Volatility Lens | Sunday 3 May 2026 | Weekend Read — Monday Open Setup

The vol curve is telling two stories simultaneously and only one of them is getting attention. The headline story — VIX at 16.99, its lowest weekly close since late April, front-end VIX9D at 14.15 — looks like an all-clear. The second story, buried one layer deeper, is VVIX at 95.17 and rising from Thursday’s 93.70: the cost of hedging volatility itself is still elevated, meaning the professionals who set prices in the vol market are not as sanguine as the VIX headline suggests. Steep front-end backwardation paired with elevated vol-of-vol is not a contradiction — it is a specific regime that tends to precede continued trending price action in the underlying, but with a warning attached: when that VVIX premium eventually unwinds, it does so fast. Friday’s record close on SPX happened on declining spot vol but accelerating VVIX. That divergence is Monday’s entire story. The NDX expected move into Monday’s close is $228.50 — just 0.82% — telling you the options market expects a quiet open. The question is whether the quiet is genuine or whether it is the silence before the VVIX premium reprices.

Core Vol Thesis — Weekend Into Monday Open

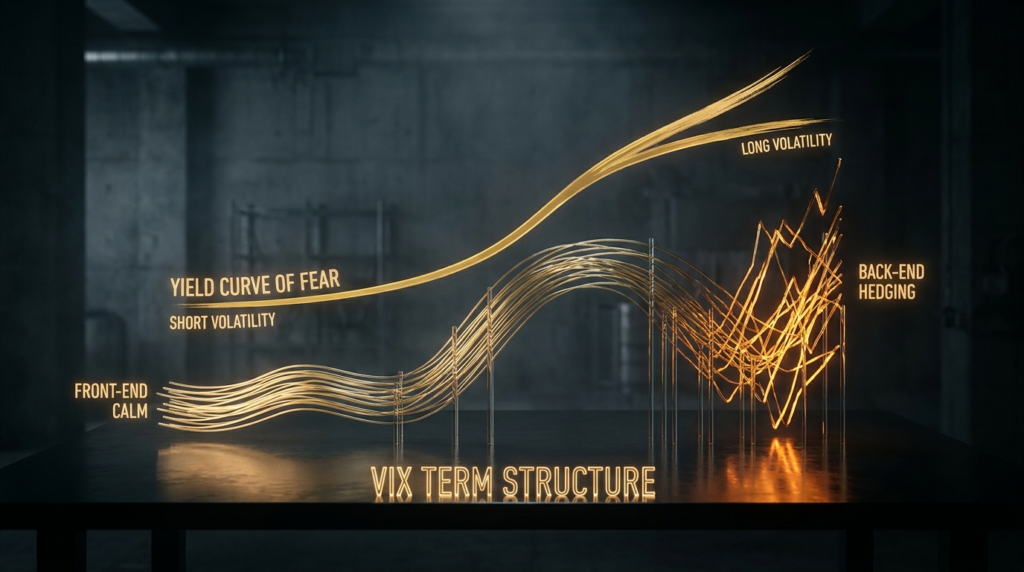

The VIX term structure is in bullish backwardation: VIX9D 14.15, VIX spot 16.99, VIX 3M 21.37. That 2.84-point gap between nine-day and one-month vol, and the further 4.38 points to three-month, is the widest front-to-back spread since mid-March. Historically this specific combination — compressed front end, elevated back end, positive SPX momentum — is one of the more reliable continuation setups in the volatility playbook. Vol sellers are comfortable taking the front premium while hedgers are buying longer-dated protection. That is not a fear trade; that is positioning for a trending market with tail protection. The smoking gun is VVIX at 95.17. Vol-of-vol at that level means professionals are paying up to hedge their hedges. The surface looks calm. Underneath it, the cost of being wrong is priced at a level that warrants respect. SPY max pain for Monday’s expiry sits at $714 — six dollars below Friday’s close — which tells you the gravitational pull is slightly lower, but with price at 720.65 and SPX GEX concentration at 7250-7280, the dealer gamma structure actively resists sharp moves in either direction on the open.

1. The Term Structure — Reading the Curve That Professionals Actually Trade

Most market participants look at VIX and stop there. That is like checking the temperature without looking at the pressure chart — you know if it is warm or cold, but you cannot tell whether a storm is coming. The vol term structure — the relationship between VIX9D, VIX spot (30-day), and VIX 3M — is where the actual information lives. Friday closed with a configuration that is worth unpacking carefully because it is doing something specific.

VIX9D at 14.15 represents the market’s expectation of realized volatility over the next nine calendar days. It collapsed from 14.37 on Thursday, driven by the PCE-in-line print clearing the dominant near-term event risk. When a data point the market has spent two weeks pricing resolves cleanly — 2.5% PCE, exactly at consensus — the nine-day vol simply deflates. The uncertainty premium that was baked in for that specific outcome evaporates within minutes of the release. That is mechanics, not signal.

VIX spot at 16.99 is a different story. One-month implied vol did not follow the nine-day lower with any conviction. It closed at 16.99 — fractionally above Thursday’s 16.89. On a day where equities made record highs and the primary data catalyst printed benign, the front-month vol barely moved. That residual premium reflects something that PCE did not resolve: the broader macro backdrop of a Fed that has not cut, a dollar testing support at DXY 98-99, yen carry flows that remain live, and a geopolitical picture that has not simplified. The one-month window still has ISM Services on Tuesday, the 30-year auction on Wednesday, and initial claims on Thursday. Those are not VIX-moving events in isolation, but they keep the bid under medium-term vol.

VIX 3M at 21.37 is the most telling number on the board. Three-month vol pricing at 21.37 while spot trades at 16.99 represents a 4.38-point slope — steep by any recent comparison. That back-end premium is the market embedding uncertainty about events that do not even exist on the calendar yet: the next Fed meeting cycle, Q2 earnings season beginning in earnest, whatever tariff or geopolitical development may be lurking in the June-July window. Professionals who manage macro risk books cannot see around that corner, so they pay for the optionality.

The steepness of this curve is not a recent phenomenon — it has been building since the tariff volatility of March and April compressed medium-term vol upward while spot vol repeatedly failed to sustain its spikes. What PCE did on Friday was validate the front-end compression without resolving the back-end question. That is the setup Monday inherits.

2. VVIX at 95 — Why the Surface Is Misleading You

VVIX measures the implied volatility of VIX options — specifically, how much the market expects VIX itself to move. When VIX spot is at 16.99 but VVIX is at 95.17, you have a market saying two things at once: “I expect the next nine days to be quiet” and “but I am willing to pay a premium price to insure against VIX spiking.” Those are not contradictory statements if you understand who is making them.

The front-end vol compression is driven by the retail and systematic options-selling community — the income generators, the covered-call writers, the short-volatility funds that have proliferated in the current low-vol regime. They are comfortable selling weekly premium at VIX 17 because recent realized vol has been lower. The VVIX bid at 95 is driven by a different constituency entirely: the macro hedge funds, the bank prop desks, the sovereign wealth managers — the people who do not care about premium income but need to protect large books against a scenario where vol itself re-accelerates. They are buying VIX calls not because they think it will happen, but because the cost of being caught without that protection in a vol spike is catastrophic for their portfolios.

That VVIX closed at 95.17 on Friday — and rose 1.47 points on a day when SPX hit a record — is the tell. When institutional hedgers are increasing their vol-of-vol exposure on the same session that the underlying is printing all-time highs, they are not doing it because they are bearish on equities. They are doing it because they know the vol surface that has been supporting this rally is not as stable as it looks. The institutional flow analysis built into this weekend’s positioning read — where dealer books were systematically reducing short hedges into the PCE print — confirms exactly this bifurcation: equity desks leaning long, vol desks buying tail protection simultaneously.

At 95.17, Monday inherits a market that is five VVIX points away from the stress threshold. That is not a reason to be bearish — the gap to 100 is real — but it means the margin for error on any unexpected news is tighter than the VIX surface suggests. The sentiment read from this weekend, where Fear and Greed sits at 66.6 in greed territory but cooling from the prior week’s 67.4, aligns with this — the crowd is greed-positioned, the institutions are hedged. Both can be right until one of them isn’t.

3. The Disconnect — Spot Vol Whispers Calm, Vol-of-Vol Shouts Hedged

Here is the tension that defines Monday’s trade. VIX at 16.99 is the number that gets screenshotted, tweeted, and used to justify being long equities into the open. It is a real data point. It means near-term implied volatility is compressed relative to the average of the past twelve months. It is consistent with a trending market, supportive of momentum continuation, and historically associated with positive forward equity returns over the next two to four weeks.

VVIX at 95.17 and rising is the number that does not make the screenshot. But it is also a real data point. It means that the people with the largest vol books — the ones who set the price of VIX options — closed Friday paying more for insurance against VIX spiking than they did on Thursday. On a day when equities hit records. That is not something you do because you believe everything is fine. You buy VIX calls at elevated VVIX because you think there is a non-trivial probability that the calm surface breaks and the feedback loop through dealer gamma books accelerates any move. The record close on SPX happened on declining VIX but accelerating VVIX. That is a split verdict, not a clean all-clear.

The practical implication: spot vol is whispering “calm, trend continuation, premium cheap to buy.” Vol-of-vol is shouting “still hedged, still seeing tail risk that is not reflected in the headline number.” Both are right. They are addressing different time horizons and different risk profiles. A trader sizing aggressively into Monday based purely on VIX 16.99 is reading half the story. A trader paralyzed by VVIX 95 and refusing to participate in a trending market is reading the other half in isolation. The correct read holds both in tension simultaneously: position for continuation with appropriately sized risk, and use the cheapness of near-term vol to add protection that VVIX tells you is worth having.

The macro picture — PCE cleared, week-ahead data light, ISM Services as the primary event Tuesday — confirms the directional bias without removing the vol uncertainty. The institutional flow read, where dealer positioning showed systematic reduction of short hedges into the print, is consistent with a market leaning constructive. But that same read showed the darkest flow — the multi-week institutional campaigns — sitting in tech names specifically, with broader market breadth already thinning. Concentrated leadership in five or six mega-cap names is exactly the kind of structure that keeps VIX elevated above where pure equity momentum would suggest, because the single-name vol does not cancel out across a narrow basket.

4. Gamma Exposure and Expected Moves — Where the Magnetic Levels Sit for Monday

The vol curve tells you the price of uncertainty. The gamma structure tells you where the market expects price to be anchored and where it expects acceleration if those anchors break. For Monday, the gamma picture is cohesive across SPY and NDX.

SPY’s max pain for Monday’s expiry is $714.00, sitting $6.65 below Friday’s close of $720.65. Max pain is not a price target — the market rarely gravitates there during the session — but it tells you where the aggregate open interest creates the maximum optionality loss for buyers. The more relevant observation is that max pain has been drifting upward through the expiry stack: $705 for May 8, $713-715 through the May 11-14 window, with the notable exception of the May 15 monthly at $690 — the first expiry where max pain drops significantly below current price. That monthly max pain at $690 represents a 4.2% discount to current levels and is where the structural put wall begins in earnest. Between 714 and 720, the dealer gamma book is broadly neutral to slightly supportive — neither a strong magnetic pull lower nor a strong push higher.

The NDX expected move for Monday is the precision data point here. At $228.50 — a range of $27,471 to $27,928 on either side of Friday’s $27,699 close — the options market is pricing just 0.82% of movement in either direction for the entire Monday session. That is exceptionally tight. It reflects the combination of compressed front-end vol (VIX9D at 14.15), no catalyst on the Monday calendar, and the positive gamma positioning from the quant community that has noted SPX concentrating around 7250-7280 as a GEX and DEX magnet.

The gamma structure across SPY and QQQ confirms what the term structure implies: Monday should be range-bound in the early session. The NDX expected move of just 0.82% is historically tight for a Monday open, suggesting the options market is not pricing in any gap risk from the weekend. That could be the correct call — there is no major catalyst scheduled — or it could be precisely the moment where the VVIX premium justifies a small tail hedge, because when the market is priced for quiet and quiet does not arrive, the delta-hedge flow from dealers amplifies the initial move.

The quant flow picture — with SPX GEX and DEX concentration at 7250-7280 — means there is a magnetic zone roughly 150-300 NDX points above Friday’s close. If price tests into that zone in the Monday session, dealers who are long gamma there will actively sell into it, capping the move. That is the call-dominated structure creating friction at the highs. Below the current price, the put gamma wall sits more diffusely — which means a downside break accelerates faster than an upside push, everything else equal.

5. The Vol Surface — How NDX Expected Moves Scale Through the Week

The NDX expected move table gives one of the clearest pictures of how the options market calibrates uncertainty as time extends. Reading it horizontally tells you what the market thinks can happen over each window. Reading it in context of the vol term structure gives you the full picture.

The implied vol column is what makes this surface interesting. Monday’s NDX options price at 11.64% implied vol — that is the cheapest forward vol available anywhere on the NDX term structure. Every subsequent expiry prices higher, with the monthly at 17.98% still well above the 11.64% entry point for Monday. This steep implied vol curve from Monday outward is the options market’s way of saying: Monday is priced for quiet, but the risk that the week-ahead data reasserts itself (particularly ISM Services Tuesday) creates vol premium at each subsequent step.

The practical implication for Monday: selling premium into the open is an expensive exercise — the surface is not offering rich enough premium in the near-term expiry to justify the tail risk. Buying protection for Monday is cheap (11.64% IV). Using Monday’s quiet to position for the Tuesday ISM Services reaction — where implied vol steps to 13.89% — is the vol structure’s silent recommendation. The macro read from this week, noting ISM Services Tuesday as the single major data event, aligns perfectly with that setup.

6. SPY and QQQ Greeks — What the Delta, Gamma, and Vega Curves Are Actually Telling You

The Greek charts for SPY and QQQ on the May 4 expiry tell a consistent story when read together. Delta transitions through zero — the at-the-money inflection — at the $720 level for SPY and $674 level for QQQ. That is exactly where Friday’s closes landed. When a liquid instrument closes precisely at the delta-neutral point on the options chain for the next-day expiry, it is not coincidental — it reflects the gravitational pull of dealer delta hedging that dragged price toward maximum dealer gamma neutrality into the close.

The SPY gamma chart peaks at the $720-725 zone for the May 4 expiry, with gamma ranging up to 0.081 at the peak. That means a $1 move in SPY at the current level requires dealers to adjust their hedge by 0.081 contracts for every option contract they hold. With hundreds of thousands of contracts clustered around that strike — as Friday’s volume data confirmed — the aggregate delta-hedge flow from a $1 move is enormous. That is what creates the “magnetic” behavior at these levels: dealers are constantly rebalancing, which creates flow in the direction of current momentum but limits acceleration at the gamma peak.

The vega picture is equally important for Monday’s risk framing. Vega peaks at the ATM strike (720 SPY, 673 QQQ) and decays rapidly in both directions. Vega ranging up to 0.26 for SPY at-the-money means every one percentage point change in implied vol costs or earns $0.26 per option on a single contract. With Friday’s VIX at 16.99 and the VVIX warning that vol could reprice, any position that is heavily long vega at these ATM strikes is exposed to vol compression risk if Monday opens quietly — which the NDX 0.82% expected move suggests is the base case. Conversely, if VVIX leads vol higher unexpectedly, those same ATM vega-long positions benefit substantially.

The theta profile is the Monday-specific warning for options buyers. With theta at negative 0.85 for SPY ATM and negative 0.92 for QQQ ATM on the May 4 expiry, every hour of Monday that passes without movement costs the option holder in premium decay. In a quiet open — which the NDX expected move of 0.82% anticipates — buying Monday ATM options and hoping for movement is a losing strategy unless the move arrives in the first ninety minutes. The vol surface is designed to punish late-Monday momentum trades.

7. Three Monday Scenarios Through the Vol Lens

The vol structure does not tell you which direction the market moves. It tells you what the market is priced to handle and where the structure breaks. Applied to Monday’s specific setup, three scenarios emerge from the data.

Scenario A: Quiet Continuation — 50% Probability

NDX opens within the $228.50 expected move window ($27,471-$27,928). SPY holds above $716 through the first hour. VIX9D stays below 15.00. VVIX drifts toward 93-94 as Friday’s institutional hedge buying does not repeat on a quiet Monday. Dealer gamma stays positive — market grinds higher or sideways with limited intraday range. SPX tests the 7250-7280 GEX/DEX magnet zone flagged by the quant desk analysis. The week-ahead light data calendar provides no catalyst to disrupt the positive momentum inherited from Friday’s record close. Volume is below average. The vol surface continues to compress the front end while the back end holds elevated. This scenario validates the PCE-cleared continuation thesis from the macro read. Vol sizing: positions sized at STANDARD or below, with the recognition that premium-selling strategies benefit from ongoing theta decay and the quiet open. The 720 pin on SPY holds as the gravitational center through the session.

Scenario B: Vol Drift With Narrowing Range — 35% Probability

NDX opens flat to slightly lower, testing the lower end of the expected move window near $27,471. VIX9D drifts to the 15.5-16.0 range as weekend positioning unwinding creates modest spot vol demand. VVIX holds or edges above 96, maintaining institutional hedge demand. SPY oscillates between $716-$722 without committing to direction. The breadth picture — which the sector and hot zones read this weekend identifies as already thinning — fails to improve on the open, with the Monday session showing tech flat and the Dow lagging again. The call-dominated GEX structure creates a ceiling at the $27,700-$27,800 zone where dealer selling caps upside. Price grinds sideways with realized vol coming in below the 11.64% implied level for Monday’s expiry — a positive outcome for premium sellers, negative for directional buyers. The VVIX premium of 95-96 is sustained without resolving, meaning the tension between surface calm and institutional hedging continues into Tuesday. Vol sizing: REDUCED. The market is not offering a clean directional setup. The best trade is patience ahead of ISM Services Tuesday.

Scenario C: VVIX Feedback — Vol Reprices — 15% Probability

An unexpected weekend development — geopolitical, tariff-related, or Asian session weakness — causes NDX to open below the $27,471 lower bound of the expected move. VIX spikes through $18.00. VVIX accelerates through $97-98 toward the $100 stress threshold. The dealer gamma structure — which has been positively reinforced at current levels — flips negative below $714 SPY and $670 QQQ, creating the feedback loop where dealer hedging amplifies the move rather than dampening it. This is the scenario VVIX’s elevated level was whispering about all Friday. The institutional hedges — the VIX calls the professional community was paying for at elevated VVIX premiums — pay off sharply. The record close on SPX Friday creates a negative return day of 1.5-2.5% as the narrative shifts from “PCE cleared” to “momentum stalling at all-time highs.” The sentiment read’s greed reading of 66.6 provides no additional cushion — greed-positioned crowds do not buy dips aggressively on day one of a vol spike. Vol sizing: AVOID adding exposure on the open in this scenario. Wait for VIX to stabilize below 18 and VVIX to roll back below 93 before re-engaging. The ISM Services on Tuesday could be the reset catalyst.

8. Monday Vol Sizing — What the Surface Dictates

The vol surface gives specific guidance on position sizing for Monday that goes beyond directional bias. Four tiers apply depending on how the open develops.

The key vol trigger to watch through Monday morning is the relationship between VIX9D and VVIX. If VIX9D continues to compress toward 13 while VVIX holds above 93, the backwardation deepens and the continuation read strengthens. If VIX9D starts rising back toward 15 while VVIX simultaneously pushes higher, you have a vol regime shift beginning — that is the signal to step down from STANDARD to REDUCED sizing before the move accelerates.

9. Three-Timeframe Vol Verdict

10. Cross-Asset Context — Where Vol Fits the Bigger Picture

The vol structure does not exist in isolation. It reflects — and reinforces — the cross-asset picture that the macro and positioning analysis have mapped for this weekend. The institutional flow read for Friday showed dealer books reducing short hedges into the PCE print, which is consistent with the VIX9D falling to 14.15 as event risk cleared. The macro read confirmed the week ahead is light — no major catalysts until ISM Services Tuesday — which is why the NDX expected move for Monday prices at just 0.82%.

But two cross-asset vol signals reinforce the VVIX caution. First, gold holding its $4,800 breakout for three sessions despite a cleared PCE print is not the behavior of a market that believes all macro uncertainty is behind it. Gold vol typically compresses when macro risk resolves cleanly. The persistence of the gold bid — alongside elevated VVIX — suggests the institutional community is hedging multiple scenarios simultaneously, not just equity downside. Second, WTI crude’s 2.45% decline on Friday on what was otherwise a risk-on session is a cross-asset vol signal that global growth uncertainty did not disappear with the PCE print. Crude options carry their own vol surface — when crude falls hard on a risk-on day, it implies the underlying demand-destruction narrative is more alive than the equity rally acknowledges. That feeds back into equity vol because energy sector realized vol eventually correlates with broader market vol.

The sentiment analysis this weekend placed Fear and Greed at 66.6 — greed — while individual investor surveys show bullish readings at 38.1%, above the historical average but down 7.9 points from the prior week. That divergence — aggregate sentiment greed, individual investor less bullish than two weeks prior — is exactly the environment where VVIX at 95 makes sense. The crowd is long but the professionals running the large books are hedged. The tension between crowd positioning and institutional hedging is precisely what a 2.84-point VIX backwardation combined with 95 VVIX is priced to contain.

One additional vol signal to track on Monday: USDJPY at 153.20 approaching the Bank of Japan verbal-intervention zone at 154. Bloomberg’s reporting that Japan likely spent $34.5 billion on yen intervention in late April confirms that the carry trade remains live and contested. When yen carry unwinds — whether from BoJ action or risk sentiment reversal — it creates an immediate demand for equity vol hedges from the global funds that have been running carry-funded equity longs. If USDJPY breaks above 154 on Monday and BoJ intervenes, expect a rapid VVIX spike as those funds reach for protection simultaneously. That is the macro tail risk that the VIX curve’s back-end elevation is partly pricing.

11. Reading the Monday SPX Chain — Bowls, Washboards, and Gradients

The gamma edge analysis that professional vol watchers published this weekend identified three recurring patterns in the SPX options chain that defined Friday’s session and are likely to reappear Monday: the bowl (where price runs), the washboard (where price stalls between gamma rims), and the gradient (where price fades). Friday’s SPX session, cited as the live example, showed stacked small bowls along the chain — a washboard configuration where price was pinned between gamma concentrations during the afternoon. That pinning grew stronger into the close, which is exactly why SPY ended at $720.65 — directly at the ATM gamma peak — rather than at the pre-NY target zone of $726-728.

For Monday, the same quant analysis noted that SPX has a clear path to 7200 if the call-dominated structure holds, with GEX and DEX both surging and heavy concentration around 7250-7280 creating a tight near-term magnet. That 7250-7280 SPX zone is the bowl rim where price will run to if Monday sees continuation. The washboard behavior that trapped Friday’s afternoon session means spreads and ranged strategies worked better than directional momentum plays. If the gamma edge pattern from Friday repeats — and it tends to when the underlying is pinned at the ATM strike into an expiry — Monday’s first two hours define the session. A clean break above SPX 7280 that holds for thirty minutes suggests the bowl pattern is in play and continuation has legs. A rejection at 7280 that sends price back toward 7200 suggests a washboard developing, and range-bound positioning outperforms.

Key Vol Levels to Monitor Monday

The vol picture for Monday is bullish with a visible asterisk. The front end says calm. The back end says watch. VVIX says the professionals are not fully convinced. The gamma structure says the range is tight. All four signals, read together, point to the same conclusion that the macro and positioning analysis arrived at from different directions: continuation is the base case, but position management — not aggressive new exposure — is what wins the week. Friday’s record was not the invitation to swing for the fences. It was the signal that the easy leg of the move is complete and the harder, more selective leg is beginning. The vol structure knows this. The question is whether the rest of the market catches up by Tuesday’s ISM print.

Continue Reading — The Full Weekend Analysis

Each piece in this weekend’s analysis builds the same argument from a different angle. The vol read above is one layer. The others complete the picture.

Related reads from this weekend’s analysis:

The institutional flow campaigns that built into Friday’s record close — how the dark pool activity and systematic dealer positioning ahead of PCE shaped the Monday open structure. The vol compression you are reading above was not random; it was engineered by that positioning in the hours before the print.

The PCE cleared, Fed path, and week-ahead macro sequence — the macro read that explains why VIX 3M is still at 21.37 even after a benign PCE. ISM Services Tuesday is the next test; the vol expected move table above prices exactly that uncertainty at each subsequent expiry step.

The retail versus institutional sentiment divergence — Fear and Greed at 66.6 while VVIX remains elevated — the two-speed market where the crowd is greed-positioned and the professionals are hedged. That divergence is the same one the vol term structure is encoding, approached from the survey and sentiment data rather than the options surface.

The vol lens closes here. The tactical trade structure — entries, stops, targets, sizing in full detail — follows next in the Hot Zones and Tactics reads for the complete Monday setup.

This analysis is for educational and informational purposes only. Nothing in this post constitutes financial advice, a recommendation to buy or sell any instrument, or an invitation to invest. All prices and data reflect the Friday 1 May 2026 close. Past patterns in volatility regimes do not guarantee future outcomes. Trading derivatives and leveraged instruments carries substantial risk of loss. Always apply your own risk management framework before placing any trade.

Continue with Titan Protect

Continue with the daily framework.

Daily Pre-Asia, Pre-London, Pre-NY and Post-Close briefs across twenty-plus instruments. Indicator suite, Shield dashboard, Foundry library and live community. Today’s case study shows the read on the tape.

Core

£59/mo

Indicator suite plus daily framework reads.

Edge Popular

£109/mo

Core plus Shield dashboard and member-only briefs.

Elite

£179/mo

Edge plus weekly 1:1 call and early access to new tools.

Save 15% on annual billing

Want to see the framework in action? Free Explorer tier — no card required.

Join the live community: Discord channel · Shield dashboard

Education, not financial advice. Trade your own analysis.

Deepen Your Understanding

Related articles from the Titan Protect Foundry: