8 May 2026 | Sentiment Shift | the macro foundations

Wednesday’s sentiment analysis flagged Fear and Greed at 68.4, at what it called the 95th percentile of a 30-day range. The crowd was already positioned long, protection was being abandoned by retail, and institutions were hedging the Nasdaq specifically while the retail side sat complacent.

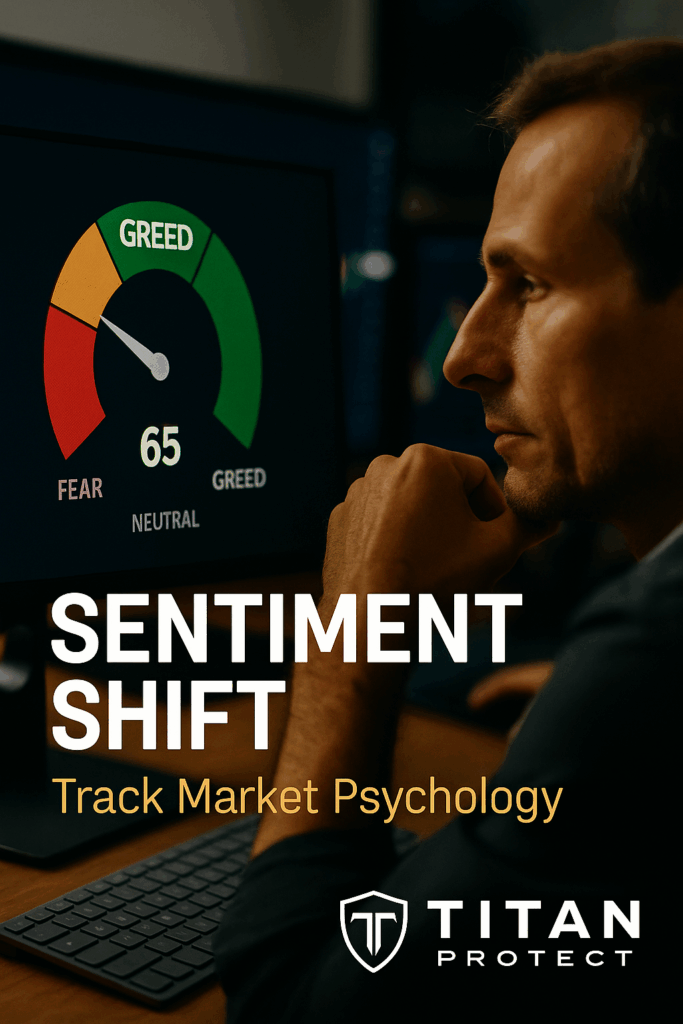

The data this morning tells a subtler story. Fear and Greed sits at 67.6, unchanged from yesterday. But in the context of the full 22-day range this indicator has traversed — from a low of 55.0 to a high of 69.9 — 67.6 places it at the 81st percentile. That is a meaningful reading. The crowd is still positioned for upside. The Gulf exchange of fire overnight has not yet moved the needle on this measure. That is either a sign of extraordinary market confidence, or a sign the crowd has not fully priced what happened.

Fear & Greed — Variance Context

F&G at 67.6, flat from yesterday’s 67.6. Over five days it is up 1.0 points, over ten days down 0.3 points. The 22-day average is 66.27. Current reading is 1.33 points above that average, sitting at the 81st percentile of the 22-day range (min 55.0, max 69.9). The 22-day range itself captures the recovery from the mid-April fear trough. The crowd that was panicking at 55 in mid-April is now sitting at 67.6 and will have to decide whether Gulf risk is reason to re-visit those lows or whether Wednesday’s ATH close means the fear was a buying opportunity validated.

The sentiment survey Data: Pessimism Is Easing, but Not Gone

The weekly sentiment survey Investor Sentiment Survey for the week ending 6 May 2026 shows: bullish sentiment 38.3%, neutral 28.7%, bearish 33.0%. The headline note from sentiment survey is “Pessimism Eases” — bullish sentiment rose 0.2 percentage points to 38.3%, only marginally above the historical average of 37.5%.

Compare that to the prior week: bullish 38.1%, bearish 39.7%. The bearish reading has fallen from 39.7% to 33.0% in one week — a 6.7 percentage point swing. But the bulls have barely moved (38.1% to 38.3%). The big shift was from bears to neutral. Investors are not rushing to the long side. They are moving from actively pessimistic to “wait and see.” That nuance matters. Neutral at 28.7% versus the historical average of 31.5% is slightly below average, meaning the wait-and-see crowd is not as large as it typically is — the bears who moved toward neutral went partially but not entirely.

sentiment survey Sentiment — Weekly Survey Progression

| Week Ending | Bullish | Neutral | Bearish | Bull-Bear |

|---|---|---|---|---|

| Historical Avg | 37.5% | 31.5% | 31.0% | +6.5% |

| 15 Apr 2026 | 31.7% | 25.5% | 42.8% | -11.1% |

| 22 Apr 2026 | 46.0% | 19.5% | 34.4% | +11.6% |

| 29 Apr 2026 | 38.1% | 22.2% | 39.7% | -1.6% |

| 6 May 2026 | 38.3% | 28.7% | 33.0% | +5.3% |

The bear reading of 33.0% is above the historical average of 31.0%. The market is at all-time highs and still 2 percentage points more bearish than the long-run average. That combination — ATH equity prices alongside above-average retail bearishness — is not typical. It can be read as a wall of worry that supports further upside (the classic contrarian signal), or as a recognition that macro conditions are genuinely more uncertain than the price suggests.

The Put/Call Shift: Retail vs Institutional Divergence Widens

As Post 00 covered, the overall gex-max-pain-and-putcall-ratios/” style=”color:#D8AF44;text-decoration:underline” title=”What is Options Intelligence?”>put/call ratio moved from 0.658 to 0.737 between Wednesday and Thursday. That is a 12% single-session increase in protection-buying. The SPY volume put/call ratio sits at 1.13 and the SPX volume put/call ratio at 1.21 — both indicating more puts traded than calls in volume terms, flagged as “bearish sentiment” by the options data.

The split between retail and institutional interpretation remains important. The total open interest put/call on SPY is 2.38 overall, and 2.71 on today’s specific expiry. These are not retail traders buying weekly puts to gamble on a crash. These are systematic hedge programmes maintaining exposure. The divergence Wednesday’s sentiment post described — retail complacent, institutions hedged — has not resolved. If anything, the rising put/call in total market terms suggests the institutional hedging programme expanded overnight, likely in response to the Gulf news.

Sentiment Metrics — Variance Context

| Metric | Today | 1d Delta | 5d Delta | 22d Percentile |

|---|---|---|---|---|

| Fear & Greed | 67.6 | 0.0 | +1.0 | 81st |

| SPY P/C (flow) | 0.737 | +0.079 | Rising | Elevated vs WTD |

| SPY OI P/C (total) | 2.38 | — | — | Defensive |

| SPX IV (30d) | 14.27% | — | — | 23rd IV rank |

| sentiment survey Bull | 38.3% | +0.2pp | Flat | Just above avg |

| sentiment survey Bear | 33.0% | -6.7pp | Falling | Above long-run avg |

BTC: The Canary in the Risk Appetite Coal Mine

BTC closed at $79,590, down approximately $183 from the prior day close. Over five days it is up 1.94%, and over ten days up 3.48%. The 22-day range runs from a low of $74,805 to a high of $80,927. At $79,590, BTC sits at the 24th percentile of that range. That is a notable divergence from SPY’s 99.9th percentile position.

When equities are at all-time highs and crypto is sitting near the lower quarter of its 22-day range, the risk appetite signal is split. BTC is not a perfect equity analogue, but it functions as one of the more sensitive real-time sentiment readings available. Institutional adoption has made it less volatile than in prior cycles, but its 22d percentile at 24% while SPY is at 99.9% is a divergence the analysis takes seriously. It suggests the broad risk-on crowd is more selective than headline equity prices indicate.

BTC vs SPY Divergence — Variance Read

SPY: 99.9th percentile 22d range. BTC: 24th percentile 22d range. This is not the alignment you would expect in a clean risk-on environment. Either BTC is lagging and will catch up (bullish crypto near-term), or BTC is leading the broader market toward mean reversion and equity is the asset that is temporarily elevated. The framework does not adjudicate which interpretation is correct — both scenarios require monitoring. What the data makes clear is that the two assets are pricing different things, and that divergence carries into Friday’s binary catalysts.

IWM Breadth: The Divergence That Compounds

IWM’s -1.58% session on Wednesday is the breadth warning that Post 00 and Post 01 have each referenced. From a sentiment perspective, what IWM’s underperformance means is straightforward: the crowd is not broadly positioned for economic expansion. Small-caps are rate-sensitive, bank-loan dependent, and domestically exposed. When they underperform large-caps by 1.3 percentage points on a day the S&P 500 is at record highs, it is the market telling you the rally is narrow, driven by a handful of mega-cap names, and that the macro optimism being priced by those names has not translated into the broader economy.

Wednesday’s sentiment post called “wait for NDTH above 60% before adding new exposure” — the percentage of Nasdaq stocks above their 200-day moving average. That level was 55.44% then. The IWM session confirms the call was correct. Adding exposure into narrow leadership at ATH, with IWM cracking and breadth indicators below the 60% threshold, remains a premature move.

The Crowded Trade Problem

The sentiment survey data offers an important long-run context point. The 1-year bullish high was 49.5% (week ending 14 January 2026). The 1-year bearish high was 52.0% (week ending 18 March 2026). Today’s 38.3% bullish and 33.0% bearish readings represent a middle state — not extreme greed, not extreme fear, but with F&G at the 81st percentile of its 22-day range, the short-term momentum is leaning greedy.

The crowded trade risk is not that sentiment is extreme by historical standards. It is that a 0.737 put/call ratio heading into a weekend with a Gulf conflict unresolved and NFP to digest means any surprise to the downside — either in the jobs data or in overnight geopolitical developments — would find a crowd that is net long, reasonably unprotected at the retail level, and facing a sentiment measure that is already in the upper fifth of its recent range. The path of least resistance for a sentiment shock is lower, not higher, from this configuration.

Sentiment Scorecard — Thursday 8 May 2026

| F&G Score | 67.6 — 81st percentile, 5d avg 67.3 |

| sentiment survey Bull/Bear Spread | +5.3% — back above neutral line |

| P/C Trend | Rising (0.658 → 0.737) — protection being added |

| BTC 22d Percentile | 24th — diverges sharply from SPY 99.9th |

| IWM Breadth Signal | -1.58% session, confirming narrow advance |

| Institutional Options Bias | Bearish QQQ + IWM; Bullish single names |

| Overall Sentiment Read | Controlled greed — not complacent, not panicked |

What Sentiment Needs to Do to Confirm the Advance

For the sentiment picture to validate further upside from ATH, three things need to happen. First, IWM needs to stop underperforming — breadth needs to broaden, not narrow. Second, the put/call ratio needs to stop rising — if it continues through 0.8 or higher, it signals systematic risk reduction rather than systematic hedging. Third, BTC’s 22d percentile needs to converge toward SPY’s — the risk appetite divergence should close if the macro backdrop is genuinely supportive.

None of these are forecasts. They are the conditions the analysis would need to see before the sentiment picture moves from “cautious greed” to “constructive accumulation.” Thursday’s session, with Gulf risk and 32 earnings in the background, is not likely to resolve any of these cleanly. NFP on Friday is the sentiment reset button regardless of direction.

Post 03 closes the loop on the volatility picture: VIX at the 27th percentile of its 22-day range while risk events multiply, and what that means for how the market prices uncertainty into the weekend.

This analysis is for informational purposes only and does not constitute financial advice. Past performance is not indicative of future results. All trading involves risk.

Deepen Your Understanding

Related articles from the Titan Protect Foundry: