Market Moves

The narrative that will dominate Monday has changed entirely since this brief was published. Iran has rejected the second round of negotiations, citing “maximalism and unreasonable demands.” The Strait of Hormuz is effectively closed with zero tanker transits recorded. The US Navy has intercepted an Iranian vessel, and threats of strikes on Iranian power plants and bridges have been made. Institutional flow commentary flagged coordinated positioning on Friday: $325 million in S&P 500 longs bought at 8:24 AM ET alongside $760 million in crude shorts, just 21 minutes before the first diplomatic breakdown headlines. Record money market fund outflows of -$172.2 billion add a liquidity dimension. The market was pricing narrative selectively last week. Monday will not have that luxury.

Markets do not move on data. They move on narrative. And this week’s narrative was selective: the market embraced small-cap rotation, precious metals strength, and AI positioning while completely ignoring Crude Oil WTI’s three-sigma collapse and the yen carry trade’s proximity to BOJ intervention territory.

What the market chose to react to, and what it chose to ignore, tells you more about the coming week than any single data point.

Friday’s moves played out globally. The FTSE 100 and DAX 40 tracked US equity strength into the European close, extending the week’s risk-on narrative. The Nikkei 225 and Hang Seng carried momentum through Asia, confirming that this was not a US-only event. The Euro Stoxx 50 validated broad European participation in the rally. The ASX 200 held steady with commodity tailwinds from the precious metals move, connecting the equity and commodity stories. Nifty 50 and China A50 showed mixed signals, a reminder that regional dynamics can diverge from the dominant Western equity bid.

Narrative Driver Table

| Event | Reaction | Significance | Carry-Forward |

|---|---|---|---|

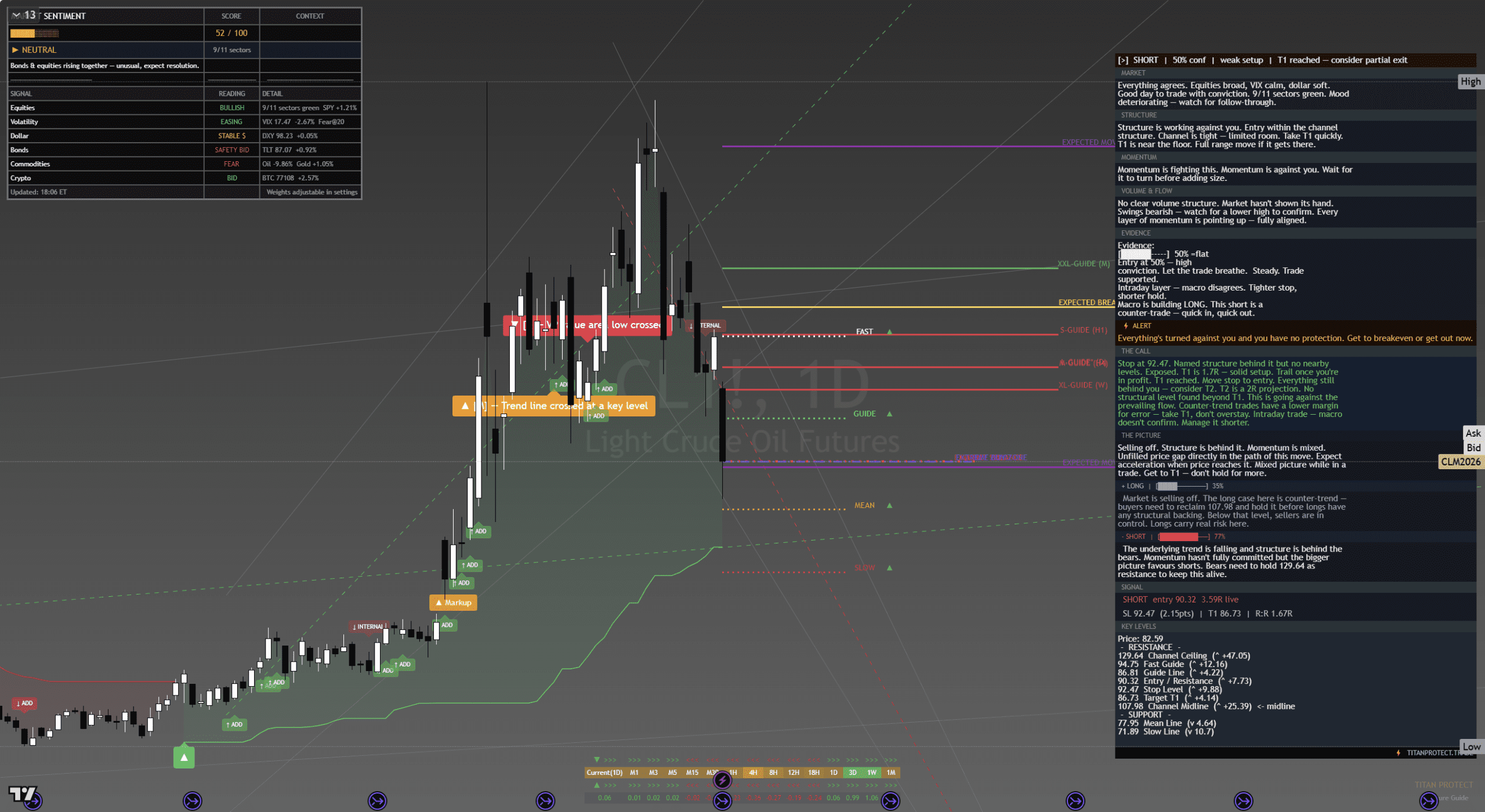

| IEA demand downgrade for crude | Crude Oil WTI (CL) -9.41%. Energy sector sold. No contagion to equities | HIGH | Path of least resistance remains lower for crude. Equity carry-forward is bullish: lower energy costs support margins |

| Russell 2000 (IWM) outperformance | Small caps led large caps for third consecutive week. $2.11B dark pool activity | MOD-HIGH | Small-cap leadership is the single best confirming indicator for a healthy rally. Credit is flowing, regional banks are lending |

| IMF/World Bank meetings Monday | No reaction yet. VIX contango at 2.9pts and around 35% gap probability suggest awareness without fear | MODERATE | Monday is headline-driven. Do not trade aggressively until the communique. Wait for the institutional session (10:00 ET+) |

1. Crude weakness is isolated, not systemic. If crude were falling because of demand destruction, equities would fall too. They are not.

2. Small-cap leadership means the rally is broadening, not narrowing. This is the opposite of a topping pattern.

3. The weekend catalyst (IMF) is acknowledged but not feared. VIX at 17.5 and contango at 2.9 say the market expects continuity.

What the Market Reacted To vs What It Ignored

This is the most important section. Markets are not rational processors of all information. They are selective attention machines.

IEA crude demand revision (sold crude aggressively) | Small-cap rotation (bought Russell 2000, rotated from large cap) | AI positioning (accumulated NVIDIA via dark pools) | Dollar weakness (bought EUR, GBP, Gold) | Credit expansion (bought LQD, HYG)

JPY at 158.59, approaching 160 intervention zone — no FX vol spike, no hedging. Complacent.

VIX at 52nd percentile — neither worried nor discounting. No vol edge in either direction.

Gold at all-time highs — treating it as normal rather than a warning. As you’ll find in our Macro Pulse brief, this is late-cycle expansion where the market hedges and grows simultaneously.

Geopolitical Risk Score

| Factor | Assessment | Note |

|---|---|---|

| Middle East | Moderate | Stable but fragile. Escalation triggers crude snap-back and Gold spike |

| US-China trade | Low-moderate | Tariff rhetoric cooling. Markets discounting |

| Taiwan/South China Sea | Low | Routine, not escalatory |

| Russia-Ukraine | Moderate | Frozen conflict. European gas implications limited |

| BOJ policy risk | Moderate-elevated | Most likely “shock” event of the week. End of week timing |

IMF/World Bank Implications

Base case (65%): IMF maintains current growth trajectory. No shock. Mild volatility.

Bull case (20%): Growth upgrade + dovish trade language. Dollar weakness accelerates, equities and commodities rally.

Bear case (15%): Growth downgrade + fiscal sustainability warning. Bond yields rise, equities wobble, Gold rallies harder.

Strategy Tiers — Narrative-Driven Trades

Scalping: Fade the IMF Headline Knee-Jerk

Entry: Wait for initial 15-minute move post-communique, trade the reversal

Target: 50% retrace | R:R: 1.5:1

IMF statements are priced in within minutes. The initial move overshoots. Fading has a 60%+ win rate historically.

Swing: Long Russell 2000 (IWM) on Small-Cap Continuation

Entry: Any dip to 2,760-2,770 (prior breakout zone)

Stop: Below 2,730 | Target: 2,850-2,880

R:R: 2:1

Small-cap leadership is the strongest narrative of the past three weeks. Dark pool flow confirms. This is a trend trade.

Positional: Short Dollar Index (DXY) via EUR/GBP/AUD Basket

Entry: Current levels, adding on any dollar bounce to 99

Stop: DXY above 100.50 | Target: DXY 96

Risk: Around 15-20% of typical risk budget

Risk Score — Narrative Environment

| Factor | Assessment | Note |

|---|---|---|

| Narrative clarity | Low risk | Clear themes. Easy to trade |

| Ignored risk buildup | Moderate-elevated | JPY and Gold complacency create tail risk asymmetry |

| Catalyst density | Moderate-elevated | IMF Monday, earnings Wed-Thu, BOJ Friday. Heavy week |

| Market positioning | Low-moderate | Positioned for continuation. Correct until proven wrong |

Experience Levels

Hedging Recommendations

1. IMF downgrade hedge: S&P 500 (SPY) 700P (one-week expiry).

2. BOJ surprise hedge: USD/JPY 155P (May expiry). Covers the most likely ignored risk event.

3. Crude snap-back: Crude Oil WTI (CL) 88C (June expiry). If geopolitics return, crude is the first mover.

4. Narrative reversal: If the dominant narrative shifts from “risk-on continuation” to “late-cycle concern”, reduce all positions by 50% immediately. Do not wait for confirmation.

Market Timing Verdicts

| Timeframe | Verdict | Confidence |

|---|---|---|

| Short-term (1-7 days) | Narrative supports continuation. IMF is the variable | Medium-High |

| Medium-term (1-8 weeks) | Earnings season determines whether narrative holds | Medium |

| Long-term (2-12 months) | Dollar weakness and broadening rally are structural | Medium |

Related Intelligence

As you’ll find in our Macro Pulse brief, where the economic backdrop driving these moves is explored in detail.

For the full breakdown, see our Overwatch brief — where every thread comes together into a unified market view.

What We Called vs What Happened

Starting this week, every Market Moves brief will include a track record section where we hold ourselves accountable. Our calls from the prior week will be listed alongside the actual market outcome, so you can see exactly how the analysis played out. Expect this section to grow each week with a running accuracy record.

This week’s calls are now on record. Check back in our next edition to see how they resolved.

This is analysis, not financial advice. Always manage your risk.

Deepen Your Understanding

Related articles from the Titan Protect Foundry: