into a Market That Already Made Its Decision

🕐 Published 20:45 UTC | 04:45 SGT | 16:45 ET

Session Recap

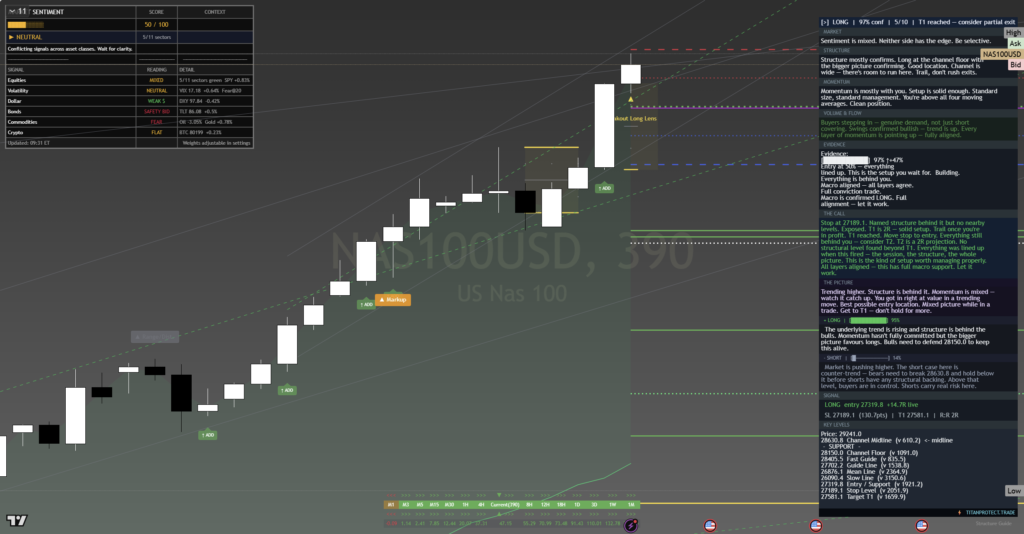

Friday’s US session resolved every open question simultaneously. SPY printed $737.62, a fresh all-time high, with the kind of conviction that only arrives when employment data lands clean and positioning is already loaded. NAS100 ripped 2.35% as AMD and the semiconductor complex led a tech rotation that forced shorts to cover into the close.

The Gulf premium evaporated in crude. WTI spiked to $98.25 mid-week on geopolitical headlines, then surrendered the entire move to close at $95.42, a 3.8% round-trip that tells you the market priced out imminent supply disruption. Dark pools printed $6.46B in SPY at the top decile of the last 52 weeks, which means institutional desks were actively adding, not distributing.

VIX settled at 17.19 with a flat term structure. No urgency to hedge. That is not complacency at an all-time high; that is consensus.

What We Called vs What Happened

“NFP is the binary resolver. Asia has 9 hours before the number lands. SPY is positioned at all-time highs. Gulf risk remains live but is being absorbed.”

Outcome: NFP resolved bullish. SPY confirmed the ATH. Gulf risk was fully absorbed (crude gave back 100% of the spike). The call was clean across all three vectors.

Asian Session Context

Sunday open is a continuation session. There is no new information to process. Markets are picking up where Friday left off, which means the gap risk is limited unless weekend headlines introduce a new variable.

HANG SENG

Watch

USD weakness supports HK but Gulf fade reduces oil importers bid

ASX 200

Bid

Commodity reset + US ATH = constructive open

Nikkei will likely lead. USD/JPY at 156.69 provides the carry tailwind that Japanese exporters love, and NAS100 +2.35% will translate directly into semiconductor and tech-heavy Nikkei longs. Expect quiet price action in the first 90 minutes, then a test of Friday’s momentum continuation.

Key Levels

| Instrument | Last | Entry (Long) | Stop | Target | R:R |

|---|---|---|---|---|---|

| NAS100 | 29,235 | 29,100 | 28,850 | 29,600 | 2.0:1 |

| SPY | 737.62 | 735.50 | 731.00 | 745.00 | 2.1:1 |

| Gold | 4,731 | 4,700 | 4,650 | 4,800 | 2.0:1 |

| WTI Crude | 95.42 | — | — | — | Avoid |

| BTC | 80,889 | 79,500 | 77,800 | 84,000 | 2.6:1 |

⚠ Crude Note

WTI surrendered the entire Gulf premium in a single session. That is headline-driven whipsaw territory. No clean level to anchor risk. Avoid until price establishes a new range, which likely takes 2-3 sessions.

Multi-Strategy Breakdown

Swing (3-10 days)

SPY ATH breakout continuation is the primary swing thesis. Entry on any 4H pullback to the 735 zone with a stop below 731. Target is measured-move extension to 745-750 over the coming week. NAS100 same logic, deeper pullback to 29,100 preferred.

Sizing: STANDARD

Positional (Asian Hours)

Asian session will be thin-liquidity continuation. Nikkei longs off the open if it gaps within 0.3% of Friday close. Gold likely holds bid in Asia as physical demand supports. BTC may drift sideways until European flow arrives.

Sizing: REDUCED (Sunday liquidity)

Scenario Analysis

| Scenario | Probability | Trigger | Action |

|---|---|---|---|

| Bull Continuation | 55% | Flat open, grind higher on Nikkei/tech | Add on pullbacks to key levels above |

| Sideways Digest | 30% | No new catalyst, thin Sunday volume | Hold existing, no new risk |

| Correction | 12% | Weekend geopolitical escalation, Gulf re-price | Stops honoured, reduce to AVOID sizing |

| Black Swan | 3% | Unexpected sovereign event, exchange halt | Flat immediately, reassess Monday |

Geopolitical Watch

The Gulf situation de-escalated on price alone. Crude giving back the entire spike tells you that physical supply was never genuinely threatened, or that the market has already priced an alternative route. Either way, the premium is gone and would need a new headline to rebuild. Watch for weekend commentary from OPEC+ members or any shipping lane disruption reports.

Trade policy remains in the background. No new tariff announcements pending, but the market is at all-time highs with DXY at 97.84, which means any surprise protectionist language would hit harder from this altitude.

Overnight risk is LOW. The weekend news cycle is empty of scheduled catalysts. The only variable is the unexpected.

Risk Assessment

Analysis Risk

Around 35%

Low-to-moderate. Skewed by Sunday liquidity, not by directional risk.

● VIX at 17.19, flat term structure — no hedging urgency, institutional confidence intact

● Fear & Greed at 66.9 (Greed) — elevated but not extreme, no contrarian signal yet

● Sunday liquidity — spreads wider, slippage risk higher, reduces confidence in tight entries

● Gulf premium removed — one less tail risk to price

● ATH positioning — breakout trades carry extension risk, stops must be mechanical

Position Sizing

| Tier | Condition | Applies To |

|---|---|---|

| STANDARD | Swing entries on Monday proper session | SPY, NAS100, Gold |

| REDUCED | Sunday Asian session (thin liquidity) | Nikkei, BTC, Gold |

| AVOID | No clean levels, headline-driven whipsaw | WTI Crude |

Monday’s Economic Calendar

| Time (UTC) | SGT | ET | Event | Impact |

|---|---|---|---|---|

| 01:30 | 09:30 | 21:30 Sun | China CPI/PPI (Apr) | Medium |

| 06:00 | 14:00 | 02:00 | German Industrial Production (Mar) | Low |

| 14:00 | 22:00 | 10:00 | US Senior Loan Officer Survey (Q1) | Medium |

| 17:00 | 01:00 Tue | 13:00 | US 3-Year Note Auction | Low |

| — | — | — | Fed speakers: Barkin, Williams | Medium |

Monday is a light calendar day. China CPI lands before most Western traders are awake, so any reaction will already be priced into Asian indices by London open. The Senior Loan Officer Survey matters for credit conditions but rarely moves markets intraday. Fed speakers may offer forward guidance that the bond market latches onto. Overall: no single-event binary risk on Monday.

Experience-Level Guidance

Beginner

Sunday open is not the time to initiate new positions if you are still learning risk management. The levels above will still be valid on Monday at full liquidity. Watch how price reacts to the Asian open, take notes on gap behaviour, and prepare your orders for the London session instead. The best trade you can make tonight is no trade at all until you see Monday’s first hour confirm direction.

Intermediate

You can participate in Asian hours with REDUCED sizing. Focus on Nikkei if it gaps within 0.3% of Friday close, or BTC if it pulls back toward 79,500 support. Keep stops mechanical. The temptation at all-time highs is to chase, but your edge is waiting for a pullback to a level, not paying up at the top of a candle. Size for the environment: Sunday liquidity is 40-60% of Monday’s.

Advanced

The dark pool print at $6.46B top-decile tells you institutions added Friday. The play is continuation until proven otherwise. Scale into swing longs on any 4H pullback into the entry zones. Crude is the contrarian opportunity if Gulf re-escalates, but only with event-driven sizing and defined stop. The term structure being flat means you can hold overnight without theta eating your hedge. Monday’s loan officer survey is the only data that could shift credit conditions narrative.

Analysis Bias

LONG CONTINUATION

ATH confirmed, institutional flow validated, Gulf risk removed, VIX flat, and the calendar is empty enough to let momentum carry through Monday without interruption.

Disclaimer: This content is for educational and informational purposes only. It does not constitute financial advice, a recommendation, or a solicitation to buy or sell any financial instrument. Trading involves substantial risk of loss. Past performance does not guarantee future results. Always conduct your own analysis and consult a qualified financial adviser before making trading decisions. You are solely responsible for your own trading outcomes.

© 2026 Titan Protect. All rights reserved.

Deepen Your Understanding

Related articles from the Titan Protect Foundry: